Key Takeaways

- Flexible Funding Range: Apply for $40,000 to $150,000 contractor working capital loans to cover payroll, taxes, materials, and essential business expenses.

- Bridge Payment Gaps: Cover Net 30–90 delays with fast unsecured financing funded in as little as 24–48 hours based on revenue and bank deposits.

- Smart Use of Capital: Learn how contractor working capital loans work, when to use them, and how they support business growth and cash-flow stability.

Cover Payroll, Taxes, and Materials With Fast Working Capital

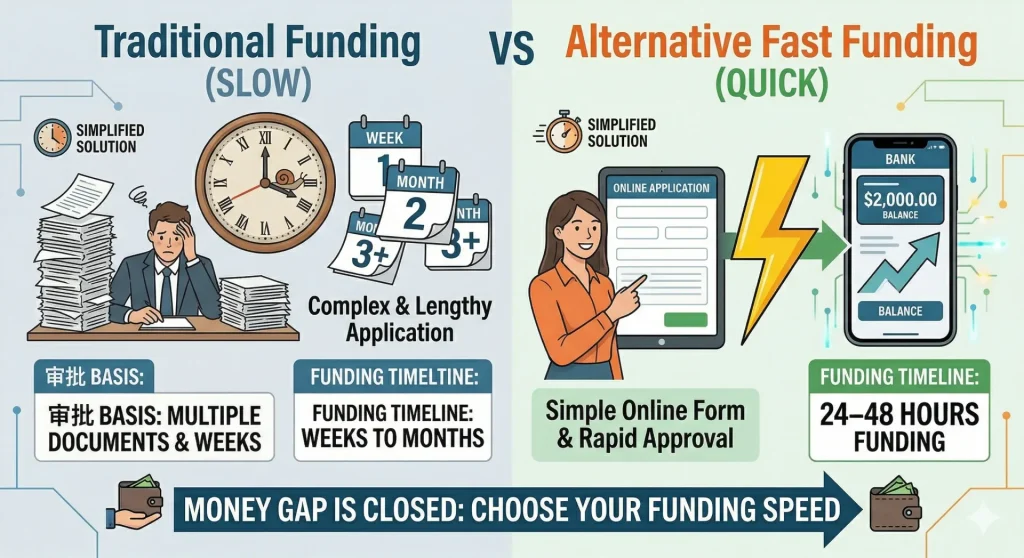

Apply for a $40,000 to $150,000 working capital loan to cover business expenses when you need to bridge gaps in your cash flow. As a contractor, you face a multitude of challenges when it comes to running your business, and keeping your operations flush with cash is one of them. A fast, short-term working capital loan can help you cover payroll, 941 payroll taxes, workers’ compensation insurance, building materials, or any other business-related expenses.

Bridge Net 30–90 Payment Gaps With Contractor Financing

Bridge capital helps you close cash-flow gaps while waiting on customers who often pay net 30, 60, or even 90 days. Used correctly, a $60K “no-doc” contractor working capital loan can keep crews working and materials on-site. While traditional loans from banks and the SBA can take weeks or months for approval, unsecured working capital from alternative lenders can be in your bank account in 24 to 48 hours, providing almost instant liquidity when it is urgently needed.

How Unsecured Working Capital Supports Construction Growth

I remember my dad telling me as a child it “takes money to make money”. Those words stuck with me, and as a business owner, I quickly began to understand exactly what he meant. The purpose of this guide is to help you better understand the ins and outs of unsecured financing, including how it works, the best use cases, and the pros and cons.

Why Apply for a $40K–$150K Construction Working Capital Loan?

Key Takeaways

- Payroll Continuity: Use $40K–$150K construction working capital loans to cover weekly payroll while waiting on Net 30–90 customer payments.

- Material Procurement: Purchase materials upfront for roofing, electrical, HVAC, and other trade-specific projects to keep jobs on schedule.

- Project Mobilization: Mobilize labor, rent equipment, and fund startup expenses for new contracts before payment is received.

