Key Takeaways

- Revolving Accessibility: Unlike a one-time term loan, a line of credit allows you to draw capital as needed, repay it, and access those funds again for new project needs.

- Rapid Deployment: Secure funding in as little as 24 to 48 hours, which can help cover urgent 941 tax deadlines or unexpected payroll spikes that traditional banks may not support quickly.

- Bridge the Payment Gap: Use a revolving line to cover upfront mobilization costs while waiting on Net 30, 60, or 90-day payment cycles common in commercial and government contracting.

- Protect Profit Margins: Fast access to capital allows you to lock in material pricing quickly, helping prevent losses caused by market fluctuations during long bank approval wait times.

Flexible Business Line of Credit for Contractors

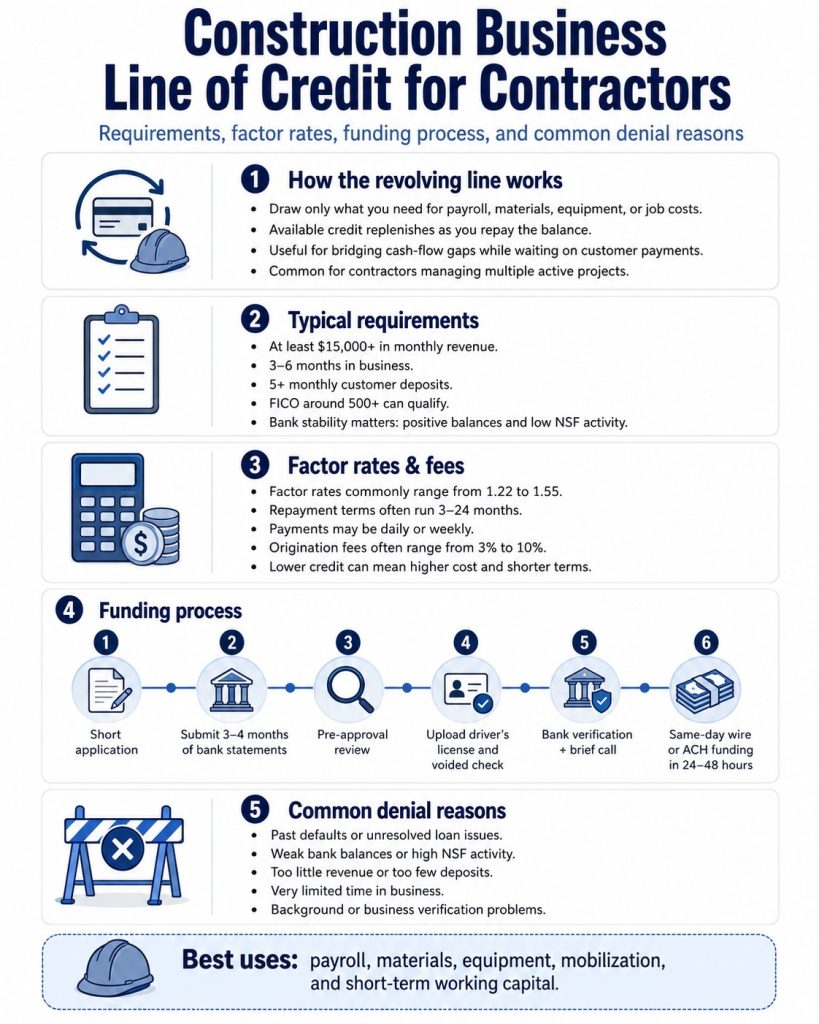

Flexible working capital, such as a line of credit for contractors with fast 24 to 48 hour funding, can help you manage your expenses when receivables exceed cash in the bank. Unlike a traditional term loan, a line of credit allows you to draw capital as you need and access more once it has been paid down. A business line of credit for contractors can help you cover urgent expenses such as payroll, 941 payroll taxes, insurance, or any other business expenses you may have while waiting on your customers, some of whom may pay on Net 30, 60, or 90-day payment cycles.

Same Day Line of Credit for Project Opportunities

A same-day credit line accessible in 24 to 48 hours or less can help your business move quickly on opportunities when they arise. To scale your construction business, you must be ready to accept purchase orders. Projects related to large commercial and government jobs often issue purchase orders which require your business to pay for expenses upfront. An unsecured line of credit for your construction business can help you be ready to cover those expenses when you most urgently need it.

