Key Takeaways

- Bridge Cash Flow Gaps: Cover payroll and materials while waiting on 30, 60, or 90-day payment cycles.

- Revenue-Based Approvals: Focus is on bank deposits and activity rather than strictly credit scores or P&L statements.

- Fast Funding: No-doc options allow for funding in as little as 24 to 48 hours for urgent business needs.

Cash Flow Gaps and Customer Payment Delays

There are many reasons to apply for a $25,000 to $250,000 unsecured construction company loan. The primary reason is to bridge cash flow gaps while waiting on customers, who often pay on net 30, 60, or 90-day terms. In the meantime, you need fast cash to cover essential expenses like payroll, 941 payroll taxes, and materials such as lumber or PVC pipe. General contractors and subcontractors including HVAC, roofing, plumbing, and landscaping professionals need working capital to keep projects from stalling.

Revenue-Based Approvals

Unsecured loans are driven by revenue rather than credit, unlike traditional bank or SBA loans. Short-term working capital loans focus on your recent business bank deposits and banking activity to determine approval. This type of loan is a viable option if you have strong deposits but your credit is below 680, or if you simply need capital quickly. Programs are available for “A” through “D” rated borrowers.

Importance of Fast Working Capital

As a business owner, I understand the importance of working capital. Payroll often comes around much faster than customers pay. For your peace of mind, it is vital to have access to fast funding. I wrote this guide to help you learn how to apply for a $25,000 no-doc unsecured loan. In it, you will learn how unsecured capital works and when it is the best fit for your business.

Key Takeaways

- Payroll Stability: Ensure crews are paid on time regardless of when commercial or government checks arrive.

- Material Procurement: Buy bulk inventory or high-ticket items like HVAC condensers and lumber upfront.

- Project Scaling: Use six-figure loans to finance the mobilization of large-scale purchase orders and contracts.

Payroll and Operating Expenses

Construction company owners have to meet with regular obligations such as payroll, when customers don’t always pay on time. Commercial and government contracts often pay purchase orders once the job is complete. Apply for a $25,000 unsecured no doc contractors working capital loan to finance your projects. Access to unsecured working capital helps cover payroll, payroll taxes and other day-to-day expenses that can drain your cash-flow.

Materials and Equipment Purchases

General contractors and subcontractors such as HVAC need to purchase materials for big projects or to keep up with seasonal demands. They also need to rent equipment, purchase tools and cover the payments upfront. Short term working capital such as a $60,000 no doc contractors loan can help resolve these issues while keeping projects on schedule.

Scaling and Larger Projects

Many contractors that we fund use the capital to take on large contracts. You can apply for a $200,000 no doc contractors loan to finance your purchase orders. Commercial and government contracts issue purchase orders that are paid on completion. Use these funds to hire crews, purchase materials or any other expenses you need to complete your new project.

Understanding $25,000 to $250,000 Unsecured Construction Company Loan

Key Takeaways

- No Collateral Required: No need to pledge equipment or real estate; products work similarly to a business credit card.

- Speed vs. Documentation: Alternative loans fund in 1–2 days compared to the weeks or months required for SBA financing.

- Lump Sum Disbursement: Funds are deposited directly into your business account for immediate use on any operational cost.

Core Structure of Revenue-Based Unsecured Working Capital

A no-doc, revenue-based, unsecured construction company loan is a type of financial product designed for businesses that does not require you to pledge any collateral. This type of capital works similarly to a business credit card. You are required to give a personal guarantee, as with any credit card type product, including American Express. Funds are deposited to your account in one lump sum and can be used for any business-related expenses. Apply for a no-doc $250,000 contractors loan to cover expenses related to large projects or while you wait for customers to pay. You can use these funds for expenses such as payroll, materials, fuel, insurance, equipment rentals, or any other expenditures that you may have.