Covering Weekly Payroll Across Multiple Crews

General contractors and subcontractors like HVAC, plumbing and landscaping do not always get paid immediately. Customers such as commercial or government entities pay purchase orders on schedules that do not always align with expenses. Net 30, 60, or even 90 day receivables can cause serious cash flow constraints. In the meantime, you still have employees with families to feed who need a weekly or biweekly paycheck. A no doc construction company working capital loan for $100,000 can help keep employees paid and materials at the jobsite so projects move in a timely fashion towards completion.

Purchasing Materials Upfront to Keep Projects Moving

Contractors and subcontractors like roofing contractors or electricians need to purchase materials. Shingles and underlayment are regular materials needed to complete roofing jobs. Electricians must purchase materials such as conduit, circuit breakers, electrical panels, boxes and switches. These expenses can add up, especially when working on multiple projects. Fast working capital can keep workers on the roof and electricians installing lighting without capital constraints.

Mobilizing Labor and Equipment for New Contracts

Growing your business requires investment. New contracts from bids require additional infrastructure such as more personnel, additional tools, equipment rental, per diem expenditures, materials and any other business related expense you can imagine. Suppliers need upfront payment and payroll needs to be met even before you are issued your first progress payment check. A $125,000 no doc construction company working capital loan can help cover those expenses so you can bid on additional business and keep growing.

What Is a $40,000–$150,000 Construction Working Capital Loan?

Key Takeaways

- Unsecured Revenue-Based Funding: $40,000 to $150,000 contractors working capital loans provide flexible financing with no collateral, usable for payroll, materials, and operating expenses.

- Faster Alternative to Banks: Unlike SBA and traditional bank loans, alternative lenders require minimal documentation and approve funding based on deposits and cash flow.

- Growth & Scaling Capital: Contractors with $40K+ monthly revenue can use this funding to bridge payment gaps, expand crews, and take on more projects without straining cash reserves.

Core Structure of a Revenue-Based Construction Loan

Revenue-based loans are similar to credit cards as they do not require collateral and there are no liens on property. Short-term loans, like credit cards, require a personal guarantee, which gives limited recourse in the event of a default. Your funding can be used for a variety of purposes such as payroll, building materials, insurance payments, equipment rental, or other business-related expenses. These loans are designed as a short-term solution to help finance your business operations.

How Alternative Lenders Differ From Banks and SBA Loans

Alternative or unsecured lenders require limited documentation and a much lower credit threshold compared to traditional lenders such as banks or the SBA. Traditional lenders require extensive documents like personal and business tax returns and bank statements. They also require a higher credit score, typically 680 or better, and you must submit CPA-prepared financial reports such as balance sheets and profit and loss statements. They can also deny your loan based on any of these findings.

Alternative lenders require minimal documentation. Generally, you need three to four months of business bank statements. You will specifically need four months if you are a California or New York resident to obey state laws. Underwriters look at your revenue versus your credit and only need a 500 FICO credit score to qualify. Your banking activity should reflect that your business maintains regular, positive cash flow. Funding timelines are 24 to 48 hours versus the weeks or months typically taken by banks or the SBA.

Why Mid-Size Contractors Target the $40K–$150K Range

Contractors that apply for a $150,000 working capital loan use the funds best when covering cash-flow gaps while waiting on customer payments. This type of working capital works best for contractors and subcontractors that exceed $40,000 in monthly revenue. It is not uncommon for a general contractor or subcontractor to invoice this amount or more monthly. This amount of capital provides enough liquidity to pay multiple crews, purchase materials in bulk, and take on larger projects without draining your operating cash.

Factor Rates, Payment Terms, and Payment Frequency Explained Before You Apply

Key Takeaways

- Unsecured Revenue-Based Funding: $40,000 to $150,000 contractors working capital loans provide flexible financing with no collateral, usable for payroll, materials, and operating expenses.

- Faster Alternative to Banks: Unlike SBA and traditional bank loans, alternative lenders require minimal documentation and approve funding based on deposits and cash flow.

- Growth & Scaling Capital: Contractors with $40K+ monthly revenue can use this funding to bridge payment gaps, expand crews, and take on more projects without straining cash reserves.