What This Guide Covers About Construction Credit Lines for Contractors

As a business owner and former owner of a construction-type business, I understand the importance of having access to a revolving line of credit. As a shade structure fabricator, I would bid on government jobs. Most of this work was issued via purchase orders. This one particular complex project in Las Vegas required me to purchase over $100,000 worth of steel upfront. Fortunately, I was able to obtain a line of credit for $150,000 to cover the expenses. It took multiple banks and weeks before I was able to receive funding. Unfortunately, steel prices rose while waiting for funding. This caused a significant loss to my profit. I can understand the importance of having working capital fast. This guide explains the differences between an unsecured construction business line of credit and a line of credit from a traditional bank. You will also learn how you can apply for a construction business line of credit for contractors and get funded in 24 to 48 hours or less so you can grow your business.

Secured vs. Unsecured Construction Business Line of Credit for Contractors

Key Takeaways

- The Appraisal Gap: Banks typically lend up to 80% on real estate but may only value heavy equipment at 50%, while unsecured lines ignore asset appraisals entirely.

- Underwriting Focus: Traditional banks prioritize two years of tax returns and audited profit and loss statements, while unsecured lenders focus mainly on the last 3 to 4 months of cash flow.

- Repayment Flexibility: Bank lines often allow interest-only payments, while unsecured lines typically require both principal and interest repayment on every draw.

- Speed of Capital: A bank line can take weeks or months due to collateral valuations, while an unsecured line can be finalized in 24 to 48 hours with minimal documentation.

Traditional Bank Construction Business Line of Credit

Documentation and Qualification Requirements

A traditional line of credit from a bank, such as Chase or HSBC, requires extensive documentation, including the last two years of personal and business tax returns. You will also be required to submit the last two years of personal and business bank statements, audited profit and loss statements, and an asset balance sheet, all while maintaining a credit score of 680 or better.

Collateral Requirements and Asset Considerations

In many cases, you may also be required to provide collateral. Banks typically prefer hard assets such as real estate equity, stocks, bonds, or heavy equipment. Stocks, bonds, and other liquid assets generally offer the greatest flexibility. Real estate often requires a property appraisal before a bank will lend up to 80% of its appraised value. Heavy equipment is evaluated differently and may qualify for financing of only up to 50% of its value, if approved.

Funding Timeline and Loan Structure

A line of credit from a traditional bank requires heavy documentation and collateral in some cases, which can result in a timeline of weeks to months for final funding. However, banks offer the best interest rates compared to non-traditional lenders. Your business can also make multiple draws and make interest-only payments until the line of credit is paid. A traditional bank line is ideal when your credit is strong and you have the financials or collateral needed to qualify.

Unsecured Construction Business Line of Credit

Simplified Approval and Underwriting

Unsecured lines of credit for your construction business from non-traditional lenders offer a faster and less complicated alternative. Alternative lenders focus on your credit and cash flow rather than your tax returns and collateral. Unsecured lenders are not regulated by the same strict guidelines as traditional banks, allowing them to provide your business with capital faster and with much less documentation.

Application Process and Funding Speed

To apply for an unsecured construction business line of credit for contractors, you simply submit a credit application and your last 3 to 4 months of bank statements. The approval and funding process usually takes between 24 and 48 hours and is available for those with credit scores as low as 500. An unsecured line of credit is a perfect alternative when you need fast funding, don’t have time to wait for banks, or when the banks flat out say no.

Repayment Structure and Cost Considerations

An unsecured line of credit works very much like a traditional line of credit, with a few key differences. Your business will be able to access a revolving line of credit that can be paid off and used again. However, each draw you take will require that you make both interest and principal payments, versus the interest-only options found at banks. Unsecured lines of credit also have higher carrying costs, meaning your overall finance charges are more expensive due to the lender’s higher risk exposure. Regardless of cost, access to a fast unsecured line of credit for contractors can help your business unlock additional profits.

Revenue-Based Underwriting for Construction Business Line of Credit

Key Takeaways

- Cash Flow Over Paperwork: Underwriters prioritize recent banking activity and actual deposit history instead of multi-year tax returns or historical financial audits.

- Real-Time Performance: Lenders evaluate the last 3 to 4 months of deposits to assess current business performance; New York and California require 4 months of data to meet state guidelines.

