Construction companies build the backbone of modern infrastructure. They construct everything from roads and bridges to skyscrapers, schools, courthouses, homes, theaters, and nearly every type of project imaginable even man-made islands like those in Dubai. To accomplish this, contractors rely on skilled labor, engineers, architects, cement, steel, and a wide range of specialized heavy equipment. A construction company building a skyscraper may need a crane, while a paving contractor requires compactors and paving equipment. Home builders often rely on boom lifts to hoist materials to second-story levels.

Construction equipment can be extremely expensive. The cost of a crane can easily run into the hundreds of thousands of dollars, while even a used boom lift can cost upwards of $50,000. Equipment ownership can often be the deciding factor in whether a contractor is awarded large projects. The challenge is that not every business has the cash available upfront to make such a significant purchase. The daily expenses of running a construction company are already cash-intensive, and when capital expenditures such as heavy equipment are added, ownership can become even more challenging.

Financing allows contractors to make these types of purchases without having to pay the full cost out of pocket. Heavy equipment loans for construction contractors provide access to essential equipment while preserving working capital. In this guide, I will explain everything you need to know about heavy equipment loans for construction contractors what’s important, who may qualify, how to qualify, and which financing options are best suited for your business.

Do you need equipment financing fast? Fill out the credit application and upload your last 6 months bank statements as well as a purchase order from your local heavy equipment dealer. FlexLenndCapital.com offers free online quotes, competitive rates and terms, as well as quick turnaround time for those that qualify.

Overview of Heavy-Equipment Loans for Construction Contractors

- Equipment Financing Access: Heavy equipment loans help construction contractors acquire essential machinery without large upfront capital investment.

- Cash Flow Preservation: Financing allows businesses to maintain liquidity for payroll, materials, fuel, and day-to-day operational expenses.

- Business Growth Support: These loans enable contractors to expand their fleet, increase capacity, and take on larger, more profitable construction projects.

Why Construction Companies use Heavy Equipment Loans

Heavy Equipment can be indispensable for a construction company owner. We used a Bobcat with an auger attachment to dig footings when I used to own a shade structure fabricator and installer. The equipment saved hours of manual labor and was a life-saver when having to dig through rock. The same goes for any construction company. Without specialized machinery, materials cannot be moved and nothing would get done. That’s why heavy equipment loans are so important for construction contractors. Here are some real and practical reasons why these loans make sense:

High Cost of Heavy Equipment

The high cost of specialized heavy equipment can drain the cash flow and life savings of any construction contractor. A used drum roller or road roller used to compact asphalt or paving can cost $45,000 used. A Bobcat is $35,000 not including all the special attachments. Most small and medium sized construction company owners simply do not have the cash to make these types of purchases. Heavy equipment financing alleviates this difficulty by allowing the cost to be spread out over easy monthly installments rather than paying the entire amount at once. Owning and growing a construction company would be almost unreachable without.

Manage Cash Flow and Retain Capital

Running a construction company is highly cash-intensive endeavor that requires constant liquidity to cover daily operating expenses such as payroll, payroll taxes, rent

and general liability insurance to name a few. Having to tie up a large amount of cash in specialized equipment would drain capital from daily operations. Heavy-equipment loans are good tools that can be used to preserve working capital while being able to afford the specialized equipment you need. Businesses that preserve cash reserves are able to maintain financial flexibility and continue to take on new projects without interrupting day-to-day operations.

Equipment Acquisition for Large Projects

Large-scale projects, such as highway construction, road development for new properties, or other major infrastructure projects, often require specialized equipment. Government contracts also require contractors to go through a rigorous vetting process. During this process, equipment inspections are conducted to ensure the contractor has the capability to perform the awarded work. Financing enables contractors to take on these projects without making large cash outlays that many small and mid-sized businesses simply cannot afford. Heavy equipment loans allow contractors to grow their business while preserving working capital.

