Key Takeaways

- Operational Continuity: Ensures critical weekly payroll obligations are met without interruption, helping prevent job site delays or labor disputes.

- Revolving Liquidity: Unlike fixed loans, a revolving line allows contractors to draw only what is needed for each pay cycle and reuse the capital as soon as it is repaid.

- Bridge the Net Pay Gap: Designed to float labor costs while waiting on Net 30, 60, or 90-day payment terms from general contractors or government entities.

- Streamlined Access: Provides a path to same-day funding with minimal documentation, bypassing the lengthy underwriting cycles of traditional banks.

Payroll Line of Credit for Contractors Same Day Funding

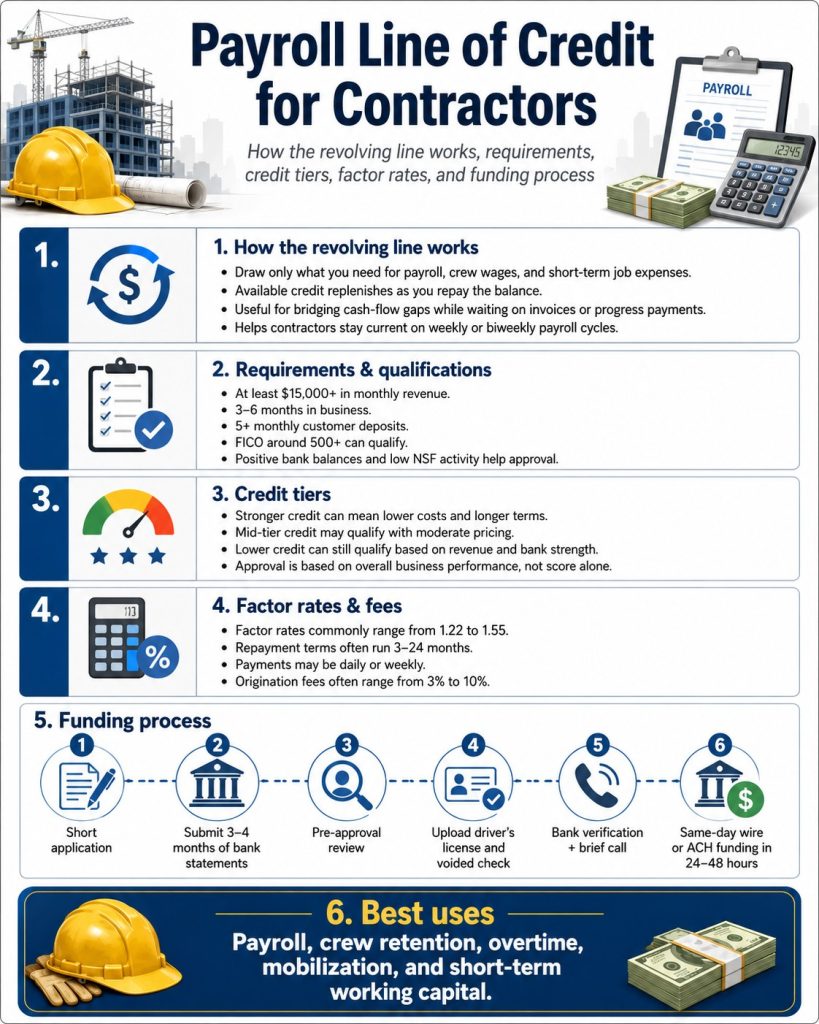

A payroll line of credit for contractors can provide your business with the flexible capital it needs to make payroll every pay period. Payroll can be one of the largest ongoing expenses you will face as a contractor. Workers and subcontractors have families to feed and bills to pay; they rely on the fact that your business has the funds needed to make payroll every week. Missed payroll can lead to job delays as well as upset workers. Access to a payroll line of credit for contractors ensures your jobs move forward without any delays.