- Deposit Density Matters: Frequent, consistent deposits throughout each month signal business stability and lower risk, which can lead to higher credit limits and better terms.

- Enhanced Accessibility: Because approval is driven by revenue volume instead of asset collateral, contractors with less-than-perfect credit can still secure a revolving line of credit.

Revenue-Based Line of Credit Underwriting

A revenue-based line of credit for construction is different from a traditional one. Unsecured revenue-based credit lines focus on your revenue rather than your historical financial documents. Lenders prioritize your last three to four months of revenue; specifically, underwriters will review the last four months for borrowers in New York and California to meet state guidelines. This approach allows for a real-time assessment of how your business has been performing based on your actual deposits.

Deposit Consistency and Approval Amounts

Underwriters look at the consistency of your banking activity as well as your total deposit volume. Frequent deposits month-over-month show that your business is stable and maintains consistent cash flow. Lenders also analyze these monthly deposits to determine the amount of capital for which your business will qualify. Generally, the greater your deposits and the higher your average daily balances, the higher your approval limit will be.

Speed and Accessibility Compared to Traditional Programs

A revenue-based construction business line of credit is much easier to qualify for than traditional bank or SBA 7(a) programs. Banks and the SBA require extensive documentation and, in many cases, hard collateral. In comparison, an unsecured contractor’s line of credit requires minimal documentation. This flexibility allows your business to access capital quickly, even if you have less-than-perfect credit.

Construction Business Line of Credit for Contractors Requirements and Qualifications

Key Takeaways

- Revenue-First Approval: Underwriters prioritize average monthly deposits over the last 90 to 120 days to determine the maximum credit limit.

- $15K Minimum Threshold: Contractors must generate at least $15,000 in monthly gross revenue to be eligible for a revolving line of credit.

- Banking Hygiene: Maintaining a positive daily balance and fewer than five NSF, or non-sufficient funds, events per month is critical for securing better rates.

- 550 FICO Floor: While revenue drives the approval amount, a minimum credit score of 550 is required to access most unsecured construction lines.

Revenue Requirements and Approval Amount

You will need a minimum of $15,000 per month in revenue to be considered for eligibility. Your approval amount is based on the average of your last three or four months of deposits, less any other unsecured loans or “positions.” New York and California residents must submit four months of business bank statements to comply with state regulations. Generally, the greater your deposits, the higher your approved limit may be. Take a look at the following example for reference:

- Month 1: $86,000

- Month 2: $103,000

- Month 3: $97,000

- Average: $95,333

In this scenario, you may qualify for a credit line of approximately $95,000, provided other requirements are met. Borrowers who have other existing positions will need to deduct the original amount of each position from that average to find their remaining eligibility.

Deposit Frequency

You will also need to make a minimum of five deposits per month to apply for a no-collateral construction business line of credit. Frequent deposits demonstrate a more diversified and stable business compared to a firm with fewer than five deposits per month. Inconsistent deposit activity can be viewed as a sign of instability and can negatively impact your approval.

Banking Activity Requirements

Underwriters also analyze your overall banking activity, specifically your average daily balances and your beginning and ending balances. Maintaining positive daily balances shows that you have the consistent cash flow necessary to repay a loan. Conversely, too many NSFs (non-sufficient funds) demonstrate potential issues like thin margins or poor cash flow management. You should aim to maintain fewer than five NSF charges per period. More than five non-sufficient fund charges in a single month may either disqualify your business or significantly increase your borrowing costs.

Time in Business

Unlike standard working capital loans, you will typically need a minimum of 6 to 12 months in business to qualify for a no-collateral line of credit for contractors. You will be able to qualify for better rates once you have surpassed two years in business. The longer your operating history, the more stability your business demonstrates. Underwriters view a longer time in business as lower risk, which often results in better rates and longer repayment terms.

Credit Requirements

Unsecured line of credit lenders focus on your revenue rather than strictly on your credit score. However, you will still need a minimum FICO score of 550 or better to qualify for a construction company line of credit. A higher credit score helps your business reduce borrowing costs and secure more favorable terms. That said, those with less-than-favorable credit are not excluded and can still be eligible to apply for a no-collateral contractor’s line of credit.