Tax Advantages

Heavy equipment loans offer several valuable tax advantages. Section 179 of the IRS tax code allows the full purchase price of qualifying heavy equipment—such as backhoes, bulldozers, or paving equipment—to be deducted in the same tax year the equipment was placed into service. As long as the equipment is used for business purposes, the IRS allows contractors to deduct the full purchase price even if the equipment is financed. In addition, any interest paid on the loan may also be eligible for a tax deduction. Incentives like these make heavy equipment loans an attractive option for contractors looking to grow their business and acquire essential assets.

Key Features of Heavy Equipment Loans for Construction Contractors

Heavy equipment plays an important role in the construction industry, allowing complex engineering projects to be completed. Without cranes, the Manhattan skyline would not be what it is today. Roads would not have the proper pavement needed for cars to travel or trucks to deliver goods. For most entrepreneurs, purchasing heavy equipment is one of the most expensive investments required to operate a business. Heavy equipment loans for contractors allow businesses to acquire machinery they might not otherwise be able to afford. Understanding how these loans work can help construction company owners make informed decisions when financing their next major equipment purchase.

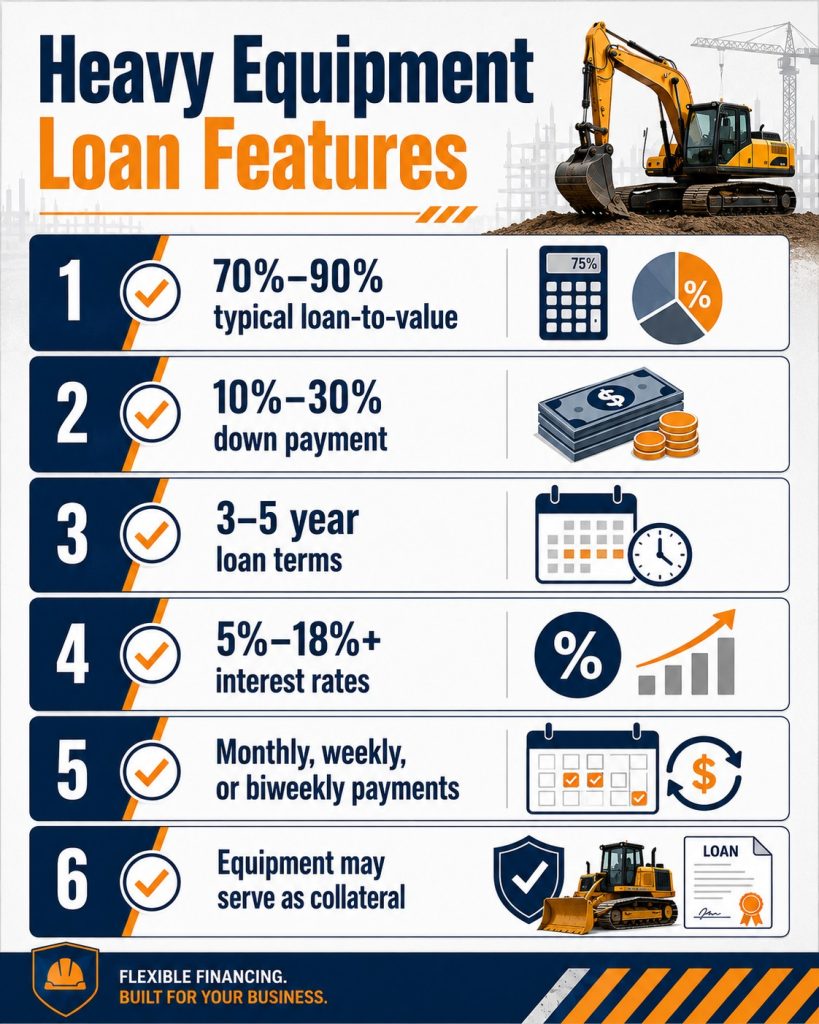

Loan-to-Value (LTV) Ratio

Most lenders will finance 70% to 90% of the cost of the equipment, especially with used machinery or vehicles such as dump trucks. Some equipment dealers will finance up to 100% on brand new purchases. A down payment from the borrower is required to fill the gap. For example, a 90% LTV means the borrower must come up with the remaining 10% down. However, some specialized equipment lenders will loan up to 120% LTV to include costs such as delivery. A variety of factors will determine how much down payment is required. Typically, those with good credit will qualify for the least down payment, although older equipment might require more. Those with credit issues will have to give the most down. Heavy equipment financing for contractors works like any other loan product.

