Key Takeaways

- High-Capacity Funding: Contractors generating $500,000+ in monthly revenue can qualify for equivalent six-figure unsecured working capital.

- Bridge Net-90 Cycles: This capital is specifically designed to cover upfront mobilization costs while waiting on 30, 60, or 90-day payment terms.

- No Asset Risk: Secure up to $500,000 or more without pledging equipment liens, real estate, or specific project collateral.

- Rapid Liquidity: Access almost instant cash flow in 24 to 48 hours to keep crews working and materials arriving on schedule.

$500K+ Contractor Working Capital for High-Revenue Construction Companies

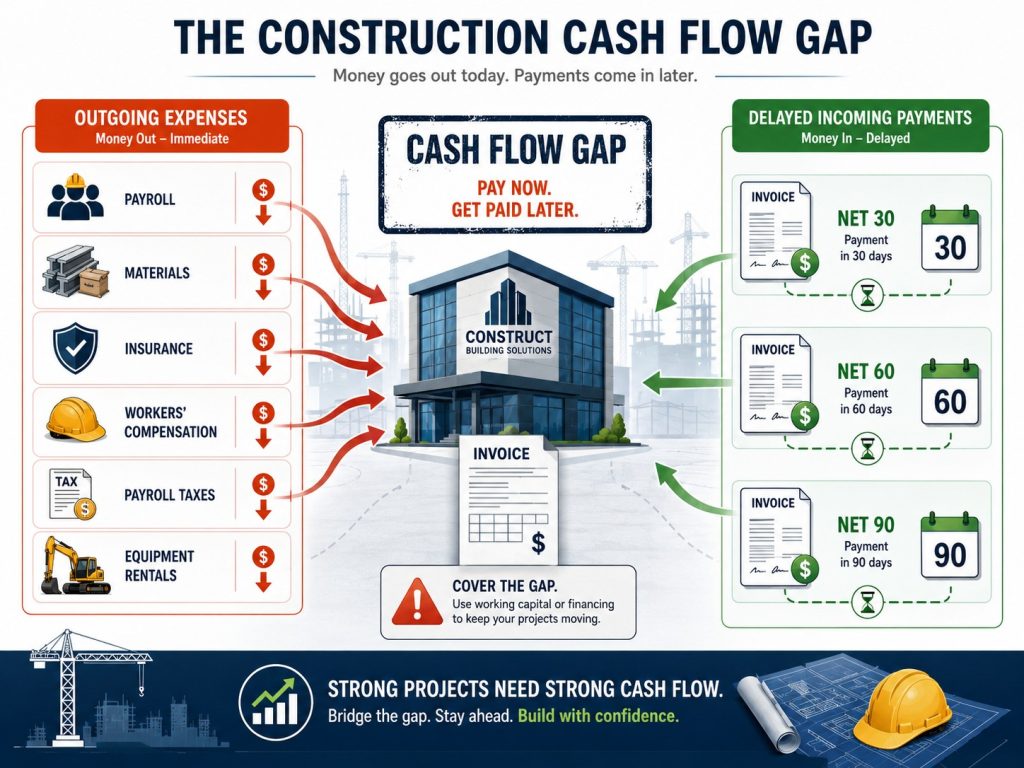

Construction is a high flying business. It is not uncommon for a construction company with $500,000 or more in monthly revenue to apply for a $500,000 contractor’s no doc working capital loan. Large commercial and government contracts are awarded on a purchase order basis. This means contractors need to upfront costs for expenses such as payroll, 941 payroll taxes, insurance, worker’s compensation and all the costs associated with completing the project. Contractors are then paid once the job is complete, sometimes net 30, 60 or even 90 days.

Bridging Cash Flow Gaps While Waiting on Receivables

Waiting on receivables can sometimes cause significant gaps in your cash flow making it more difficult to operate your business. For contractors with revenue of $500,000 or more who bid on large projects, access to no collateral working capital in 24 to 48 hours when you need it can be a huge lifesaver. Access to almost instant liquidity can keep your crews working while materials arrive on time, preventing unnecessary delays that can further detain your cash flow.

Purpose of This Guide for Contractors Doing $500K+ Per Month

As a former business owner, I understand the importance of having working capital available when you need it. Cash flow is the life blood of any small to medium sized business and without it your business will suffer. This guide will show you to apply for a $500,000 or more no collateral working capital loan. You will learn how to submit the proper documentation, the best uses and how underwriters analyze your file. The purpose of my guide is to help you get approved quickly with minimal surprises.