Flexible Payroll Funding for Contractors

A contractor’s payroll credit line allows you to draw funds as needed and use them again once the funds have been repaid. This type of flexibility is important when dealing with purchase orders or customers who pay on Net 30, 60, or 90-day cycles. These types of payment gaps can put a strain on any business, making it more difficult to meet basic obligations such as payroll. Access to same-day funding when your business needs it can be a lifesaver for any construction business.

What You Will Learn About Payroll Line of Credit for Contractors

As a former shade structure fabrication business owner, I understand the importance of having access to revolving working capital. Running a business in a constantly changing, dynamic environment can be quite challenging. This guide will show you how you can apply for an unsecured contractor’s line of credit for payroll with minimal documentation and same-day funding. You will also learn how underwriting evaluates your business to determine your eligibility, as well as the qualifications needed, factor rates, repayment terms, and payment frequency.

Revenue-Based Underwriting for Payroll Line of Credit for Contractors

Key Takeaways

- Efficiency Over Documentation: Underwriting focuses on the last 90 to 120 days of actual revenue rather than years of historical tax returns or audited financial statements.

- Deposit Volume and Frequency: The number of monthly deposits and total gross volume are the primary metrics used to determine a business’s ability to support a payroll line.

- Debt-to-Income Calculation: The maximum credit limit is calculated by taking average monthly deposits and subtracting any existing unsecured loan payments.

- Funding Speed: This streamlined evaluation process allows for pre-approvals within hours and final funding for payroll needs in as little as one business day.

Revenue-Based vs. Traditional Bank Underwriting

A revenue-based line of credit is different from a traditional line of credit from a bank or the SBA. Banks and SBA working capital credit lines focus on your credit, tax returns, business and personal bank statements, as well as financial documents such as balance sheets and profit and loss statements. Unsecured lenders focus on your last 3 to 4 months of revenue and the overall health of your business to determine your eligibility. This makes for a more streamlined underwriting process that results in quick funding.

Deposit Activity and Banking Behavior

Underwriters focus on factors such as your deposit frequency and your banking activity. Consistent deposits and stable cash flow indicate your business is able to handle ongoing expenses such as payroll. Frequent deposits throughout the month can increase your overall chances of approval. Strong banking activity minimizes your risk profile and also demonstrates your ability to maintain a payroll line of credit long-term.

Approval Amount Based on Revenue

The total monthly deposit volume is the primary indicator of how much working capital the business can afford to borrow. Your approval is based on the last 3 to 4 months of your gross deposits, less any other unsecured loans that you may have. Regardless, stronger revenue can unlock a higher credit line. This type of revenue-based approach allows contractors to quickly access capital for payroll even when banks turn you down.

Secured vs Unsecured Payroll Line of Credit for Contractors

Secured Payroll Revolving Line of Credit

A secured credit line for contractor payroll requires that you pledge collateral such as real estate with equity or heavy-equipment. This is one of the most cost effective approaches to obtaining a line of credit for your business. Banks will typically loan you around 80% LTV for real estate and much less for heavy-equipment. The greater value of your collateral the more the bank is likely to loan.

A secured credit line does require more extensive documentation such as tax returns and financial statements. Real estate appraisals are required for any secured loans that are tied to some sort of property. This can take weeks, sometimes even months for completion. The biggest downside to this type of loan is that your asset or property can be seized in the event of a default. It is best to use an unsecured loan before you put your home up for collateral.

Unsecured Payroll Revolving Line of Credit

An unsecured payroll credit line does not require that you pledge any collateral. This type of lending relies on your gross revenue over the last 3 to 4 months vs. tax returns and financial statements or credit. This allows contractors with strong cash to be eligible for approval even if they do not meet traditional banking requirements. This type of speed and flexibility allows contractors to access funds for urgent payroll or even 941 tax obligations.

Unsecured lines require minimal documentation such as a completed credit application and business bank statements. You do not have to pledge any collateral or wait for lengthy appraisals to be completed. This easy process allows for fast approvals and quick access to funds when you most urgently need it. In my opinion, this reduces the hassles associated with borrowing making it easier for contractors to secure payroll funding without any delays.