Existing Lines or Positions

You may apply for a construction company line of credit even with other outstanding loan balances, provided your revenue can support the additional payment. Lenders will deduct the original amount of existing positions from your monthly average to determine if you qualify and for how much. Your file will be considered “overleveraged” if existing positions exceed your monthly average, which will likely result in a denial.

Factor Rates, Payment Terms, and Repayment Frequency for Construction Business Line of Credit

Key Takeaways

- Multiplier-Based Cost: Unlike traditional interest, a factor rate is a fixed multiplier applied to the specific amount drawn, not the entire line.

- Draw-Specific Charges: Financing charges apply only to the capital actually used, allowing for more controlled cash-flow management.

- Term and Cost Trade-Off: Longer terms of up to 18 to 24 months offer lower payments but higher total borrowing costs, while shorter terms reduce total cost with higher periodic payments.

- Profile-Driven Frequency: Payment schedules may be daily, weekly, or monthly depending on risk profile, with monthly payments generally reserved for stronger credit and revenue credentials.

Factor Rates for Construction Business Line of Credit for Contractors

Traditional bank and SBA loans charge standard interest rates which accrue either daily or monthly on any unpaid balances. Alternative lenders, however, charge a factor rate. A factor rate is a straight integer-based calculation that uses a “multiplier” against the specific loan amount. Typical factor rates range from approximately 1.20 to 1.45 or higher, depending on your business and credit profile. This cost is applied per draw and not to the entire credit line, meaning you only pay for the capital that you actually use.

Payment Terms for Construction Business Line of Credit for Contractors

Payment terms typically range from 3 to 18 months for a construction business line of credit and may extend up to 24 months in some cases. Borrowers are approved on a case-by-case basis based on their overall business profile. Generally, a longer term makes your borrowing costs more expensive over time, though your individual payments will be lower. Conversely, a shorter term is less expensive to finance overall, although your periodic payments will be higher.

Payment Frequency for Construction Business Line of Credit for Contractors

Your payment frequency is also determined by your business profile and credit score. Lenders typically approve either daily, weekly, or monthly payments. These payments are collected directly from your account via ACH at the agreed-upon schedule. Payment frequency is approved on an individual basis, with your overall business and credit profile determining the final schedule. Higher-risk borrowers are often subject to daily payments, while weekly and monthly payments are typically reserved for borrowers with stronger financial credentials.

Common Reasons Construction Business Line of Credit for Contractors Are Denied

Key Takeaways

- The Industry Blacklist: DataMerch is a universal database that tracks repayment history across the alternative lending industry.

- SSN vs. EIN Tracking: Defaults are tied to your Social Security Number, meaning past personal business failures can impact your current company’s eligibility.

- The Modification Trap: Even without a technical default, a payment arrangement or restructuring can be flagged as a modification and viewed as a high-risk signal.

- Real-Time Risk Profile: Underwriters may view any deviation from a primary contract as evidence of current cash-flow instability, which can lead to an immediate denial.

Defaults Detected Through DataMerch

One of the most common denial reasons we see involves borrowers who have prior defaults with other unsecured lenders. Lenders will always check your file through an online resource called DataMerch, which tracks your specific lending history. Your payment history is tied to your Social Security Number (SSN) as well as your Federal EIN. This means that any past defaults with any other businesses will show up on the report; this includes any businesses you might have owned with a partner in the past. Unfortunately, any past defaults in your history will typically keep you from being approved for an unsecured contractor’s line of credit.

Payment Modifications Identified Through DataMerch

Payment modifications are also a significant reason borrowers are denied a line of credit. Any type of payment arrangement that deviates from the original agreement is considered a payment modification. Late payments or modified agreements signal to an underwriter that the business has underlying cash flow issues, which significantly increases your risk profile. This is seen as a direct indication that your business may struggle to meet future repayment obligations as well.

How to Apply for Construction Business Line of Credit for Contractors Same Day Funding

Key Takeaways

- Streamlined Documentation: Initial pre-approval requires only a simple credit application and the last 3 to 4 months of business bank statements.

- State-Specific Compliance: Borrowers in New York and California must provide a full 4 months of statements to satisfy local regulatory requirements.

- Real-Time Verification: Final underwriting uses DecisionLogic and DataMerch to verify current cash-flow hygiene and prior industry payment history.