Loan Term

The loan term is the length of the loan, usually measured in months or years. Terms on loans for heavy equipment for construction range from 3 to 5 years. This is often the life expectancy of the equipment. The longer the term, the lower the monthly payment, the more interest paid over time. Shorter terms are subject to a higher monthly payment but pay the least amount of interest.

Interest Rates

Interest rates for heavy equipment loans range from 5% to over 18%. Your rate depends heavily on your credit profile. Top-tier rates for borrowers with excellent credit of 680 or more will start around 5%. Rates for those with less than perfect credit can exceed 18%. More details can be found on NerdWallet.com.

Payment Frequency

Most loans are paid monthly, however, in the event of bad credit the lender may want weekly or bi-weekly payments. In some cases, the lender may want to establish payment history prior to going on a monthly schedule. Those with good credit will almost always qualify for a monthly payment.

Collateral Requirements

Heavy equipment loans are collateralized by the equipment itself. In many cases, the lenders will require that a GPS tracking device is installed. In the event of a default, the lender will be able to repossess the equipment. In addition, many lenders will only finance equipment that is purchased from a local dealer, be it used or new. This allows them to coordinate the installation of the tracking device post-purchase and prior to delivery.

Overview of Key Features of Heavy Equipment Loans for Construction Contractors

- How It Works: Explains how heavy equipment loans for contractors are structured and used to finance essential machinery.

- Loan-to-Value (LTV): Covers typical LTV ranges and down payment requirements based on equipment type and risk profile.

- Loan Terms: Breaks down repayment lengths and how terms impact total financing costs.

- Payment Structure: Outlines monthly versus weekly payment schedules and how they affect cash flow.

- Collateral Rules: Reviews how equipment acts as collateral and the implications of repossession in case of default.

- Financing Comparison: Helps construction company owners evaluate and compare different lender options.

- Smarter Decisions: Guides contractors toward more informed and strategic equipment purchasing decisions.

Heavy Equipment Loans for Construction Contractors: Qualifications and Eligibility Requirements

There are a few basic requirements needed to qualify for a heavy equipment loan for your construction business. You must have a registered business such as an LLC, corporation, or sole proprietorship with at least one to two years in operation. You must also meet basic credit score requirements, with the minimum being 550. Those with lower credit should expect to pay higher interest rates, while those with good credit will qualify for the best programs. You must also have a business bank account with verifiable income on your statements. In some cases, lenders will also require tax returns.

Those who have a brand new business will need to have a 650 or better credit score. Most lenders will also want a down payment of 10% to 30%. Most lenders will also require a personal guarantee from the borrower as well.

Required Documents

Most lenders will require basic documentation in order to apply for a heavy equipment loan. Be prepared to provide the following: business license and registration, proof of identity, personal and business tax returns, 6 to 12 months past business bank statements, equipment purchase order, as well as signed contracts.

Business License and Registration

Be prepared to provide the articles of incorporation from either your LLC or registered corporation. For those with a sole proprietorship, be sure to have your assumed name or DBA ready. LLC and corporate documents are available from the secretary of state in which you are registered. Sole proprietors can go to their local government offices for DBA documentation. All these documents were provided to you initially and are needed to open a bank account.

Owner’s Proof of Identity

Most lenders will require that you provide a valid state driver’s license or passport to prove your identity. This is standard procedure to prevent fraud and update all pertaining documents.