Key Differences

The biggest difference between a secured and unsecured line of credit is the way the payment is structured. A traditional bank line of credit allows you to pay interest only payments every month until you are able to pay down the line and draw again. An unsecured credit line for payroll requires that you make a principal and interest payment for each draw that you make.

Traditional secured bank lines of credit also offer the lowest rates, however, there is risk to your assets. Alternative unsecured credit lines do not require collateral but come with a higher cost. Your credit line is based around the value of your pledged collateral for a secured loan. On the other hand, an unsecured loan is based around your revenue and only limited by your gross monthly deposits.

Payroll Line of Credit for Contractors Requirements and Qualifications

Key Takeaways

- Revenue Benchmark: A minimum of $15,000 in monthly gross deposits over the last 90 to 120 days is required to establish the borrowing base.

- State-Specific Compliance: Borrowers in New York and California must provide four months of bank statements to meet local regulatory standards.

- Deposit Diversity: Lenders require at least five deposits per month to confirm revenue is diversified and not reliant on a single source.

- Banking Health: Maintaining fewer than five NSF events and strong average daily balances is critical for securing lower factor rates and higher limits.

- Credit Flexibility: While a 550 FICO score is the minimum entry point, scores above 600 can unlock better repayment terms and lower costs.

Revenue Requirements and Approval Amount

Revenue is one of the primary factors underwriters review when you apply for a contractor’s payroll line of credit. You will need a minimum of $15,000 per month in gross deposits over the last 3 to 4 months to be eligible for consideration. Underwriters will review the last 4 months of deposits for borrowers in New York and California in order to comply with state regulations.

The amount of your credit line is based on the average of those deposits, less any outstanding loan obligations that you may already have. The following example will help you clearly understand how it works:

- Month 1: $75,000

- Month 2: $63,000

- Month 3: $84,000

- Average: $74,000

Your approval will be based around $74,000 or less, depending on your outstanding liabilities as well as the overall health of your banking activity. Consistent deposits, strong average daily balances, and low NSF activity are viewed as favorable and will help you unlock the highest approval amount. Any existing loans or positions will be deducted from your average to determine the final amount. You can have multiple positions or loans so long as your revenue supports the additional payment.

Deposit Frequency

Your deposit frequency refers to the number of monthly deposits you receive from your customers. You will need to make a minimum of 5 deposits per month or more in order to be eligible. Your customer base is viewed as more diversified when you have more frequent deposits. Fewer than 5 monthly deposits increases your risk profile and may result in a denial. Consistent activity shows that your business is actively generating revenue rather than relying on only one or two payments per month.

Banking Activity Requirements

Underwriters also review the activity within your bank statements in order to evaluate your qualifications. Maintaining strong average daily balances shows that your business has good cash flow and that you are able to manage it responsibly. You will also need to have strong beginning and ending balances, as well as minimal NSF activity. You should aim for 5 NSF charges or fewer in order to get the best rates. More than 5 NSF charges can result in a higher factor rate, and excessive NSF charges are a common reason for denial. Clean banking activity results in better approval odds and lower overall finance charges.

Time in Business

You will need a minimum of 6 months in business to meet the requirements. Two years or more in operation is preferred and typically helps you qualify for better programs with higher limits and longer terms. Your risk profile reduces the longer you are in business, which demonstrates your ability to complete projects and work through delays as well as market fluctuations.

Credit Requirements

You will need a minimum credit score of 550 to apply for a payroll working capital line of credit. Borrowers with a 600 or better FICO score will qualify for superior programs. While underwriters focus primarily on your revenue rather than your credit, your score still impacts the cost. Bad credit borrowers are not excluded from approval; however, they will be subject to higher rates. Those with higher credit scores will qualify for lower finance costs, longer terms, and greater approval amounts.