- Same-Day Capital: Once the merchant interview is complete, funds are sent by wire transfer; meeting the 4:00 PM ET cutoff can support same-day access.

Submit Credit Application

In order to apply for a construction business line of credit for contractors, you need to complete a short online credit application. This form asks for basic information such as your business and personal name. You will also need to submit contact information, such as your phone number, as well as your business and personal details and your time in business.

Submit Business Bank Statements

The next step is to submit the last 3 to 4 months of your business bank statements via our online portal. New York and California borrowers are required to submit the last 4 months in order to comply with state regulations. You are not allowed to submit personal statements or statements from processors such as Stripe or PayPal. Ensure you transfer your funds to a proper business bank account to be considered for approval.

Receive Pre-Approval Offer

You will receive a pre-approval offer usually within a few hours, depending on the complexity of your file. The pre-approval will outline your loan amount, payment frequency, and the factor rate. This allows you to calculate your costs upfront and determine your return on investment. Should your file not meet the minimum qualifications, you will be notified as well. Those who do not meet these requirements can re-apply in 3 months.

Sign Documents

Your loan documents will be sent once you accept and agree to the offer. You will need to sign the documents, usually via DocuSign or a similar platform, and provide a copy of your state-issued driver’s license and a voided check. You may also be required to submit proof of ownership documents, such as your state articles of incorporation or tax documents like your IRS Form 1040.

Final Underwriting Review

Your file will be sent into final underwriting once all documents and stipulations are received. A more thorough investigation into your business and banking profile will be conducted. This always includes a look into your past payment history with any other unsecured lenders via DataMerch. DataMerch is an online resource that tracks this history and is used as a credit rating standard in the industry.

You will also be required to link your bank account via DecisionLogic, a real-time bank verification tool that allows the underwriter to look into your most current month’s banking activity. Underwriting will verify that your revenue is consistent with previous months and look for other unsecured loans that might have been funded but not disclosed. Such activity will cause either a denial or a reprice of your current offer. You must also make sure that your bank account balance is positive and has enough cash to cover at least three payments.

Merchant Interview

A merchant interview will also take place prior to final funding. During this interview, the underwriter will ask questions regarding the use of your funds. You may not use a contractor’s credit line for any personal purposes, and stating so will result in a denial of your loan. This process usually takes about 5 to 10 minutes at most.

Final Funding

Final funding is sent the same day once you pass the merchant interview. Funding is sent via same-day wire transfer and will arrive the same day so long as the transfer is made prior to the 4:00 PM ET wire transfer cutoff. Anything sent after the 4:00 PM ET cutoff will arrive the next day. ACH transfers typically take 24 to 48 hours to arrive in your account.

Trades That Use Construction Business Line of Credit for Contractors

Key Takeaways

- Payroll and Mobilization: General contractors use revolving lines to float subcontractor payments and labor costs while waiting for draws on large-scale projects.

- Seasonal Readiness: HVAC and roofing contractors use credit to stock inventory, such as R32 refrigerant or shingles, ahead of peak seasons and storm surges.

- Receivable Bridging: Electrical and plumbing trades use capital to bridge the gap between Certificate of Occupancy or retainage releases and upfront material costs.

- Bulk Material Hedging: Access to immediate funds allows contractors to purchase high-volatility items like copper wiring or steel in bulk to help lock in profit margins.

General Contractors

General contractors use a construction business line of credit to cover payroll, insurance, and workers’ compensation, or even to pay subcontractors when waiting for payments from customers. A construction revolving line of credit can be used over and over to cover these types of expenses. Large commercial and government projects require access to liquidity in order to accept purchase orders. A revolving line of credit for contractors gives you the capital you need to keep projects moving forward and take on new business without straining your cash flow.

HVAC Contractors

HVAC contractors can use an HVAC revolving line of credit to cover expenses such as condensers, thermostats, or enough R32 refrigerant for the entire summer. Be ready for peak seasons or extreme weather conditions. A revolving line of credit for use during peak seasons allows you to hire more technicians as well. Pay down your credit line and continue to use it over and over as opportunities arise.

Roofing Contractors

Roofing contractors can use their roofing credit line to purchase materials in bulk and be prepared for insurance claims during storm season. Insurance companies typically pay these claims in a two-stage process: the first payment is based on the Actual Cash Value (ACV), while the second payment is based on the Replacement Cost Value (RCV). You can use a roofing contractor’s line of credit to cover business expenses while waiting on the second payment, which can sometimes take weeks or months.

