Key Takeaways

- Fast Funding: Learn how to secure up to $250,000 in unsecured capital in as little as 24 to 48 hours to bridge the gap between project start and final payment.

- No Collateral Required: Understand the benefits of unsecured working capital, allowing you to fund payroll and materials without putting up equipment or property as leverage.

- Insider Industry Perspective: Get practical advice from a former construction professional on navigating factor rates and terms to maximize your project’s profitability.

Why Contractors Seek $250K Unsecured Working Capital

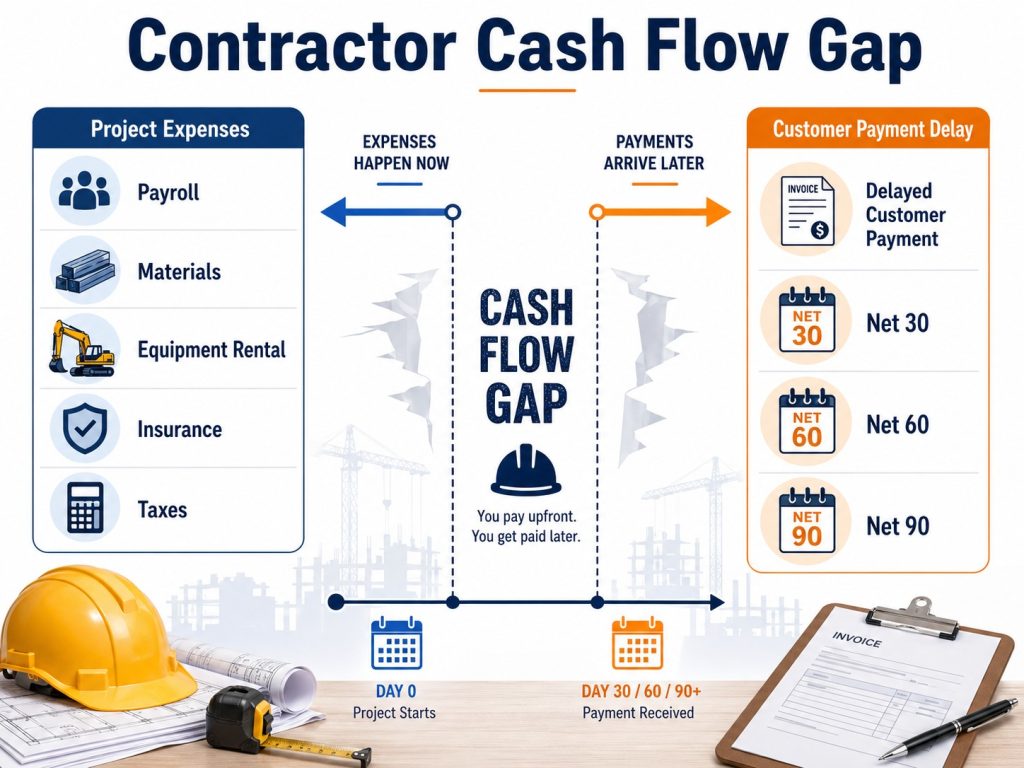

Contractors apply for a $250k unsecured construction company working capital loan for a variety of reasons. One of the primary reasons is that customers often pay contractors for projects once they are complete, or because they simply don’t always pay on time. This means that as a contractor, you need to cover all the expenses upfront. Weekly payroll, quarterly 941 payroll taxes, project materials, tools, equipment rentals, insurance, workers’ compensation, emergencies, and all sorts of other expenses need to be paid out of pocket.

Funding Large Projects Before You Get Paid

Contractors bid on large commercial or government construction projects that require financing in order to complete. Many of these projects issue purchase orders that require the contractor to pay for labor, materials, and other expenses before getting paid at completion. A $250,000 unsecured working capital loan in 24 to 48 hours can help facilitate these expenses. Short-term working capital can help your business secure additional revenue that might not be feasible otherwise.

Real-World Contractor Perspective on Access to Capital

As a former tension shade structure installer, I understand how important it is to have access to working capital when you need it. Running a construction business of any sort can be very challenging. It is even more difficult without access to funds when opportunity arises. In this guide, I will show you how you can apply for a $250,000 unsecured construction company working capital loan. You will learn about factor rates, payment frequency, and terms, as well as other insider tips.