Existing Loans or Positions

You may still apply for a payroll line of credit even with existing debt or position obligations. You are only limited by the amount of revenue that your business generates. Certain programs do require that you have no more than two existing positions; however, you may still qualify for other programs as well. Keep in mind that your risk profile increases with each additional position, which in turn increases your borrowing costs.

Factor Rates, Payment Terms, and Repayment Frequency for Payroll Line of Credit

Key Takeaways

- Multiplier-Based Cost: Alternative lenders use factor rates, such as 1.20x, rather than traditional accruing interest to determine the total cost of a specific draw.

- Draw-Specific Charges: Finance charges are only applied to the capital actually used, not the total limit of the credit line.

- Flexible Term Lengths: Repayment windows typically span 3 to 24 months, allowing contractors to balance lower payments against total borrowing costs.

- Risk-Adjusted Frequency: Payment schedules, including daily, weekly, or monthly options, are determined by FICO score and the consistency of daily bank balances.

Factor Rates for Payroll Line of Credit for Contractors

Alternative lender loans differ from traditional loans in that they do not use interest to calculate your finance charges. Bank and SBA loans charge interest which accrues either daily or monthly on any unpaid balances. Alternative lenders charge a factor rate, which is based on a straight integer-based calculation that uses a “multiplier” against the specific loan amount. Typical factor rates range from approximately 1.20 to 1.45 or higher, depending on your business and credit profile. This cost is only applied per draw and not to the entire credit line.

Payment Terms for Payroll Line of Credit for Contractors

Payment terms on a payroll credit line range from 3 to 24 months, depending on your qualifications. Longer terms offer smaller individual payments, but higher total finance charges will apply. Conversely, shorter terms are subject to higher payments but result in lower overall finance charges. It is best to choose the terms that fit most effectively with your specific cash flow needs.

Payment Frequency for Payroll Line of Credit for Contractors

Payment frequency may be daily, weekly, or, in some cases, monthly, depending on your qualifications. Applicants with a credit score of 600 or higher and strong banking activity, such as consistent revenue and healthy positive daily balances, may qualify for more favorable terms, including weekly or monthly payments. Borrowers with credit scores between 550 and 600 or weaker banking activity may be required to make daily payments.

Payroll Line of Credit for Contractors With Bad Credit

Key Takeaways

- Low FICO Entry: Contractors can qualify for a revolving payroll line with a credit score as low as 550, provided their cash flow is strong.

- Revenue-Centric Approval: Underwriters prioritize current banking performance and deposit consistency over historical credit issues.

- Risk-Adjusted Terms: FICO scores between 550 and 600 typically result in higher factor rates and daily repayment schedules.

- Tiered Benefits: Scoring above 600 significantly improves your chances of securing lower rates and transitioning to weekly payments.

Can Contractors Qualify With Bad Credit?

Contractors with bad credit can still apply for a construction company payroll line of credit with a FICO score as low as 550. Unsecured payroll credit lines are based on revenue and your overall banking activity rather than primarily on your credit score. Strong, consistent monthly deposits, as well as regular positive daily beginning and ending balances, show that your business has good cash flow and is able to repay the loan. Lenders focus on your current performance rather than past credit issues when making an approval decision.

How Bad Credit Affects Terms

Bad credit does not affect your ability to apply for a construction company payroll line of credit. Those with FICO scores between 550 and 600 are eligible to be considered for approval. However, borrowers with credit scores in this range will typically pay a higher factor rate and receive less favorable terms. Lower credit tier borrowers may also be approved for daily payments as opposed to weekly. Fair credit borrowers whose FICO scores fall between 600 and 650 will qualify for better programs with improved rates and terms. Those with fair to good credit will also have a greater chance of qualifying for a weekly payment.

How to Apply for Payroll Line of Credit for Contractors Same Day Funding

Key Takeaways

- Streamlined Documentation: Initial review requires only a brief credit application and the last 3 to 4 months of business bank statements.

- Verification Tools: Underwriters use DataMerch to check industry payment history and DecisionLogic for real-time bank verification.