Electrical Contractors

Large commercial or municipal projects often require that electrical contractors work with purchase orders that do not pay until the project receives its Certificate of Occupancy. This can take weeks or months before the payment is received. Use an electrical contractor’s revolving line of credit to purchase inventory for these projects, such as copper wiring, electrical panels, and transformers. Access to revolving working capital allows electrical contractors to take on more projects and keep bills paid while receivables exceed cash on hand.

Plumbing Contractors

Use a credit line for plumbing contractors to bridge gaps between customer payments and business expenses. Use your funds for anything from a Google or Facebook marketing campaign to covering 10% retainage fees held back on large projects. Plumbing contractors must often work with a retainer that is not paid until the project is completed in full. This requires dealing with other contractors who need to finish their jobs, as well as material or weather delays common to the construction industry. A working capital line of credit allows you to unlock those retainage fees and use that capital toward growing your business.

Landscaping Contractors

Use your landscaping contractor’s revolving credit line to purchase equipment such as mowers, blowers, edgers, wheelbarrows, or any gear you need to keep your crews working efficiently. Commercial and municipal contracts also require that landscapers float project expenses upfront. These costs can add up, especially when working multiple job sites. You can also use your landscaper’s line of credit to cover payment gaps when customers pay on Net 30, 60, or even 90-day cycles, which can strain your cash flow.

How Contractors Use a Construction Line of Credit to Manage Cash Flow

Key Takeaways

- Payroll Stability: Maintains uninterrupted field operations by helping crews and subcontractors get paid on time, even during dead zones between project draws.

- Material Hedging: Allows contractors to fulfill purchase orders and lock in pricing for volatile commodities like steel, copper, or lumber before market spikes.

- Off-Season Inventory: Provides HVAC, roofing, and electrical trades the liquidity to stock high-demand units and refrigerants during the off-season to prepare for peak demand.

- Emergency Resilience: Acts as a financial safety net for equipment breakdowns or unforeseen site conditions, helping prevent costly project shutdowns.

Revolving Line of Credit for Payroll

Payroll is one of the largest expenses that any construction business owner deals with. Contractors must keep their workers paid in order for jobs to run smoothly. General contractors must also pay subcontractors even when customers have not yet paid. Delays in payroll can cause job disruptions or lead to disgruntled employees. A contractor’s credit line for payroll keeps your crews paid and your projects moving forward.

Revolving Line of Credit for Materials

Contractors often must purchase materials upfront to comply with purchase order requirements. Materials can include a variety of items ranging from concrete and lumber to steel, drywall, and underlayment. A contractor’s credit line for materials helps you make those purchases quickly and without any delays.

Revolving Line of Credit for Purchase Orders

General Contractors and subcontractors bid on commercial and municipal proejcts, many of which issue purchase orders, which are paid upon completion. Often times contraactors must wait until the Certificate of Occupancy gets issued for final payment. In the meantime, day to day expenses don’t stop. A credit line for purchase orders can be used to finance these types of projects so that opportunity is never lost.

Revolving Line of Credit for Inventory

Contractors must also purchase inventory to keep on hand to service customers. For example, an HVAC contractor or Trane dealer can use a credit line to purchase inventory such as R32 refrigerant or brand-new A/C units before the summer rush.

Revolving Line of Credit for Equipment

Contractors often need to purchase or rent equipment such as excavators, skid steers, cranes, or other job-related heavy machinery. A contractor’s credit line for equipment helps you cover these expenses without draining your bank account. This allows you to keep your projects moving efficiently while preserving cash flow for other business expenses.

Revolving Line of Credit for Emergencies

Contractors frequently face emergencies, such as equipment breakdowns or unexpected cost overruns. A revolving credit line for emergencies allows you to respond to these situations quickly. This ensures your projects remain on schedule and prevents unexpected setbacks from turning into costly job delays or lost contracts.

Revolving Line of Credit for Marketing

Contractors can also use their credit line for marketing purposes. A revolving line of credit is perfect for managing the significant expenses related to Google Pay-Per-Click (PPC), Facebook or Instagram ads, or even billboards in your city. You can grow a construction business of any type by utilizing a contractor credit line for marketing and lead generation.