Revenue-Based Underwriting for High-Revenue Construction Companies

Key Takeaways

- Cash Flow Priority: Underwriters value your recent 90-120 day banking history and operational stability over static credit scores.

- Credit Flexibility: Gross monthly deposits exceeding $500,000 can effectively offset credit challenges that would trigger denials at traditional banks.

- Revenue-Linked Limits: Loan caps are typically set at 100% of your average monthly deposits, adjusted for existing debt positions.

- Regulatory Compliance: While a 3-month look-back is standard, New York and California residents must provide 4 months of statements.

Why Monthly Revenue Matters More Than Credit Scores

Unsecured lenders are not bound by the same rigid underwriting guidelines as traditional banks or the SBA, allowing for significantly more flexibility. Your banking activity over the last three to four months provides a real-time window into the operational stability of your organization. Underwriters prioritize your average daily balances and consistent deposit history to determine your ability to service the debt. In this model, a proven track record of strong, recurring deposits often carries more weight than a static credit score.

How Strong Revenue Can Offset Lower Credit Scores

Contractors seeking a no-doc loan of $500,000 or more can still qualify even with less-than-perfect credit. When banking activity reflects gross monthly deposits exceeding $500,000 alongside healthy month-end balances, it signals to underwriters that the business possesses the cash flow necessary to support the repayment. This “liquidity-first” approach allows strong revenue to effectively offset credit challenges that would typically result in a denial at a conventional bank.

How Monthly Deposits Determine Loan Size

The maximum size of your loan is primarily calculated based on the average of your last three to four months of deposits. For residents of New York and California, underwriting specifically requires a four-month look-back to comply with state disclosure laws. Underwriters also factor in any existing debt obligations; however, you can still qualify for a $500,000 no-doc loan with other “positions” (existing loans) in place, provided your top-line revenue can comfortably support the additional payment.

Example of a Deposit-Based Loan Calculation

A first-position unsecured working capital loan of $500,000 or more is typically modeled using a revenue snapshot like the one below: May: $480,000 June: $515,000 July: $505,000 In this scenario, the average monthly deposit is exactly $500,000. Underwriting would generally target an approval near this $500,000 mark, assuming the business meets other stability benchmarks such as minimal NSF activity and consistent daily balances.

$500,000 Construction Loan Bank Statement Requirements

Key Takeaways

- Revenue Benchmark: A $500,000 loan typically requires $500,000+ in monthly gross deposits to prove the business can service the debt.

- Liquidity Indicators: Strong average daily balances and healthy beginning/ending monthly balances are essential proof of repayment capacity.

- NSF Thresholds: Keeping NSF charges under five per month is critical; exceeding ten charges often leads to immediate denial.

- Activity Consistency: Lenders prefer seeing at least five deposits per month to demonstrate diverse income sources and steady project volume.

What Underwriters Look for in Business Bank Statements

When you apply for a $500K construction company loan, underwriters will carefully review your bank statements and overall cash flow to determine your eligibility. The first factor lenders evaluate is your monthly revenue. To qualify for a $500K contractors no doc loan, most lenders will expect to see at least $500K per month in deposits or more, showing that your company generates enough cash flow to support the loan.

Average Daily Balance and Account Stability

Underwriters also evaluate your average daily balance. You will need to demonstrate a positive daily balance throughout the 3 to 4 month period being reviewed. Strong daily balances, along with healthy beginning and ending balances, help show that your business can comfortably handle the loan payment. Consistently healthy balances indicate to lenders that your company maintains enough liquidity to service the debt.

NSF Activity and Overdraft Risk

Underwriting also looks closely at your NSF activity. You should try to keep your NSF charges to five or fewer per month. More than five NSF charges can increase the cost of your loan, while more than ten NSF charges may result in a denial. Lenders view NSF activity as a sign of cash flow stability, so keeping overdrafts to a minimum can significantly improve your chances of approval and better loan terms.

Deposit Frequency and Revenue Consistency

Lenders also review deposit frequency. Most lenders prefer to see five or more deposits per month along with consistent revenue patterns. Frequent deposits throughout the month show that your business has active projects and multiple income sources. Fewer than five deposits may increase your risk profile. Regular deposits demonstrate that your company generates steady income and maintains a stable customer base.

Are Tax Returns Required for Large Construction Loans?

Tax Return Requirements for Large Unsecured Construction Loans

Key Takeaways

- No-Doc Threshold: Unsecured loans under $150,000 typically require zero tax returns, focusing exclusively on recent business bank statements.