- Operational Focus: The merchant interview is a 5-minute final step to confirm that funds will be used for legitimate business purposes.

- Same-Day Deadlines: To receive funds by same-day wire transfer, all steps, including the interview, must be completed before the 4:00 PM ET cutoff.

Submit Credit Application

Your first step is to submit a brief online credit application. You will need to provide basic information such as your business name and address, personal details, time in business, Social Security number, and Federal EIN. You will also need to provide ownership details. Borrowers with more than one partner who do not have 51% or more ownership of the business will need to provide information and signatures from additional partners as well.

Submit Bank Statements

Once you have submitted your credit application, you will need to submit the last 3 to 4 months of your business bank statements. Borrowers in New York and California will need to submit the last 4 months of business bank statements to comply with state regulations. You cannot submit personal bank statements or processor statements from platforms like Stripe or PayPal. It is best to transfer those funds into a regular business checking account if you are using a payment processor to collect from customers.

Receive Pre-Approval

Your documents will go in for pre-approval review once you have submitted your credit application and business bank statements. Should your business meet or exceed the basic requirements, you will typically be sent a pre-approval the same day. This initial offer will include the loan amount, factor rate, length of the terms, and the payment frequency of the credit line.

Sign Documents

Should you accept the offer, the next step toward final funding is to sign the loan documents, typically through DocuSign. You will also need to submit your state-issued driver’s license, a voided check, and, in some cases, proof of ownership. The Articles of Incorporation issued by your Secretary of State contain this information. You can also submit tax documents such as your Form 1040 or K-1 partnership documents.

Final Underwriting Review

Your file will be sent into final underwriting once all loan documents and other requirements are received. At this point, an underwriter will conduct a more thorough investigation into your business and bank statements. A DataMerch search is conducted to review your past payment history. DataMerch is an online resource that tracks your industry-specific payment history.

A DecisionLogic real-time bank verification will also be conducted using a one-time bank connect link. This application allows underwriters to look into your most current month’s banking activity. They will verify that your revenue is consistent with previous months and look for other undisclosed unsecured loans. Additional “positions” not mentioned during pre-approval can cause a denial or changes to your current offer. You must also ensure that your bank account balance is positive and has enough cash to cover at least three payments.

Merchant Interview

A short 5 to 10-minute merchant interview will be conducted once you have passed final underwriting. You will be asked basic questions about your business as well as the intended use of the funds. You may only use your funds for business-related purposes. You will be denied funding should you state any use other than business.

Final Funding

Final funding will happen immediately once you have passed the merchant interview. Your loan proceeds will be sent to your business bank account via same-day wire transfer, provided the wire is sent prior to the 4:00 PM ET cutoff. Wire transfers sent after the deadline will be received the next day. Funding sent via ACH typically takes 24 to 48 hours to show up in your account.

Trades That Use Payroll Line of Credit for Contractors

Key Takeaways

- General Contractors: Bridge the gap between milestone progress payments to help in-house crews and subcontractors get paid on time.

- HVAC Specialists: Manage sudden spikes in labor costs during seasonal heat waves or deep freezes without straining operating capital.

- Roofing Professionals: Float payroll expenses while waiting for the multi-stage insurance claim payout process, including ACV and RCV payments.

- Electrical and Plumbing: Cover weekly labor and tax obligations on long-term projects where payment is tied to the final Certificate of Occupancy.

- Landscaping Crews: Maintain consistent weekly payroll while navigating Net 30, 60, or 90-day commercial contract payment cycles.

General Contractors

General contractors can use a construction company payroll line of credit to manage payroll for in-house workers or subcontractors when waiting on customer payments. General contractors who work on multiple jobs at once can ensure they always have cash ready to pay employees while waiting on the next milestone progress payment. A payroll credit line ensures that jobs remain on schedule and prevents costly delays.

HVAC Contractors

HVAC contractors are subject to seasonal peak demands that can be driven by extreme weather in the summer and winter. A summer heat wave can create sudden demand, requiring A/C contractors to hire additional technicians to cover these spikes. A payroll line of credit for HVAC contractors can help manage those increased costs so your business can cover the surge in labor expenses.