Tax Returns (Personal and Business)

Be prepared to provide 1 to 2 years of tax returns for both your business and personal taxes. Tax returns provide the lender with your overall financial picture by gauging business revenue, profitability, as well as stability. The analysis made from these documents will determine if you are approved, for how much, and at what terms.

Business Bank Statements (last 6 to 12 months)

Lenders will always want to look at your bank statements to determine and verify your cash flow. They use these statements to assess your income vs. expenses and determine the overall financial health of the business.

Heavy Equipment Purchase Receipt or Dealer Quotation

Heavy equipment loans are made against a purchase order for a specific unit. The purchase order provides basic information such as serial number, year, make and model, as well as the condition of the equipment, be it new or used.

Signed Contracts or Signed Plans

All loan and sales documents must be signed prior to the equipment leaving the lot. Once the documents have been signed, the lender can fund the loan and pay the dealer. At this point, the clock starts ticking, and the loan must be paid according to schedule.

Final Checklist

Prior to submitting your application, it is important to ensure that all your documentation is in complete order. Gather your most recent tax returns, bank statements, proof of insurance, and any other required documentation. Having all your paperwork in order makes your life easier and improves your chances of getting approved.

Overview of Heavy Equipment Loans for Construction Contractors: Qualifications and Eligibility Requirements

- Business Requirements: Must be a registered business with at least 1–2 years in operation to qualify for most equipment financing programs.

- Credit Score Guidelines: Minimum credit score typically starts around 550, while 650+ is preferred for newer businesses seeking better terms.

- Interest Rate Factors: Rates vary based on your credit profile, time in business, and the lender’s underwriting criteria.

- Down Payment: Expect to provide 10%–30% upfront depending on the equipment type and risk profile.

- Financial Documentation: Verifiable business bank statements are required to demonstrate revenue and repayment capacity.

- Personal Guarantee: Most lenders require a personal guarantee to secure the financing agreement.

Risks and Drawbacks of Heavy Equipment Loans for Construction Contractors

Every purchase does not come without its risks and drawbacks. The purchase of heavy equipment is not without its pros and cons. Take a look at some of the drawbacks owners must face.

High Monthly Payments

Heavy equipment can be very expensive. Expect a high monthly payment, especially if your specialized equipment costs north of $50,000. Be sure to have enough cash flow on hand to pay for six months of payments in the event projects are delayed. Be sure to plan your monthly payment around your cash flow. Bottom line: do not bite more than you can chew, or you could end up in a financial bind.

Equipment Depreciation

Every piece of equipment or machinery depreciates over time. A brand-new dump truck can cost more than $100,000 and only sell for $45,000 a few years later. If your equipment depreciates faster than you can pay it off, you will owe more than the equipment is worth. You may end up losing money in the event of a fire sale.

Maintenance, Fuel, and Insurance Costs

Owning any piece of heavy equipment is like owning a car. Equipment requires regular maintenance and repairs. Be sure to factor in the costs of oil changes, new tires, or even accidents as part of your maintenance expenses. These costs can range in the thousands of dollars per year, depending on the equipment. Be sure to factor in the costs of fuel and insurance. Heavy equipment requires either diesel or gasoline to run, and insurance to keep it protected. All these additional costs will add to your monthly cost of ownership.

Overview of Risks and Drawbacks of Heavy Equipment Loans for Construction Contractors

- Cash Flow Pressure: High monthly payments can strain your business cash flow, especially during slow project cycles or delayed receivables.

- Depreciation Risk: Equipment loses value over time and may be worth less than the remaining loan balance.

- Ongoing Ownership Costs: Maintenance, fuel, repairs, and insurance add significant long-term expenses beyond the loan itself.

How to Choose the Right Lender for Heavy Equipment Loans for Construction Contractors

Be sure to review the following criteria before choosing a lender for your next specialized heavy equipment purchase. Factors to take into consideration are interest rates and additional fees, speed of approval, and area of expertise. Having all your facts straight will help you make the right decision when you choose the right lender for your heavy equipment financing needs.