$250,000 Unsecured Construction Company Working Capital Loan Defined

Revenue-Based vs Bank Loans

A $250,000 unsecured construction company working capital loan is different from a traditional bank or SBA-type loan. An unsecured short-term loan is a type of financing solution that is revenue-based and does not involve pledging any collateral, such as real estate or heavy equipment. Underwriters focus on your revenue and banking activity to determine your eligibility. A “no-doc” $250,000 unsecured loan also requires significantly less documentation than traditional loans. Simply submit a completed credit application as well as your last three to four months of bank statements, and you can be on your way to funding in 24 to 48 hours. Traditional lenders require extensive documentation as well as good credit for funding to take place in weeks—sometimes months. This type of speed and flexibility can be a lifesaver when receivables exceed the cash in the bank.

Why Big Jobs Require More Capital

Contractors that bid on large commercial and government projects, such as shopping centers or a new public school, need to have capital in order to complete the project in case the bid is awarded. These types of projects require the purchase of bulk materials, such as 4×4 square tubing or drywall. They also require significant manpower and access to heavy equipment. All of these are costs that sometimes have to be covered by the contractor until the job is completed. Such expenditures can cause significant strain on your cash flow. To cover these cash-flow gaps and take on large projects, contractors apply for a $250,000 no-doc construction company loan.

Approval Requirements For a $250,000 Unsecured Construction Company Loan

Minimum Monthly Revenue

In order to be approved for a $250,000 no-doc business loan, you will need to have $250,000 or more in monthly revenue. The amount of your approval is based on the average of your last 3 to 4 months of business bank statements, less any other unsecured loans you may have. That means you will need at least three consistent months of gross revenue that averages $250,000 or more. This type of revenue is not uncommon for general contractors or even subcontractors such as HVAC, landscaping, plumbing, and roofing firms.

Minimum 5+ Customer Deposits

You will also need to have at least five or more monthly deposits from your customers. Deposit frequency shows the underwriters the stability of your business. Businesses that have more than five customer deposits per month are seen as more diversified. Less than five customer deposits per month is seen as less stable due to a limited customer base.

Time in Business Requirements

You will also need to have 3 to 6 months in business to be considered for eligibility. Those with less time in business will usually have to pay higher finance costs due to the lack of business history. You will be able to get access to better programs with longer terms and better rates with at least two or more years in business. Regardless, unsecured loans offer contractors more flexibility and fewer requirements than traditional bank or SBA loans.

Cash Flow Stability, Daily Balances, and NSF Limits

Your business must also demonstrate a stable cash flow history with positive daily balances and a limited amount of NSF (Non-Sufficient Funds) charges. You should try to keep your overdraft charges to a minimum. Underwriters prefer to see that you have five or fewer NSF charges in any given 3 to 4 month period. More than five NSF charges per month can lead to higher finance costs or even a loan application denial.

Factor Rates, Payment Frequency, and Loan Terms Explained

Understanding Factor Rates

Unsecured loans from alternative lenders do not charge interest the same way a traditional bank loan or credit card product does. Banks and credit cards charge interest rates that accrue either daily or monthly on any unpaid balances. A factor rate is a straight integer-based multiplier, such as 1.29, that is used to calculate the finance charges. The factor rate is multiplied by the amount of the loan. For example, a $250,000 loan with a 1.29 factor rate has a total payback of $322,500. The formula is very simple: the loan amount multiplied by the factor rate. Factor rates will vary and are determined by a variety of considerations, including credit history.

Typical Terms for $250K Unsecured Construction Loans

Your payment terms can vary between 3 and 24 months and are approved on an individual basis. We see approvals average around 9 to 15 months for most contractors. Generally, the longer your term, the more expensive the financing charges; loans with shorter terms will be less expensive overall. Many lenders also offer early-pay discounts for borrowers. This discount is typically taken as a percentage of either the gross loan amount or the interest owed. The sooner you pay off the loan, the greater the discount. Ask your funding coordinator for specific details.

Payment Frequency: Daily vs. Weekly

Payment frequency is also approved on a case-by-case basis. Frequency is typically going to be weekly or daily. Those with better credit and strong cash flow will likely be approved for a weekly payment. Borrowers that do not meet certain requirements may be approved with a daily payment. Those with multiple loans or “positions” will also be subject to a daily payment, as lenders do not like to be the last to be paid. Payments are taken via ACH at an agreed-upon schedule once funding has been completed.