Roofing Contractors

A roofing contractor’s workload is also frequently driven by seasonal demand. A hail storm or heavy wind storm can cause major damage to both residential and commercial customers. To handle this workload, roofing contractors must be prepared to work with insurance claims that pay out in stages. A payroll line of credit for roofing contractors gives your business access to the capital it needs to take on these high-volume jobs.

Electrical Contractors

Commercial and government projects often require that electrical contractors work with purchase orders that do not pay until the project receives the final Certificate of Occupancy. This process can take weeks or even months. An electrical contractor’s line of credit for payroll can help cover your payroll expenses so your business can take on multiple projects at once.

Plumbing Contractors

Plumbing contractors can use a construction company line of credit to bridge the gap between receiving customer payments and outgoing business expenses. Large commercial and government projects also require that plumbers work with purchase orders that pay when the project receives its final Certificate of Occupancy. This can take several weeks to many months. A payroll line of credit for plumbing contractors can help your business cover your payroll and tax obligations while you wait for final payments.

Landscaping Contractors

A landscaping contractor’s revolving payroll credit line can help keep your crews paid when working on multiple jobs. Commercial landscaping contracts are also sometimes subject to Net 30, 60, or 90-day terms. This can create significant cash flow gaps when trying to cover payroll expenses. A landscaping contractor’s line of credit helps your business manage multiple jobs and keeps your crews paid at all times.

How Contractors Use Payroll Line of Credit to Manage Cash Flow

Key Takeaways

- Operational Stability: Bridges the critical gap between project milestones and weekly payroll deadlines, helping ensure fieldwork never grinds to a halt.

- Diversified Funding: Ideal for projects that use purchase orders or government contracts, where payment is often delayed until 30, 60, or 90 days after completion.

- Growth Readiness: Provides immediate liquidity needed to scale the workforce quickly for large-scale projects without waiting for existing receivables to clear.

- Morale Retention: Eliminates the risk of missed paydays, which is important for maintaining worker trust and preventing labor turnover in a competitive market.

Cash Flow Challenges in Construction Projects

Cash flow is one of the biggest challenges that construction company owners must face. Milestone or progress payments can take weeks or months, depending on the complexity of the project. In some cases, contractors bid for projects that issue purchase orders. These types of jobs are not paid until completion and, in some cases, even 30, 60, or 90 days after the job is done. Delays like these in cash flow can disrupt your operations, making it difficult to meet important obligations such as payroll. A payroll credit line for a construction company can help stabilize your cash flow and ensure that your labor costs are covered.

Payroll Stability for Contractors

A contractor’s payroll working capital credit line ensures that your workers are paid on time every week or bi-weekly. Workers rely on payroll from their employer to make ends meet for themselves and their families. Ensuring that you have money every time your employees are paid preserves worker morale and prevents costly delays that can damage client relationships.

Scaling Workforce With a Payroll Line of Credit

A payroll line of credit for your construction company allows your business to take on larger projects and hire the additional workforce needed to complete the work. Use your revolving credit line to increase your revenue and hire the additional workforce required. Flexibility of this type allows for operations to scale more easily during peak seasons or when working on multiple projects simultaneously.

Managing Payment Gaps Between Receivables and Payroll

Contractors often must deal with delayed payments due to the completion of project milestones or waiting on invoice payments. A contractor’s line of credit can help bridge the gap between payments and payroll by giving your business the working capital to meet demands. Access to fast working capital helps your business operate smoothly when receivables exceed cash on hand.

From $25K to $500K+: Choosing the Right Construction Line of Credit

$25,000 Contractor Credit Line

If your business generates at least $25,000 a month in deposits, this revolving line is built for you. It handles smaller material orders and keeps operations moving while you wait out client payments. See how it works and apply for an unsecured contractor loan from $25K to $250K.