Review interest rates and additional fees

Be sure to compare and review offers prior to accepting anything. Double-check interest rates and read the fine print to make sure that you understand everything. If something sounds too good to be true, it usually is. Some low-interest offers are loaded with extra fees that can result in higher costs over time.

Speed of loan approval and disbursement

Know how long it is going to take to get approved. Banks and SBA 504 loans can take weeks, even multiple months, to get final approval. On the other hand, online lenders such as FlexLendCapital.com can get you approved in 48 to 72 hours. Therefore, it is important to understand the urgency behind your loan. Have your timeline ready prior to making any purchase decision.

Area of Expertise

Be sure to look for lenders who specialize in heavy-equipment lending. Lenders who specialize in heavy equipment are more likely to approve your loan quicker. Banks and other lenders may be less likely to approve your purchase.

Reputation

Be sure to work with a reputable lender. Most lenders do not have your best interest in mind. Keep in mind that lenders hire salespeople who will always tell you what you want to hear. A reputable lender will monitor their sales staff and eliminate those with less-than-scrupulous practices.

Overview of How to Choose the Right Lender for Heavy Equipment Loans for Construction Contractors

- Rate Comparison: Compare interest rates carefully and watch for hidden fees that can increase the total cost of financing.

- Funding Speed: Understand the lender’s approval and funding timeline to ensure it aligns with your project deadlines.

- Industry Expertise: Choose lenders that specialize in heavy equipment financing and understand construction business needs.

- Reputation Matters: Work with reputable lenders and avoid high-pressure sales tactics that may lead to unfavorable loan terms.

How to Improve Your Approval Odds for Heavy Equipment Loans for Construction Contractors

Take a look at the following strategies to improve your approval odds for heavy equipment loans. Being armed with the right knowledge can make the difference between getting approved or not.

Maintain a strong and stable credit score

Most lenders in 2026 and beyond will look at your personal credit score. Be sure to pay your bills on time. Avoid delinquencies of any kind to show that you are a responsible creditor. Strong credit scores will improve your chances of loan approval and help you avoid any necessary delays.

Show proof of stable contracts or future projects

If you have signed contracts or a pipeline of upcoming projects, it gives lenders confidence that your business has a steady stream of income. With such documentation, you may be able to borrow more for multiple pieces of equipment.

Have all documents ready in advance

Have all your documents in order prior to applying for heavy equipment for your construction company. Using folders can sometimes help keep documents such as these in order. Take your tax returns and place them in a labeled folder. Keep a proper file for your business licenses as well. All your bank statements should be available online. Have them printed and ready ahead of time. Lack of documentation can slow down the approval process or lead to a disappointing rejection.

Start with a limited loan

Try starting with a smaller loan if you have limited credit. This gives you time to establish a good working relationship with your lender. Consistent and timely payment will eventually lead to better terms and rates for larger loans. Baby steps or stepping stones is a timeless common-sense strategy you can use to set yourself up in the future.

Consider an alternative recourse in case of a low credit score

Those with a less-than-perfect credit history should consider other resources such as a co-signer. Most lenders will accept a cosigner; however, they will average both credit scores to determine eligibility. Bad credit borrowers may also need to come up with additional money for a down payment to improve approval odds.

Overview of How to Improve Your Approval Odds for Heavy Equipment Loans for Construction Contractors

- Credit Strength: Maintain a strong credit score and avoid late payments to qualify for better rates and higher approval chances.

- Proof of Revenue: Show stable contracts or upcoming projects to demonstrate consistent cash flow and repayment ability.

- Prepared Documentation: Have all required documents organized in advance to speed up the approval process.

- Start Smaller: Begin with a smaller loan amount if your credit profile is limited to build lender confidence.

- Risk Mitigation: Consider a co-signer or a larger down payment to strengthen your application if your credit is low.

What Types of Heavy Equipment Can Be Financed?