- Bank Statement Priority: Alternative lenders prioritize real-time cash flow and average daily balances over historical tax data for smaller requests.

- Rapid Funding: By reducing documentation requirements, contractors can secure project liquidity in as little as 24 to 48 hours.

- Large Loan Verification: Requests over $150,000 generally require 1–2 years of tax returns (Form 1120, 1065, or Schedule C) to verify long-term financial capacity.

Loans Under $150K Usually Do Not Require Tax Returns

Unsecured loans under $150,000 do not require any tax returns for funding purposes. For loans $150,000 and under underwriting is based on your business bank statements as opposed to full financial documentation disclosure. Lenders are able to focus on your current banking situation rather than your past tax returns.

Why Alternative Lenders Focus on Bank Statements

Alternative lenders are not regulated by the same underwriting rules as banks or SBA loans. Underwriting is focused on your averaged daily balances and the overall stability of your business based on its cash flow. This gives alternative lenders flexibility to reduce paperwork and speed up the underwriting process.

Faster Approvals Through Reduced Documentation

Reduced documentation allows lenders to speed up the approval process from weeks or months to less than 24 to 48 hours. Contractors can quickly secure liquidity for large projects or covering expenses when receivables exceed cash in the bank. Access to 24 to 48 hour funding for contractors can help your business move projects forward and avoid delays.

When Tax Returns Are Required for Larger Loans

Loans above $150,000 are usually required to submit at least one year of tax returns and in some cases two. These documents help verify your revenue over the long term and the stability of your business as well. Underwriters will ask for the most current tax returns. You can submit Form 1120 or Schedule C if you are a sole proprietor or Form 1065 for partnerships along with your K-1 schedule. These documents help verify income and the financial capacity for your construction company to be approved for a $500,000 unsecured no doc contractors loan.

Factor Rates for $500K Contractor Loans Explained

Key Takeaways

- Fixed Cost Multiplier: Factor rates are fixed integers used to calculate total payback upfront, rather than accruing interest on a declining balance.

- Simple Calculation: Total payback is determined by multiplying the loan amount by the factor rate, such as $500,000 x 1.22.

- Margin Transparency: Because the total cost is known immediately, contractors can accurately price bids and calculate project profit margins.

- Credit Impact: While scores as low as 500 are accepted, a 650+ FICO typically unlocks the most competitive rates, starting around 1.22.

How Factor Rates Differ From Traditional Interest Rates

Unsecured lenders do not calculate finance charges the same way as traditional banks and the SBA. Traditional loans are calculated using standard interest rates that accrue either daily or monthly on any unpaid balance that you owe. Unsecured lenders calculate the cost of your loan using what is known as a factor rate.

How Factor Rates Are Calculated

A factor rate is an integer based multiplier that determines the total payback of the loan. Simply multiply the factor rate times the amount of the loan. Factor rates will vary depending on your credit, time in business as well as your banking activity. Rates for high revenue contractors with good credit start at about 1.22. Your total payback for a $500,000 unsecured contractors loan with a 1.22 factor rate is going to be $500,000 X 1.22 = 610,000. The payment is then calculated by dividing the total cost of the loan by the term.

Why Factor Rates Offer Cost Transparency

The advantage is that you will know the exact cost of the loan. This makes it easier to calculate profit margins and determine if the project makes finance sense. You will be able to determine quickly and upfront the cost of the loan and compare that with the revenue generated from the project. This type of transparency allows you the flexibility needed to make faster and better informed financial decisions.

How Credit Score Influences Your Factor Rate

Your credit does play an important role in determining your factor rate. You can still apply for a $500K contractor working capital loan with a 500 FICO score. However, your factor rates will be much higher. Factor rates for a bad credit $500K working capital loan may start at 1.40 and go up from there, depending on the complexity of the file. FICO scores of 650 or better will see factor rates that may start at 1.22.

Time in Business, Revenue Stability, and Repayment Terms for a $500K Contractors Working Capital Loan

Key Takeaways

- Stability Incentives: Consistent monthly deposits and extended operating history directly correlate with more favorable rates and longer repayment terms.

- Operational Longevity: While some approvals occur at 3–6 months, a minimum of one year in business is the standard for securing $500,000+ in capital.

- Repayment Hierarchy: Top-tier profiles may unlock weekly or monthly payments, while daily structures are typical for multi-position or lower-credit files.

- Term Flexibility: Funding programs for large approvals generally range from 3 to 24 months, allowing contractors to balance payment size against total finance charges.