$50,000 Construction Company Line of Credit

Perfect for trade and roofing firms clearing $50,000 or more per month. Use this capital to pull the trigger on bulk material buys—like Owens Corning shingles or structural steel beams—to protect your margins. Read how to apply for a no-doc $50,000 unsecured loan for your construction company.

$100,000 Credit Line for Contractors

Built for mid-sized commercial work and large residential projects. This limit gives you the breathing room to absorb sudden payroll spikes, carry bulk inventory, and float costs across multiple jobsites at once. View our criteria for a $100K construction loan with no-doc working capital.

$250,000+ High-Limit Contractor Line of Credit

Geared toward established firms hitting $250,000+ in monthly revenue. This tier gives you the explicit leverage needed to mobilize quickly, secure larger contract bids, and keep your cash flow fluid on high-value jobs. Get details on a $250K unsecured construction company working capital loan.

$500,000+ Ultra-High-Limit Construction Business Line of Credit

Reserved for large-scale contractors hauling in $500,000 or more every month. This elite tier provides massive liquidity to fund heavy material outlays, backstop major municipal or commercial mobilization costs, and manage multiple developments without tapping your cash reserves. Check your eligibility for our $500K contractor working capital loans.

Frequently Asked Questions (FAQ)

What Is a Payroll Line of Credit for Contractors?

An unsecured line of credit for payroll is a revolving source of capital that works just like a credit card. You are allowed to borrow up to your credit limit, repay what you have borrowed, and continue to draw again. This type of product can be used to cover cash flow gaps caused by a variety of purposes.

Can I Get a Payroll Line of Credit With Bad Credit?

Yes. FlexLendCapital.com has a variety of programs available for contractors with credit scores as low as 550. Your approval is based on your revenue and over all cash flow.

How Much Can I Qualify for on a Contractor Payroll Credit Line?

Your approval is based on the average of your last 3 to 4 months of deposits less any existing unsecured loan obligations that you may have. Approvals for borrowers in NY and CA are based on 4 months of business bank statements and gross deposits.

How Fast Can I Receive Funding?

You can receive your funding in as little as 24 to 48 hours, or less so long as you meet all requirements. Funds are transferred via same day wire transfer or next day ACH.

What Documents Are Required to Apply?

Most lenders require a completed credit application and the last 3 to 4 months of business bank statements. Additional documents may include a driver’s license, voided check, and proof of business ownership.

What Are the Requirements for a Payroll Line of Credit?

You need at least $15,000 in gross monthly deposits, as well as a minimum of 6 months in business, at least 5 monthly customer deposits, and a credit score of 550 or higher. You will also need to demonstrate responsible cash flow management.

Can General Contractors and Subcontractors Use a Payroll Line of Credit?

Yes. General contractors, HVAC contractors, roofers, electricians, plumbers, landscapers, and other trade contractors frequently use payroll credit lines to cover labor expenses while waiting for customer payments, milestone draws, or final project completion.

Author Bio:

Robert “Todd” Holliday is a construction financing specialist with over two decades of combined experience in the construction and alternative lending sectors. Since 2020, he has facilitated millions of dollars in capital for contractors across the U.S., helping them navigate the complex cash flow cycles of the modern industry. As the former founder of ShadeIt, LLC (2004–2005), a commercial and residential tension shade fabricator, Todd possesses the unique “boots-on-the-ground” perspective required to understand the real-world financial pressures of materials, payroll, and project delays. He now leverages that expertise to bridge the gap between construction firms and the best available 2026 funding options.

Financial Disclaimer

The information provided in this guide is for educational and informational purposes only and does not constitute professional financial, legal, or tax advice. Loan rates, terms, and SBA program guidelines mentioned are based on early 2026 market projections and are subject to change without notice based on lender criteria and Federal Reserve policy. Qualification for any construction loan product depends on individual business factors, including credit score, annual revenue, and time in business. We recommend consulting with a certified financial advisor or a qualified tax professional before entering into any credit agreement.