Construction Business Line of Credit for Contractors With Bad Credit

Key Takeaways

- FICO Floor: While traditional banks often require a 680+ score, alternative construction lines typically have a minimum entry point of 550.

- Cash Flow vs. Credit: Underwriters prioritize the last 3 to 4 months of deposit activity and daily balance stability over historical credit reports.

- Risk-Based Terms: Lower credit scores generally result in higher factor rates and daily repayment schedules to offset lender risk.

- Path to Improvement: Consistent repayment of a bad-credit line of credit can act as a bridge, helping contractors qualify for better rates and monthly terms in the future.

Can Contractors Qualify With Bad Credit

You can still qualify for a construction business line of credit with a less-than-perfect FICO score. We require that you have a minimum credit score of 550 in order to qualify. Traditional lenders focus on your tax returns, bank statements, and profit and loss reports, as well as your credit. In contrast, alternative lenders focus on your cash flow over the last 3 to 4 months. Your cash flow provides a clear insight into your business’s ability to repay the loan. Underwriters look for consistent deposits, positive daily balances, and strong beginning and ending balances, as well as low NSF activity, to determine your overall creditworthiness.

How Bad Credit Affects Line of Credit Terms

Bad credit does not disqualify your business from applying for a contractor’s line of credit. However, borrowers with lower FICO scores will typically face higher factor rates, possibly shorter terms, and a daily payment schedule to compensate for the added risk. Regardless of these limitations, a bad credit borrower can still access revolving working capital loans to cover any business-related expenses. Borrowers with less than a 550 FICO score will more than likely not be approved. You should focus on improving your credit profile to qualify for better rates and terms in the future. Maintaining strong deposits, positive balances, and a clean payment history can also help unlock better approvals as your business grows.

From $25K to $500K+: Choosing the Right Construction Line of Credit

$25,000 Contractor Credit Line

Ideal for residential trades generating at least $25,000 in monthly revenue. This revolving capital easily covers materials for smaller jobs and bridges minor cash flow gaps while waiting on client payments. Learn more about our entry-level programs and apply for an unsecured contractor loan from $25K to $250K.

$50,000 Construction Company Line of Credit

Perfect for businesses pulling in $50,000 or more per month. This tier allows roofing or specialty firms to buy materials in bulk—like Owens Corning shingles or structural steel beams—to protect project margins. Discover how to apply for a no-doc $50,000 unsecured loan for your construction company.

$100,000 Credit Line for Contractors

Designed for mid-sized commercial or large residential projects. Construction businesses frequently deploy this level of funding to absorb weekly payroll spikes, manage bulk inventory, and support multiple active jobsites simultaneously. Explore the criteria for a $100K construction loan with no-doc working capital.

$250,000+ High-Limit Contractor Line of Credit

Geared toward stable firms with over $250,000 in monthly revenue. This tier provides a construction company with the leverage to aggressively scale operations, secure major contract bids, and maintain smooth cash flow across multiple high-value jobs. Read about qualifying for a $250K unsecured construction company working capital loan.

$500,000+ Ultra-High-Limit Construction Business Line of Credit

Reserved for mid-sized commercial entities generating $500,000 or more in monthly revenue. This elite tier of funding provides massive liquidity to fund heavy material purchases, backstop major project mobilization costs, and juggle multiple large-scale developments without draining corporate cash reserves. Check your eligibility for our premium $500K contractor working capital loans.

Explore More Contractor Financing Resources

Construction Company Loan Guide

Discover the complete breakdown of specialized general funding options, interest structures, and terms tailored exclusively for the building trades. Learn how to identify the best financing solutions to back your commercial project pipeline. Read the Construction Company Loan Guide

Bank Statement Contractor Working Capital Loans

Find out how to bypass slow traditional underwriting and skip tax return verification entirely. Learn how your actual monthly revenue and recent bank deposits can unlock fast unsecured business financing. Explore Bank Statement Working Capital Loans

Construction Business Loans for Contractors

Get a deep dive into how modern contractors and subcontractors structure short-term business capital. See how top construction firms manage multiple job sites, handle 941 payroll taxes, and fund supplier invoices simultaneously. Read the Construction Business Loans Guide

Explore Our Core Construction Financing Guides

Building a profitable contracting business requires the right financial foundation. Dive into our comprehensive pillar guides to master your cash flow, compare your funding options, and secure the capital your business needs to scale.