How Factor Rates Determine Total Payback on Construction Loans

One of the major differences between traditional loans and alternative lenders is how your total loan cost is calculated. Traditional banks charge accruing interest, which builds either daily or weekly. In contrast, unsecured lenders charge a factor rate. This is a straight integer-based calculation where you multiply the loan amount by a fixed rate, such as 1.35. For example, if you apply for a $100,000 “no-doc” contractor loan, your total payback would be $135,000 ($100,000 x 1.35). Factor rates vary based on qualification criteria; “A-paper” borrowers with strong files qualify for the best rates, while those with lower credit scores, such as a 500 FICO, will qualify for higher factor rates and potentially shorter terms.

Typical Repayment Terms for $40K–$150K Working Capital Loans

Repayment terms typically range from 3 to 24 months, with the average approval falling between 9 and 15 months. Generally, the longer the term, the more expensive it becomes to hold the capital, whereas shorter terms of 3 months or less carry a lower total cost. Longer terms offer lower individual payments, while shorter terms require higher payments. To calculate your payment, take your total payback amount and divide it by the term. Note that terms are often stated in weeks or business days.

Daily vs Weekly Payment Frequency and Cash-Flow Impact

Your payment frequency is approved on a case-by-case basis, weekly or daily. Your credit score and banking activity will determine this frequency. Daily payments occur on business days only (Monday through Friday), and weekends or holidays are unpaid. Both weekly and daily payments are collected directly from your business bank account via ACH on a predetermined date. In some cases, if you are approved for a weekly schedule, underwriting will ask you to choose the best day for the draft.

Structuring Payments Around Active Project Revenue Cycles

Always borrow an amount that is in alignment with your current receivables or expected revenue from future contracts. Do not borrow more than you can comfortably afford so you can best manage your debt load. A smart strategy for managing a daily payment is to set aside a week’s worth of payments in advance. Proper structuring ensures that your payments remain affordable and that you are able to manage debt effectively in accordance with your receivables.

Final Underwriting Review Before Funding a $40K–$150K Construction Loan

Key Takeaways

- Banking Activity Analysis: Underwriters review your last 3 to 4 months of deposits, average daily balances, NSF activity, and existing loan positions to determine eligibility and funding amount.

- Credit & Lending History Verification: Your borrowing history is checked through DataMerch, and past defaults or modified repayment arrangements can lead to decline.

- Real-Time Bank Verification: DecisionLogic is used to confirm current balances, recent deposits, and detect any undisclosed loans or liabilities.

- Merchant Confirmation Requirement: A short merchant interview is required before funding to confirm business purpose use of funds.

How Revenue Strength and Cash Flow Impact Your Loan Offer

Underwriters analyze your revenue to determine how much they are willing to lend your business. They base your approval on the average of your last 3 to 4 months of deposits into your business bank account. New York and California residents must submit 4 months of statements to follow state disclosure laws. They will also consider any other loans or “positions” you currently have. You can hold multiple positions at once, provided your revenue justifies the total payment. On average, you will need at least $65,000 in monthly revenue to qualify for a $65,000 “no-doc” contractor working capital loan.

Underwriters also examine your overall banking activity, specifically your average daily balances and the number of Non-Sufficient Funds (NSF) charges incurred. Try to avoid more than 5 NSF charges in any 3 to 4 month period to save on finance charges. More than 10 NSFs will likely cause a denial. Additionally, underwriters look at the frequency of your deposits. You generally need 5 or more deposits per month to qualify, as fewer than 5 is often viewed as having an overly limited customer base.

DataMerch Reports and Existing Loan Position Verification

Underwriters will also verify your borrowing history via DataMerch, an online resource that tracks your activity across the industry. Because you are tracked via your Social Security number, you cannot hide a past default from a previously owned company. Any past defaults or modified payment histories with other unsecured lenders will cause an immediate denial.

DecisionLogic Bank Validation and Real-Time Activity Checks

Underwriters perform real-time verification of your recent activity via DecisionLogic. They will check your current balance and recent deposits to see if you have taken out any undisclosed “no-doc” contractor loans. Your loan may be denied or repriced if your revenue has taken a significant drop or if undisclosed debt is discovered. These real-time checks are a critical part of the final underwriting stage.