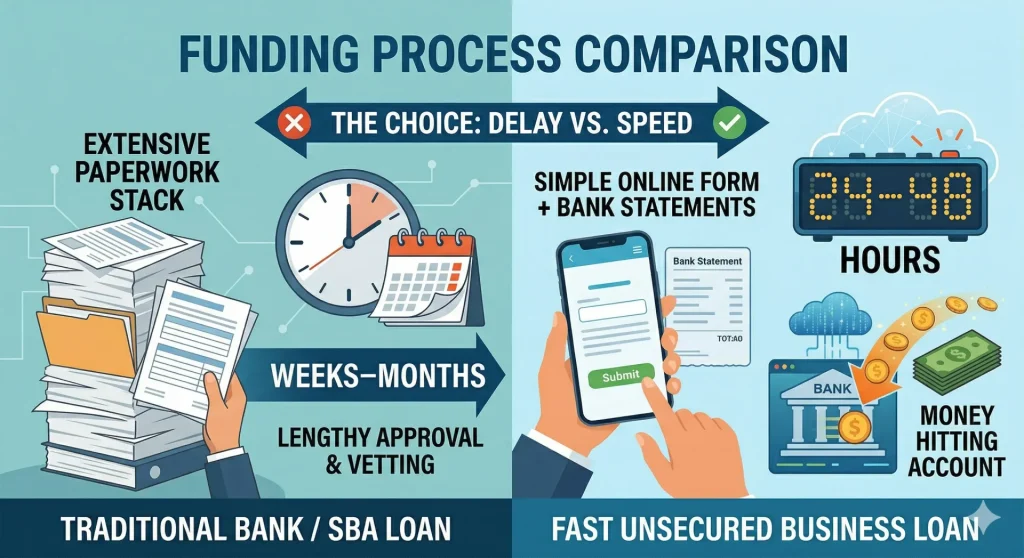

How Unsecured Loans Differ From Bank and SBA Financing

An unsecured no-doc loan is very different from traditional bank or SBA loans. Bank and SBA loans require extensive documentation, such as three years of personal and business tax returns, profit and loss statements, balance sheets, and three to twelve months of business and personal bank statements; in many cases, they may also require collateral. Unsecured loans do not require that you pledge any collateral. They also require minimal documentation, such as a completed credit application and the last three to four months of bank statements. Bank and SBA loans can take weeks or months, while a no-doc unsecured loan for $250,000 can be funded in 24 to 48 hours or less.

Why the $25K to $250K Range Fits Most Trade Contractors

Many contractors have more than $25,000 in revenue. We often see contractors with $250,000 or more in revenue; revenue in this range is not uncommon for a construction company. You can apply for a $250,000 short-term working capital loan to cover gaps in cash flow while customers pay. This type of liquidity can provide enough working capital for a variety of business-related purposes.

Understanding Costs and Repayment for $25,000 to $250,000 Construction Company Loans

Key Takeaways

- Factor Rates: Costs are determined by a fixed multiplier (e.g., 1.32) rather than an accruing interest rate.

- Repayment Terms: Terms generally range from 3 to 24 months, with most approvals falling between 9 and 15 months.

- Payment Frequency: Daily or weekly automated debits are standard, depending on credit strength and revenue consistency.

How Factor Rates Determine Total Payback

Unsecured alternative lenders calculate your finance charges differently from traditional loans. Traditional loans—like banks, the SBA, or even a retail credit card such as Dillard’s—charge interest. Interest accrues either daily or monthly on any unpaid balances. A factor rate is simply a straight calculation that multiplies your loan amount by a factor, such as 1.32. If you apply for a $250,000 no-doc contractors working capital loan, expect to pay $330,000 if your factor rate is 1.32. This amount is fixed upfront and does not fluctuate like interest-based loans.

Your factor rate is going to vary depending on a variety of qualifications, such as your credit score, your time in business, and your overall banking activity. Contractors who have a FICO score of 700 or better will qualify for “A-paper” quality lenders. If your credit score is not so perfect, expect to pay a higher factor rate. Understanding how your factor rate is calculated will help you make a better decision when you apply for a $250,000 no-doc construction company loan.