Steps Needed to Apply: Final Underwriting, DataMerch Reviews, and DecisionLogic

Submit Credit Application and Bank Statements

The first thing that you need to do is complete a basic credit application and submit your last 3 to 4 months of bank statements. New York and California residents need to submit the last 4 months due to state disclosure laws. You will need to fill out basic information such as business and personal names, as well as addresses. You will also need to submit your Social Security number as well as your Federal EIN number.

Pre-Approval Review and Eligibility Assessment

Once your credit application and bank statements are received, your file will be analyzed for pre-approval. At this point, underwriters will look at your revenue as well as your overall banking activity to determine your eligibility. You will be sent a pre-approval with the loan amount as well as the rate and terms if you are able to pass this preliminary process.

Execute Loan Documents

You will be sent your loan docs via DocuSign once you have agreed to the terms. You will need to sign and return them along with your driver’s license and a voided check, and in some cases, you will be required to provide proof of ownership. Your articles of incorporation from the Secretary of State or a copy of your K-1 from your last tax return are the proper documents needed to provide proof.

Final Underwriting Review

Once all your documents are submitted, your file will be sent into final underwriting. During this phase, the underwriter will do a more thorough background investigation which includes running your file through DataMerch, an online resource that tracks payment history for unsecured lenders. The underwriter will check to see if you have any past defaults or payment modifications with any other lenders. Any defaults or payment modifications will result in a denial at final underwriting.

DecisionLogic Bank Account Verification

You will also be required to link your bank account via DecisionLogic. This is a one-time, real-time check of your bank account. Underwriters will look to see that your revenue is consistent and that your bank account is positive. They will also be able to determine if you have taken any other undisclosed loans during the current month. Any undisclosed loans can result in a denial or repricing if your revenue does not support the additional payment.

Merchant Interview and Use of Funds Confirmation

The next step after you pass final underwriting is to complete a merchant interview. During this process, the underwriter will ask you some questions in regards to your business as well as the use of funds. You may only use the proceeds for any business-related purposes; you will be denied if you state otherwise.

Final Funding Timeline

Once the merchant interview is complete, your file will then be sent for immediate funding. Proceeds will be sent via same-day wire transfer. Your funding will arrive that same day so long as the wire is sent prior to the 4:00 PM cutoff time. Anything sent after that will arrive the following day. ACH transfers are received within 24 hours. This entire process takes 24 to 48 hours, including funding to your bank account.

Bad Credit and $250,000 Construction Working Capital Approvals

Lower Credit Scores vs. Revenue

An unsecured no-doc $250,000 loan offers more flexibility than traditional bank or SBA loans. Unsecured lenders use private funding and are not held to the same high, strict underwriting standards as banks. This means that you can still get funded with a 500 credit score, so long as your business meets other requirements. Underwriters focus on revenue vs. your credit score. You can still get approved for $250,000 so long as you meet gross revenue requirements of $250,000 and your bank account demonstrates positive daily balances and limited NSF charges.

Defaults and Loan Modifications

As stated before, you will be denied funding if you have had any defaults in the past. Your loan history is tied to your Social Security number as well, and not just your Federal EIN. Any past defaults with any other businesses, even if you were a partner, will result in a denial. Any payment arrangements that deviate from the original agreement are considered loan modifications; this, again, will result in non-approval.

Construction Trades That Commonly Use $250K Unsecured Working Capital

General Contractors and Commercial Builders

General contractors and commercial builders apply for no-doc $250K unsecured loans to cover cash-flow gaps between expenses and payment from receivables. In addition, $250K working capital can be enough to finance large projects when customers pay net 30, 60, or 90 days. A no-doc contractors loan can be used for covering payroll and materials. You can also use your loan to pay for other expenses such as equipment rentals, insurance payments, building permits, or just about any other business-related purposes. A $250K unsecured working capital loan can help your business with daily expenses when receivables exceed cash flow or to help you scale to the next level.

Roofing, HVAC, and Plumbing Contractors

Roofing contractors can use their proceeds to purchase materials such as shingles prior to deploying crews to a storm-affected area. HVAC contractors can use a $250K loan to finance commercial or government purchase orders. Plumbing contractors can bid on projects that they might not have otherwise been able to bid. Unsecured working capital can provide 24 to 48 hour funding when banks say no.