Final Merchant Interview and Use-of-Funds Confirmation

Once your file passes the technical review, you must complete a merchant interview. A representative will call to ask questions regarding your business operations and your intended use of funds. It is important to remember that loan proceeds must be used for business purposes only. You may not use these funds for personal expenses or investments. Stating otherwise will cause an automatic denial.

Can You Apply for a $40K–$150K Construction Loan With Bad Credit?

Key Takeaways

- Revenue Over Credit: Alternative lenders prioritize revenue and cash flow over credit score. Contractors with FICO scores as low as 500 can still qualify if monthly deposits support the requested loan amount.

- Risk-Based Pricing: Lower credit profiles typically receive higher factor rates, often starting around 1.40 and increasing based on revenue consistency, banking performance, and overall risk.

- Hard Disqualifiers: Open defaults flagged through DataMerch or active bankruptcies result in automatic decline regardless of revenue strength.

Why Revenue Matters More Than Credit Score for Contractors

Traditional banks and the SBA typically require a 680 or higher credit score. Alternative lenders are not regulated by the same entities and can extend credit even if your FICO score is as low as 500. These unsecured lenders focus on your income and banking, not just your credit score. You remain eligible for approval as long as your business demonstrates it is capable of servicing the loan amount requested. For example, you can still get approved if you apply for a $150,000 working capital loan with a credit score of 505, provided your revenue is equal to or greater than $150,000 monthly. However, FICO scores below 500 will not be approved.

Expected Factor Rates for Higher-Risk or Bad Credit Files

You can expect to pay a higher factor rate if your credit score is low, which reflects the increased risk the lender assumes. For a “no-doc” $50,000 loan with bad credit, factor rates typically start around 1.40 and increase from there. I have seen factor rates as high as 1.55 depending on the borrower’s specific credit and business profile. Despite the higher cost, we regularly fund contractors with bad credit who need to maintain project momentum.

Disqualifiers: Open Defaults, Bankruptcies

The most significant disqualifying issue is a history of past defaults. Contractors do not always disclose previous defaults, which often occurred with a different business entity. However, DataMerch will always discover defaults associated with your current business or any business you owned in the past. Open bankruptcies will also cause an automatic disqualification.

Trade Contractors That Commonly Use $40K–$150K Working Capital Loans

Key Takeaways

- General Contractors & Builders: Use $40K to $150K working capital loans to cover payroll, materials, and jobsite expenses while waiting on customer payments.

- Roofing, HVAC & Plumbing: Rely on fast funding to purchase materials, scale crews during peak demand, and take on larger purchase-order-based contracts.

- Landscaping & Specialty Trades: Use these loans to manage cash flow and cover expenses while waiting on Net 30–90 payments.

General Contractors and Home Builders

General contractors and home builders often apply for a $150,000 “no-doc” working capital loan to cover a variety of immediate expenses. This type of funding is best utilized when you are waiting on customer payments but critical expenditures, such as payroll, cannot wait. A $150,000 contractor working capital loan ensures that your crews stay on-site, materials remain at the jobsite, and projects continue moving toward completion without delay.

Roofing Contractors

Roofing contractors often apply for a $75,000 “no-doc” contractor loan to cover material costs during high-demand storm surges. A short-term working capital loan is perfect for paying daily per-diem expenses when crews must be deployed to storm-affected areas. This $75K funding can be used to purchase materials, rent specialized equipment, or cover any other business-related expenses. Securing working capital in 24 to 48 hours allows you to keep your business ready for peak season demands.

HVAC and Plumbing Contractors

HVAC and plumbing contractors rely on short-term loans for various growth-related purposes. A fast $40,000 “no-doc” loan provides the necessary liquidity to hire additional technicians and bid on larger commercial or government jobs that issue purchase orders. Access to working capital ensures your business is able to scale operations while consistently turning a profit.

Landscaping, Electrical, and Specialty Trade Contractors

Landscaping contractors can use a $45K “no-doc” contractor loan to hire more crews for commercial contracts as needed. Similarly, electrical and specialty trade contractors, such as concrete professionals, use these loans to manage cash flow while waiting on customers who pay on net 30, 60, or even 90-day terms. Receiving cash in 24 to 48 hours helps your business stay competitive and responsive in today’s environment.