Typical Repayment Terms for $25K–$250K Contractor Loans

Repayment terms vary from 3 to 24 months. Each borrower is approved on a case-by-case basis. We see most applicants get approved for somewhere between 9 and 15 months, depending on how you qualify. The longer you hold on to the funds, the more expensive it is, but the lower the payment. Very short-term loans will pay fewer finance charges and require a higher payment to service the debt quickly.

Daily vs. Weekly Payment Structures and Cash-Flow Impact

Payment frequency is either going to be daily or weekly. This is also approved on a case-by-case basis. The stronger your revenue, credit, and banking activity, the more chances you have of being approved for a weekly payment. Expect a daily payment if your credit is low and banking qualifications are not as strong. You can also expect a daily payment if you have more than one loan or “positions.”

Structuring Payments Around Active Project Revenue Cycles

Be sure to always borrow an amount that is in alignment with your expected revenue or current accounts receivables. Borrow $50,000 in short-term working capital when you need to cover payroll while your customer owes you around that amount or more. Make sure you have enough leeway in your receivables to cover your borrowing costs as well. A smart strategy to cover a daily payment is to set aside a week’s worth of payments in advance. A properly planned and structured loan can help you manage your debt according to what you are able to afford.

Revenue-Based Approval Amount Determination

Revenue is the primary driving factor that determines the amount of your approval. You are approved based on the average of your last 3 to 4 months of deposits, less any unsecured loans you may already have. You will need $175,000 or more per month of revenue if you apply for a $175,000 construction company loan. This is not uncommon in the construction industry.

Banking Activity Review and NSF Charge Tolerance

Underwriters also look at your overall banking activity. They look at factors such as your average daily balances, number of NSF charges, customer deposit frequency, and credit, as well as other factors to determine your eligibility. Most underwriters look for 5 or less NSF charges in a 3 to 4 month period. Higher factor rates will apply for those that have more, as it shows your business has more volatility. Too many NSF charges can result in denial.

Customer Deposit Frequency and Revenue Diversification

Underwriters also look at the number of customer deposits in your bank account. You should have 5 or more monthly deposits to be considered for approval. The more frequent and diverse your deposit base appears, the better chances you have for better approval rates and terms. Those with less than 5 deposits per month will not be approved.

Existing Loan Positions and Payment Capacity Review

Lenders will also look to see if you have any existing loans with other lenders. Most underwriters will approve additional loans or positions so long as your revenue will support the additional payment. They want to confirm that adding another position will not overextend your cash flow or increase the risk of default.

DataMerch History and Prior Lending Performance

Underwriters will also look at your past lending history via DataMerch. This is an online resource that tracks your unsecured loan history. Your history is tied to your social security number and not your Federal EIN number. Any past defaults or loan modification requests will result in a non-approval. Any payment arrangement with a past lender is considered a loan modification.

DecisionLogic Real-Time Bank Activity Verification

Underwriters will also check your most recent month of business banking activity via DecisionLogic. This real-time verification allows underwriting to confirm that revenue is in line with previous months. They will also make sure that your bank account is positive and that you have not taken out any other previous undisclosed loans. Your loan will be repriced or denied if your revenue will not support any additional positions.

Final Merchant Interview and Use-of-Funds Confirmation

A brief merchant interview is conducted once you have been approved by final underwriting. You will be asked a series of questions regarding your business as well as how you are going to use the funds. You can only use the funds for business purposes, and stating otherwise can result in denial.

Funding Timeline and Disbursement Methods

Once the final merchant interview is complete, your funds will be sent to your business bank account within 24 to 48 hours. Funds are sent via same-day wire transfer or ACH transfer. Same-day wire transfers will arrive either that day or the next, depending on if the wire was sent before the 4:00 PM wire cutoff time. ACH transfers will be available in 24 to 48 hours.

Can You Apply for $25K to $250K Construction Company Loan With Bad Credit?