Introduction

Underwriters look at a variety of factors to determine if a borrower, such as a contractor will be able to repay a loan. Factors such as time in business, the consistency of your revenue and your overall banking activity help determine your terms as well the payment frequency of your loan. A contractor with $700,000 in May, $500,000 in June and $100,000 in July shows more volatility than if the contractor had $400,000 in July revenue. Contractors with consistent deposits and more time in business usually qualify for better rates and terms.

Minimum Time in Business Requirements

In order to apply for a $500K contractors working capital loan, you will need to have at least 1 or more years in business. Some underwriters approve those with 3 to 6 months in business, however, based on the size of the loan it is easier to get approved with at least one or more years in business. As a contractor and borrower you have more options available with a more stable business history. The more extensive your history the more confidence lenders have when you apply for a contractor’s 500K working capital loan.

Daily vs Weekly Repayment Structures

Underwriters determine your payment frequency based on the assessed risk level of your business. If you have very good credit, strong revenue, an established business history and no other unsecured loans then you should qualify for a weekly payment. You can have more than one position should your revenue support the extra payment, however, most underwriters will require a daily payment. You will also be subject to a daily payment should you have less than perfect credit. FICO scores as low as 500 are eligible, however, the extra risk is taken into consideration.

Monthly Payments for Top-Tier Borrowers

In some cases, monthly payments are available for contractors with highly stable consistent deposits and very good credit. Underwriters will also take into consideration where your business is located. Borrowers that reside in states, such as Texas, New York or Florida where the economy is strong may be eligible.

Payment Terms

Large $500K or more approvals are often eligible for longer payment terms. Typical payment terms range from 3 to 24 months. The longer you hold on to the funds the more expensive your finance charges, however, your payment is smaller. Shorter terms are subject to the less expensive finance charges, however, your payment is higher. Our goal is to match your business with what suits your needs the best.

How to Apply for a $500K Contractors Working Capital Loan and Get Funded in 24 to 48 Hours or Less

Key Takeaways

- Streamlined Submission: Applying requires a credit application and the last 3–4 months of bank statements (4 months for NY/CA residents).

- Transparent Offers: Pre-approval includes a full disclosure of the loan amount, factor rate, total payback, and payment frequency.

- Real-Time Verification: Final underwriting uses DecisionLogic for secure bank verification and DataMerch to confirm clean repayment history.

- Rapid Disbursement: Funds are typically sent via wire transfer, with same-day arrival available for wires completed before the 4:00 PM ET cutoff.

Credit Application and Bank Statement Submission

To apply for a $500K contractors working capital loan, you need to submit a credit application and your last 3 to 4 months of bank statements. New York and California residents need to submit 4 months due to state regulations. The application includes basic information such as business and personal information. Partnerships must submit both owners’ information, unless one of the owners has 51% or more ownership. You must also submit basic information such as your Federal EIN number and Social Security number.

Pre-Approval and Loan Offer

Once submitted, you will receive a pre-approval offer if you are eligible. This includes the loan amount, terms, as well as payment frequency. Your offer will explain the factor rate as well as the total offer of the loan. Your upfront costs will be fully transparent prior to taking the loan.

Final Underwriting and Risk Review

Once you approve the loan, you will need to sign your loan documents as well as submit your state-issued driver’s license and a voided check from your bank. At final underwriting, underwriters will also perform a DataMerch check to see if you have any past defaults or loan modifications which may disqualify your loan. You will also be required to link your bank account via DecisionLogic for a real-time bank verification. This one-time bank verification will verify your current month’s revenue. Underwriters will also be able to determine if you have taken any other undisclosed unsecured loans that may disqualify you altogether or result in a repricing of your loan offer.

Merchant Interview and Final Funding

Final funding will take place once the merchant interview has been completed. Your loan proceeds will be sent via wire transfer. Your funding will arrive the same day so long as the wire is sent prior to the 4:00 PM ET wire transfer cutoff time. Wire transfers sent afterwards will arrive the next day. The entire funding process can take 24 to 48 hours. This type of speed allows your business the flexibility it needs to respond to working capital demands when you need it.

Trade Contractors That Commonly Qualify for $500K Construction Financing

Key Takeaways

- Gap Bridging: Financing covers payroll and materials while waiting on 30, 60, or 90-day receivables.

- Seasonal Scalability: HVAC and roofing sectors use capital to scale quickly during weather events or peak demand periods.

- Competitive Bidding: Large commercial projects often require upfront mobilization capital that these loans provide.

- Operational Continuity: Fast access to funds prevents project delays and keeps crews working on-site.