When to Use and When Not to Use a $40K–$150K Construction Working Capital Loan

Key Takeaways

- Flexible Working Capital Use: Apply for $40K to $150K contractor working capital loans to cover payroll, materials, and financing purchase orders while waiting on Net 30–90 customer payments or progress payments.

- Growth & Scaling Capital: Use fast funding to scale operations, hire crews, and take on new contracts when traditional banks decline or cannot move quickly enough.

- Responsible Borrowing: Avoid using this financing to pay off existing debt or rescue a failing business, as stacking obligations can increase payment pressure and default risk.

When You Should Apply

You should only apply for a $40K to $150K contractors working capital loan to cover expenses when waiting on customer payments or to grow your business. This type of short-term working capital is best used to cover expenses such as payroll or materials when you are waiting on progress payments or receivables that pay net 30, 60 or 90 days. You should also apply for a $40K to $150K no doc contractors loan to scale your business. Fast capital in 24 to 48 hours can help you secure working capital when customers issue purchase orders. Short term capital is a good alternative when the bank says no or is going to take too long.

When You Should Not Apply

You should not apply for this type of capital to cover other debt. Credit cards are already subject to interest and adding more interest does not work in your favor. The same can be said for paying another unsecured loan with a new one. This will more than likely spiral your debt to an unmanageable level. Never use expensive working capital as a last resort to save a failing business. At this point, it might be best to seek other sources of capital or walk away.

Explore Other Construction Working Capital Tiers

If your current project scale requires a different capital structure or a larger funding range than our payroll program, explore our full suite of construction working capital loans:

- $25,000 to $250,000: Unsecured Construction Working Capital for flexible operational capital, general business overhead, and short-term equipment rentals.

- $100,000: No-Doc Construction Working Capital for fast, streamlined approvals based strictly on bank statements without intensive tax paperwork.

- $250,000: Unsecured Construction Loans to fund major upfront mobilization and heavy material procurement for commercial contracts.

- $500,000: Large Project Construction Working Capital built for enterprise contractors managing heavy upfront expenses and severe retainage delays.

Recommended Lending Guides

To help you choose the best financial strategy for your upcoming project pipeline, browse our targeted contractor resources:

-

Construction Company Loan: A clear overview of working capital options, interest layouts, and unsecured terms designed for the building industry.

-

Bank Statement Contractor Working Capital Loans: Discover how to use your recent commercial banking history to get approved for funding within 24 to 48 hours without tax paperwork.

-

Construction Business Loans for Contractors: Learn how modern trade crews use short-term funding lines to handle upfront mobilization costs and survive slow client draws.

Frequently Asked Questions (FAQ)

How is a “No-Doc” loan different from a traditional bank loan?

Traditional bank or SBA loans require extensive documentation, including tax returns, P&L statements, and balance sheets, often taking weeks to fund. In contrast, a “No-Doc” loan only requires a simple application and 3 to 4 months of bank statements. This streamlined process allows lenders to provide funding in as little as 24 to 48 hours.

Can I still qualify for $50,000 with a 550 FICO score?

Yes. You can qualify for a $50,000 loan with a 550 credit score because underwriters prioritize your revenue over your credit. To qualify for this amount, you generally need $50,000 or more in monthly deposits and must demonstrate healthy banking activity, such as limited NSF charges and consistent positive daily balances.

How is a “Factor Rate” different from interest rates?

A factor rate is a fixed multiplier used to determine your total payback upfront. For example, a $50,000 loan with a 1.30 factor rate means you pay back exactly $65,000. Unlike an APR, which accrues interest on a declining balance, a factor rate is transparent and fixed, so you know the exact cost before signing.

Can I use the funds for 941 payroll taxes or insurance premiums?

Yes. You can use the funds for any business-related purposes, including 941 payroll taxes, crew payroll, and workers’ compensation insurance. You can also use the capital to purchase materials to fulfill large purchase orders. While any business expense is permitted, the funds cannot be used for personal expenses under any circumstances.

Will this loan require me to put up any property or equipment as collateral?

No. You do not have to pledge equipment, real estate, or other specific assets to secure a $50,000 no-doc loan. This type of financing is unsecured and works similarly to a business credit card, requiring only a personal guarantee rather than a lien on your physical property or business equipment.