Key Takeaways

- FICO Floor: Approval is possible with scores as low as 500, as revenue carries more weight than credit history.

- Risk Pricing: Lower credit scores typically result in higher factor rates (1.40+) and more frequent (daily) payments.

- Hard Disqualifiers: Open bankruptcies or defaults tracked via DataMerch will result in immediate denial.

Why Revenue Matters More Than Credit Score for Contractors

An unsecured no doc $200,000 loan is different from a traditional bank or SBA loan. Traditional loans focus on 3 years tax returns, credit, P&L statements and other stipulations that may be required. Unsecured business loans focus on your revenue and your banking activity vs. your credit. Contractors with a FICO score of 500 or more are still eligible for approval. You can still get funded for $50,000 so long as your revenue meets qualifications and your business demonstrates that it can make the payments. Those with a less than 500 FICO score will get denied.

Expected Factor Rates for Higher-Risk Credit Profiles

Expect to pay a higher factor rate for a bad credit unsecured no-doc loan. Borrowers with very low credit scores will usually have to pay a factor rate of 1.40 or more, depending on your approval. Fluctuating revenue and more than 5 NSF charges in a 3 or 4 month period can also raise your borrowing costs. We have seen factor rates as high as 1.55 for borrowers with very low qualification standards. Excessive NSF charges can also result in denial.

Disqualifiers: Open Defaults, Bankruptcies, and Excessive Stacking

Underwriters will always check your borrowing history via DataMerch. Your lending history is tracked via your social security and not just your federal EIN number. This means that any defaults with any past lenders will result in non approval. Those with open bankruptcies will not be approved. You can be approved if you have a bankruptcy that has been resolved and is 2 years or more or in the past.

Trade Contractors That Commonly Apply for a $25K to $250K Unsecured Construction Company Loan

Key Takeaways

- Broad Utility: Loans serve GCs, HVAC, Roofers, and Landscapers with trade-specific needs.

- Material Financing: Ideal for purchasing lumber, shingles, PVC, condensers, and electrical panels.

- Equipment Access: Funds can be used to rent specialized machinery like cranes, bulldozers, or excavators.

General Contractors

General contractors apply for $25K to $250K construction company loans to finance large projects or commercial contracts. This funding range is perfect for covering expenses such as payroll, permits, insurance, and equipment rentals such as cranes or bulldozers, as well as other expenses. This type of financing can help bridge the gap between expenses and customer payments. A $250,000 short-term working capital loan can help you take on new projects and scale your business.

Roofing, HVAC, and Plumbing Contractors

Roofing contractors use short-term capital to purchase materials such as shingles or underlayment. HVAC and plumbing contractors can use a $125,000 short-term working capital loan to purchase inventory such as condensers or PVC pipe. Access to quick capital can keep your inventory stocked and crews paid while projects move forward without any delays.

Electrical, Landscaping, and Specialty Trade Contractors

Electrical and landscaping contractors can use a no-doc short-term $25K loan for a variety of purposes as well. Short-term business loans for contractors can be used to pay for copper wire and electrical panels, or to rent equipment such as excavators for landscapers. Trade contractors can use unsecured capital for a variety of purposes as well. A $25K unsecured no-doc loan can provide your business with enough liquidity to take on new contracts and grow your operation.

Concrete, Framing, and Site Work Companies

Concrete and framing contractors can use short-term contractors loans to pay for cement or drywall for commercial contracts. City and commercial contracts often issue purchase orders and expect job completion before issuing final payment. A fast no-doc $40,000 loan can help your business finance these types of projects.

When to Apply For $25,000 to $250,000 Unsecured Construction Company Working Capital

Key Takeaways

- Strategic Borrowing: Apply only when the return on investment (ROI) exceeds the cost of the factor rate.

- Avoid Debt Cycles: Never use unsecured loans to refinance existing credit card debt or failing operations.

- Business Purpose Only: Funds must be used for operational expenses like payroll, materials, and insurance.