General Contractors

General contractors often apply for a $500,000 working capital loan to cover expenses while waiting on customers to pay receivables. Unsecured contractor $500K funding can be used for anything from payroll and materials to workers’ compensation or any business-related expenses. Access to fast capital can keep your crews working and projects moving towards completion, all while avoiding expensive delays.

HVAC Contractors

HVAC contractors operate a seasonal business driven by the weather, and in some cases, extreme weather. Seasonal demands can place stress on your cash flow. HVAC contractors can use unsecured $500K working capital to buy inventory, such as complete AC units, and have enough capital to expand their crews and take on any weather challenge.

Roofing Contractors

Roofing companies can use unsecured capital for financing inventory to buy shingles such as GAF and Owens Corning as well as underlayment when a large hailstorm or hurricane hits. You can also use unsecured capital for expenses such as advertising campaigns as well.

Plumbing Contractors

Plumbing contractors can bid on large commercial projects that issue purchase orders that pay upon job completion. This capital can be used to cover labor expenses, materials, and anything else your plumbing contractor company needs to complete the job. Apply for a contractor’s $500,000 working capital loan and don’t miss out on opportunities that generate profit.

Landscaping Contractors

Landscaping contractors can also use unsecured working capital to cover expenses when working on multiple jobs at once. Unsecured landscaping contractor loans can be used to cover anything from payroll to equipment rental.

Electrical Contractors

Electrical contractors can also use unsecured working capital to cover expenses when customers have not paid. Sometimes customers pay late, and other times they pay in 30, 60, or 90 days. This can cause gaps in your cash flow that require a bridge loan to cover your expenses while you wait. Apply for a $500K electrical contractors loan to cover your expenses when receivables exceed cash in the bank.

Looking for a Different Amount?

If your current projects require a different capital structure, explore our targeted funding tiers:

-

$25,000 to $250,000: Unsecured Contractor Loans for flexible, everyday business expenses.

-

$40,000 to $150,000: Payroll & Cash Flow Funding to bridge the gap between customer draws.

-

$100,000: No-Doc Working Capital for fast approvals based strictly on bank statements.

-

$250,000: Unsecured Construction Loans to back large commercial or public contracts.

Additional Guides to Read

To help you find the right financing structure for your cash flow patterns, explore our dedicated resource hubs:

-

Construction Company Loan: A complete breakdown of general funding options, interest structures, and terms built for the building trades.

-

Bank Statement Contractor Working Capital Loans: Learn how to skip tax return verification and get approved fast using your actual monthly revenue.

-

Construction Business Loans for Contractors: A deep dive into how contractors and subcontractors structure capital to manage multiple job sites and supplier invoices.

Frequently Asked Questions (FAQ)

How do I apply for a $500,000 unsecured construction company loan?

Simply fill out a short credit application and submit your last 3 to 4 months of business bank statements. NY and CA residents must submit last 4 months business bank statements. You need to fill out basic information such as name, address, social security and Federal EIN number.

How much revenue do I need to qualify for a $500K contractor working capital loan?

To qualify for a $500K no doc contractor working capital loan you will need to have at least $500,000 or more in gross revenue over the last 3 to 4 months. You may have other unsecured loans that will be taken into consideration as well.

Can I get a $500,000 contractor loan with bad credit?

Yes you can still qualify for a $500,000 working capital loan for contractors if you have a minimum FICO score of 500. Underwriters will evaluate your revenue and overall banking activity to determine eligibility. Keep in mind that a lower credit score may result in higher financing costs.

Do I need tax returns for a $500K construction company loan?

Yes you will need to submit tax returns for any loans above $150,000. Underwriters will usually request the last 1 to 2 years of returns. To satisfy underwriting stipulations you can submit IRS Form 1120, Schedule C or Form 1065 along with your K-1 schedule. This helps confirm your income.

How fast can you fund my $500,000 contractor working capital loan?

You can be funded in 24 to 48 hours, sometimes less. You will need to submit a credit application and business bank statements for a pre approval, then pass final underwriting and conduct a merchant interview. The entire process can be done in 24 to 48 hours.

What can I use a $500K construction company loan for?

You can use a $500K construction company loan to cover any business related expenses such as payroll, materials, insurance, or even finance large commercial and government issued purchase orders. Contractors use this type of working capital to cover expenses when receivables exceed cash in the bank.

Do I need to pledge any collateral or give a personal guarantee?

You do not need to pledge any collateral such as real estate or heavy equipment. However, a personal guarantee is required just as with any business or personal credit card.