Electrical, Concrete, and Site Work Companies

Electrical, concrete, and site work subcontractors often incur upfront costs in order to cover equipment such as excavators or covering payroll. A concrete contractor can bid on a sidewalk project for the city and have the working capital needed to cover additional crews as well as expensive concrete. Access to working capital in 24 to 48 hours can help your business move beyond your current boundaries and grow.

Framing, Excavation, and Specialty Trade Contractors

Framing contractors can move beyond small local jobs to working with larger homebuilders and large commercial projects. Contractors and subcontractors have large gaps between payments; weeks sometimes, or sometimes months, can pass before customers issue payment. In addition, contractors must deal with retainage due to completion of final punch lists. Construction projects are never without issues. Access to $250K unsecured working capital can be used to cover your payroll and other expenses while you wait for issues to be resolved and payment released.

Additional Construction Financing Resources

To find the perfect funding model for your business pipeline, review our specialized guide breakdowns:

-

Construction Company Loan: Explore underwriting terms, payment structures, and general working capital options built for commercial builders.

-

Bank Statement Contractor Working Capital Loans: Find out how to bypass traditional tax return documentation and secure an approval using raw monthly sales deposits.

-

Construction Business Loans for Contractors: Read our deep dive into how field subcontractors deploy quick capital to manage payroll demands and upfront supply orders.

Frequently Asked Questions

How fast can I really get funded for a $250,000 unsecured construction loan?

FlexLendCapital.com can fund your business in 24 to 48 hours. All you need to do is complete a credit application and submit your last 3 to 4 months of bank statements. A pre-approval will be sent as soon as the same day in some instances. Final underwriting usually takes 4 to 8 hours and funding is done immediately once approved.

Do I need collateral to qualify for a $250K unsecured working capital loan?

You do not need collateral to fund an unsecured loan for $250,000. You must have at least $250K per month in revenue and demonstrate a healthy business through your banking activity, such as your average daily balances and your deposit frequency. You will need to give a personal guarantee as you would with any other business or personal credit card.

What minimum revenue is required to qualify for $250,000?

You will need $250,000 in gross monthly revenue to be considered for eligibility. You must also demonstrate consistent monthly deposits and your revenue cannot be declining over the last 3 to 4 months. Your current month of operation must also show similar revenue as well.

Can I get approved with bad credit?

Yes, you are eligible for consideration with a credit score as low as 500. Underwriters focus on your revenue as well as the overall health of your business as demonstrated through your last 3 to 4 months of banking activity. Bad credit $250,000 working capital loans are subject to higher rates due to increased risk.

How are factor rates calculated on a $250,000 loan?

Factor rates will vary depending on a variety of conditions. The longer you keep the capital, the more expensive it becomes. The shorter your term, the less expensive. Expect to pay factor rates as low as 1.22 with good credit or 1.45 with bad credit. 3-month terms have factor rates as low as 1.10.

What are typical repayment terms and payment frequencies?

Payment terms and frequency are approved on an individual basis. Terms can range from 3 to 24 months, the average being between 9 and 15 months. Payment frequency is either daily or weekly and is taken directly from your business bank account via ACH.

What can I use a $250K unsecured construction loan for?

Funds must be used for business purposes exclusively. You can use your proceeds for expenditures like payroll, materials, equipment rentals, insurance, or anything business-related. You cannot use the funds for personal expenses.

Robert “Todd” Holliday is a construction financing specialist with over two decades of combined experience in the construction and alternative lending sectors. Since 2020, he has facilitated millions of dollars in capital for contractors across the U.S., helping them navigate the complex cash flow cycles of the modern industry. As the former founder of ShadeIt, LLC (2004–2005), a commercial and residential tension shade fabricator, Todd possesses the unique “boots-on-the-ground” perspective required to understand the real-world financial pressures of materials, payroll, and project delays. He now leverages that expertise to bridge the gap between construction firms and the best available 2026 funding options.

Financial Disclaimer

The information provided in this guide is for educational and informational purposes only and does not constitute professional financial, legal, or tax advice. Loan rates, terms, and SBA program guidelines mentioned are based on early 2026 market projections and are subject to change without notice based on lender criteria and Federal Reserve policy. Qualification for any construction loan product depends on individual business factors, including credit score, annual revenue, and time in business. We recommend consulting with a certified financial advisor or a qualified tax professional before entering into any credit agreement.