Working Capital Loans for Construction Companies

Learn how to stabilize your daily operations, manage weekly field payroll, and bridge the gap between extended client payment cycles with specialized, flexible working capital.

Online Lenders vs. Traditional Banks for Construction Company Loans

An upfront comparison of speed versus cost. Discover when to use a fast alternative lender to protect your project margins and when to stick with conventional bank financing.

Heavy Equipment Loans for Construction Contractors

Stop draining your liquid cash reserves on steep machinery rentals. Master the process of financing yellow iron, specialized tools, and fleet vehicles to build long-term business equity.

How to Qualify for the Best Loan Options for Construction Companies

An insider’s look at modern commercial underwriting. Find out exactly what metrics lenders analyze—from deposit volume to banking activity—and how to position your company for maximum approval amounts.

Frequently Asked Questions (FAQ)

What is a construction business line of credit for contractors?

A construction business line of credit is a revolving financial product that allows contractors to borrow funds as needed from a revolving credit line. You have the ability to repay the loan and access funds again, similar to a credit card. These funds can be used to cover cash-flow gaps, cover expenses such as payroll or materials, and juggle multiple projects at once.

How fast can I get approved and funded for a contractor line of credit?

An unsecured contractor’s line of credit can be funded within 24 to 48 hours of submitting your application. Unsecured credit lines are not subject to the same banking underwriting requirements as traditional loans and can be approved and funded efficiently and quickly. Same-day funding may be available for those who meet the requirements and submit documentation in a timely manner.

What are the minimum requirements to qualify for a revolving line of credit for contractors?

You will need to generate a minimum of $15,000 in monthly revenue. Lenders will look at the last 3 to 4 months of your business bank statements and evaluate your banking activity, such as your deposit frequency and average daily balances, to determine funding eligibility.

Can I qualify for a contractor’s line of credit with bad credit?

Yes, you can still qualify for a credit line for your construction company with a FICO score as low as 550. Your approval is based on your cash flow and overall banking activity rather than strictly your credit score or tax returns. Consistent revenue and positive daily balances demonstrate that your business has the ability to repay a loan.

How do lenders determine my construction line of credit limit?

Underwriters determine the size of your credit line based on the average of your last 3 to 4 months of gross deposits into your business bank account, minus any existing loan obligations. Underwriters average the last 4 months for borrowers in New York and California to comply with state guidelines.

What can I use a construction business line of credit for?

A line of credit for a construction business can be used for a variety of business-related expenses such as payroll, materials, marketing, inventory, or any other operational costs. You can use your credit line to cover expenses while waiting on payment from customers or to cover upfront costs related to financing purchase orders for new projects.

What is the difference between a secured and unsecured line of credit?

A secured line of credit requires that you pledge assets such as real estate or heavy equipment. Secured lines often offer lower rates but may require time-consuming appraisals. An unsecured line of credit does not require you to pledge any collateral; instead, these lines are based on your revenue and overall cash flow.

Why would a contractor be denied a line of credit?

You can be denied a line of credit due to prior defaults with other unsecured lenders, payment modifications, excessive overleveraged debt, open bankruptcies, or if your business does not meet overall underwriting guidelines.

Author Bio:

Robert “Todd” Holliday is a construction financing specialist with over two decades of combined experience in the construction and alternative lending sectors. Since 2020, he has facilitated millions of dollars in capital for contractors across the U.S., helping them navigate the complex cash flow cycles of the modern industry. As the former founder of ShadeIt, LLC (2004–2005), a commercial and residential tension shade fabricator, Todd possesses the unique “boots-on-the-ground” perspective required to understand the real-world financial pressures of materials, payroll, and project delays. He now leverages that expertise to bridge the gap between construction firms and the best available 2026 funding options.

Financial Disclaimer

The information provided in this guide is for educational and informational purposes only and does not constitute professional financial, legal, or tax advice. Loan rates, terms, and SBA program guidelines mentioned are based on early 2026 market projections and are subject to change without notice based on lender criteria and Federal Reserve policy. Qualification for any construction loan product depends on individual business factors, including credit score, annual revenue, and time in business. We recommend consulting with a certified financial advisor or a qualified tax professional before entering into any credit agreement.