Specialized lenders such as FlexLendCapital.com will finance a wide variety of both new and used heavy equipment for construction contractors. Factors such as the age, condition and resale value will affect the approval as will the borrower’s credit. Listed below are some of the common pieces of heavy construction equipment that can be financed in the United States.

Earthmoving & Site Preparation Equipment

- Skid steers and compact track loaders (Bobcats)

- Excavators and mini excavators

- Backhoes

- Bulldozers and dozers

- Wheel loaders

- Trenchers and scrapers

Paving & Road Construction Equipment

- Drum rollers and compactors

- Asphalt pavers

- Milling machines

- Road reclaimers and stabilizers

- Concrete spreaders

Lifting & Access Equipment

- Cranes

- Boom lifts

- Scissor lifts

- Telehandlers

- Rough-terrain forklifts

Concrete & Masonry Equipment

- Concrete mixers and batch plants

- Concrete pumps

- Power trowels

- Shotcrete machines

- Rebar benders and cutters

Hauling & Job-Site Support Equipment

- Dump trucks and trailers (when paired with equipment programs)

- Water trucks

- Fuel trucks

- Generators and light towers

- Compressors

Specialty & Attachment Financing

Many lenders will also finance attachments and specialty tools when they are purchased with the primary machine, including:

- Augers

- Buckets and grapples

- Hydraulic breakers and hammers

- Compaction wheels

- Mulchers and trenching attachments

In most cases, financing is structured around the specific piece of equipment being purchased, meaning the lender evaluates the machine’s make, model, year, condition, and resale value in addition to the contractor’s financial profile. Well-known brands such as Caterpillar, John Deere, Komatsu, Volvo, Takeuchi, Bobcat, and CASE typically receive the most favorable terms because of their strong secondary-market value.

Choosing the right equipment to finance and working with a lender that understands construction machinery—can make it easier to secure approval, minimize down payments, and keep monthly payments aligned with project cash flow.

Frequently Asked Questions About Heavy Equipment Loans for Construction Contractors

How fast can construction contractors get approved for heavy equipment loans?

Approval timelines may vary by lender. Banks and SBA programs can take several weeks or months. We usually take 24 to 72 hours to approve and fund a loan once documentation is submitted.

Can I finance used heavy equipment?

Yes. We finance used equipment all the time, although from experience older machines require a larger down payment or shorter loan term. The condition, brand, and resale value of the equipment play a major role in approval.

What credit score do I need to qualify for a heavy equipment loan?

We can work with minimum credit scores of 550. We find that newer businesses often need 650 or higher. As with any loan product, borrowers with stronger credit generally qualify for lower interest rates and smaller down payments.

Do heavy equipment loans require collateral?

Yes. The equipment being financed typically serves as collateral for the loan. Our partners usually also install a GPS tracking device to monitor your equipment.

How much down payment is required for heavy equipment financing?

We require a down payment that usually ranges from 10% to 30%, depending on your credit profile, business history, and the type of equipment being purchased. In some cases we finance up to 100% for brand-new equipment.

Can startup construction companies qualify for heavy equipment loans?

Startups may qualify, but usually need stronger personal credit, a larger down payment, and proof of contracts or future projects. Some lenders also require personal guarantees. We have programs that may work for startups. Contact us for more details.

Are heavy equipment loan payments monthly or weekly?

We see borrowers with good credit qualify for monthly payments while those with weaker credit profiles may be required to make weekly or biweekly payments until payment history is established.

What documents are required to apply for a heavy equipment loan?

We need documentation such as business registration, proof of identity, tax returns, recent bank statements, insurance, and a purchase order or dealer quote for the equipment.

Can heavy equipment loans be used for multiple machines?

Yes. We have customers buy multiple pieces of machinery regularly. So long as the business is able to qualify with good credit, cash flow, etc.

What happens if I default on a heavy equipment loan?

We try to avoid this scenario at all costs and will work with you as much as possible. However, If you are unable to pay the loan your equipment is subject to repossession.