When You Should Apply

Only apply for a no-doc, unsecured $25,000 to $250,000 working capital loan when you need to finance customer payments that have not arrived. Use these loans as a means of bridge capital to cover expenses such as payroll, materials, insurance, or any other business-related expenditures. You should also use this type of working capital when your return on investment exceeds the cost of the loan. A no-doc $175,000 contractors working capital loan can provide your business with cash to complete purchase orders and commercial contracts that pay upon completion.

When You Should Not Apply

Never apply for this type of loan when you need to refinance debt such as credit cards or other unsecured loans. You are already facing finance charges from your initial debt, and to add more charges on top of that does not make sense. I never recommend that borrowers pay interest on top of interest, as the math does not work in your favor. You should also never use short-term contractors working capital to keep your business from closing its doors. It is better to look for other sources of financing or simply walk away before you create debt that you will not be able to pay back.

Scalable Funding Solutions for Construction Teams

If your active pipeline or upcoming bids demand a different injection of cash, select the targeted financing tier that matches your current operating expenses:

-

$40,000 to $150,000: Construction Payroll & Cash Flow Funding to keep your skilled workforce compensated on schedule while navigating the lag time of architectural sign-offs.

-

$100,000: No-Doc Construction Working Capital to skip tedious underwriting delays and capitalize on immediate wholesale material discounts using revenue verification.

-

$250,000: Unsecured Construction Loans to establish the robust capital backing required to clear pre-qualification hurdles for high-profile regional developments.

-

$500,000: Large Project Construction Working Capital designed exclusively to sustain heavy upfront structural phases and cushion your books against delayed final closeouts.

Further Reading on Contractor Financing

To find the right cash flow solution for your specific project pipeline, explore our detailed resource hubs:

-

Construction Company Loan: A straightforward guide to working capital options, approval limits, and unsecured financing built for commercial builders.

-

Bank Statement Contractor Working Capital Loans: Find out how to secure fast business funding based strictly on your recent monthly deposits without traditional tax paperwork.

-

Construction Business Loans for Contractors: Learn how specialty crews use short-term capital lines to bridge mobilization costs and manage payroll during long payment cycles.

Frequently Asked Questions (FAQ)

How fast can I get a no-doc construction company loan funded?

An unsecured loan up to $250,000 can be funded in 24 to 48 hours. Submit a credit application and 3 to 4 months of business bank statements to start. Once the final merchant interview is complete, you can receive your funds via same-day wire transfer or ACH transfer.

Can I qualify for a $250,000 contractors loan with a credit score below 600?

Yes. You can be eligible to apply for a $250,000 contractors loan with a FICO score as low as 500. Underwriters focus on your revenue and banking activity vs. your credit and P&L statements.

What is a factor rate, and how is it different from traditional interest?

A factor rate is a fixed multiplier that is used to determine your total finance charges. A $100,000 loan with a 1.32 factor rate will repay a total of $132,000. This amount is fixed and does not fluctuate or accrue as does regular interest.

Will I be approved with a default in my past?

No, you will not be approved if you have defaulted with any other unsecured lenders. Underwriters use DataMerch to track SSN for past defaults or loan modifications. If you have an open default or a history of requesting payment arrangements with previous unsecured lenders, your application will be denied.

What is the minimum amount of monthly bank deposits I need to be approved?

You will need to have at least 5 or more monthly deposits. Frequent deposits demonstrate to the underwriter that you have a diverse customer base. Less than 5 deposits shows your customer base is limited and your business may be volatile.

What are the common disqualifiers for an unsecured construction loan?

The most common reason people are denied is having too many NSF charges in a given 3 to 4 month period and weak daily balances. You can also be denied if you have any open bankruptcies or past defaults.

What can I use the $25,000 to $250,000 working capital for?

You can use these funds to cover business expenses from payroll to advertising. Short-term bridge capital is available with minimal documentation and can be in your bank account in 24 to 48 hours.