Overview

- Revenue-Generating Expenses: Use funding for payroll, materials, mobilization, or urgent job-related expenses that help generate revenue.

- Costs to Avoid: Avoid using funds for personal costs, speculative projects, or non-essential overhead that does not directly support active work.

- Best Fit for Contractors: These loans are best suited for contractors with steady cash flow, active projects, and a clear plan for repayment.

Why Contractors Look for No-Doc $50,000 Working Capital

If you need to apply for a no-doc $50,000 construction company loan, you are already looking for a fast, convenient solution. Every contractor and subcontractor needs working capital to cover business expenses in times of expansion. Cash-flow gaps caused by customer payment cycles can leave any HVAC, electrical, or general contractor looking for financing. Oftentimes, a $50,000 unsecured no-doc loan is just enough liquidity needed to cover your payroll, 941 payroll taxes, and materials when receivables are strong but cash is weak.

How No-Doc Loans Differ From Traditional Bank and SBA Financing

Traditional SBA or bank loans require extensive documentation such as personal and business tax returns, personal and business bank statements, profit and loss statements, balance sheets, and other stipulations that may arise. A no-doc $50,000 unsecured construction company loan only requires three to four months of business bank statements and a completed credit application.

What You Will Learn in This Application Guide

As a former business owner, I understand the importance of access to quick working capital. Projects come around, timelines can’t wait, and quite frankly, no one wants to be poked and prodded for a few thousand dollars. In this guide, I will show you how to apply for a no-doc construction company loan and get your business funded quickly in as little as 24 to 48 hours, without submitting extensive documentation or pledging any of your personal collateral.

Why Construction Trades Seek $50,000 Unsecured Loans

Overview

- Payroll Gap Coverage: Payroll gaps from Net 30 to 90 customer payments can force contractors to seek quick working capital to keep crews paid.

- Material Cost Support: Rising material costs and upfront purchases often require fast funding to keep construction projects on schedule.

- Emergency Job Funding: Emergency equipment repairs and crew mobilization for new jobs can make a $50,000 no-doc loan a practical short-term solution.

Payroll Pressure Across Skilled Trades

Contractors and subcontractors are always faced with similar problems, such as sourcing working capital, especially for payroll. Plumbers, landscapers and HVAC contractors must keep their crews working at all times. This means that technicians and workers expect to get paid on a regular schedule even when customers pay net 30 or even net 90. This can create huge payment gaps during which crews need to be constantly fed. This is why many contractors look to see how to apply for a no-doc $50,000 construction company loan.

Material Costs for Trade-Specific Projects

Materials are also in constant demand with prices fluctuating regularly. Your bid reflects one price one day, and the next day that same 4×4 square costs 30% more. Materials need to be purchased in a timely manner—not just to save money at purchase time, but to keep projects moving forward from one phase to the next. A short-term $50K no-doc construction company working capital loan funded in 24 hours can ensure you purchase on time and your crews keep on schedule.

Equipment and Vehicle Repairs by Trade

Electricians, plumbers, HVAC, and even landscaping companies rely on working vans and equipment to get around town and complete jobs. Unfortunately, nothing lasts forever and anything mechanical is going to need maintenance and repairs. It’s just the nature of the beast; there’s no escaping it. A short-term no-doc working capital loan for $50,000 might just be the perfect amount you need to make those repairs in case of an emergency.

Mobilizing Crews for New Jobs

“It takes money to make money” is an age-old adage that also applies towards construction. Governments and commercial contracts often issue purchase orders for large projects. To complete these contracts, you need to hire additional crews and rent equipment. It is at times like these that you need to apply for a quick no-doc $50,000 loan.

What Is a $50,000 Unsecured Loan for Construction Trades?

Overview

- Lump-Sum Cash Deposit: A $50,000 unsecured no-doc loan provides a lump-sum cash deposit with no collateral required, typically backed by a personal guarantee.

- Faster Alternative Funding: Compared to bank or SBA loans, alternative lenders require fewer documents, focus on revenue and bank statements, and can fund approvals in 24 to 48 hours.

- Fixed Repayment Structure: Repayment is based on a factor rate with fixed daily or weekly payments.

- Common Contractor Uses: A $50,000 loan is commonly used to cover materials, payroll, and crew expansion for active construction projects.

Core Structure of an Unsecured Working Capital Loan

A $50k no-doc construction company loan works much like a credit card in that you do not have to pledge any assets against the loan. You do have to provide a personal guarantee, just as you do with any credit card. A home equity loan is an example of a secured loan. Your rates are very low in comparison, however, you could lose your property if you default. Once approved, you will receive a one-time lump sum cash deposit that can be used for any business expenses.

Differences Between Alternative Lenders and Traditional Loans

The major difference between a bank or SBA loan and an unsecured no-doc loan is that traditional loans require extensive documentation and good credit to qualify. The SBA and banks always require that you submit personal and business tax returns and bank statements. They also may require audited financial statements from a certified CPA and a 680 or better credit score.

Alternative lenders require minimal documents to approve. All you need is a completed credit application, the last 3 to 4 months of business bank statements, and basic business verification. At funding, you will have to submit a state-issued driver’s license and a voided business check. You must also have a minimum credit score of 500 to be considered. Streamlined documentation requirements facilitate funding in 24 to 48 hours.

Factor Rates Vs. Interest Rates

The other major difference is that banks charge interest that accrues either daily or monthly. No-doc short-term unsecured loans charge a factor rate to determine the total payback upfront. Your loan is calculated by multiplying the loan amount by a factor, like 1.35. Factor rates can vary depending on your credit and how long you keep the funds. For example, a $50,000 loan with a 1.35 factor rate is calculated by multiplying $50,000 X 1.35, resulting in a total payback of $67,500.

Typical Repayment Terms and Payment Frequency

Terms are approved on a case-by-case basis and can range from 3 to 24 months. However, most contractors will fall between 9 and 15 months. Payment frequency is either weekly or daily and is also determined on an individual basis. Daily payments are typically made Monday through Friday only, excluding bank holidays. To determine what your payment will be, simply divide the total payback by your terms. A $67,500 payback over 48 weekly payments will cause a $1,406.25 payment. Daily payments are calculated the same way.

Why $50,000 Fits Many Construction Trades

$50,000 is an ideal funding amount sought out by general contractors and subcontractors alike. Contractors can use these funds to purchase materials, such as shingles for a roofing contractor or 4×4 square tubing for a welder. HVAC contractors can use a $50K no-doc short-term working capital loan to hire additional crews during the peak summer or winter months. Overall, this amount of funding can provide your business with immediate liquidity when it’s needed most.

Construction Trades That Commonly Qualify for $50,000 Loans

Overview

- Trades That Often Qualify: General contractors, roofers, HVAC, plumbing, and electrical trades often qualify due to steady project revenue and ongoing expenses.

- Common Job-Related Uses: Landscaping, site work, concrete, framing, and specialty trades use $50,000 loans to cover materials, equipment rentals, fuel, and payroll.

- Cash-Flow Gap Support: These loans commonly bridge cash-flow gaps while waiting on Net 30 to 90 payments, helping keep crews working and projects on schedule.

General Contractors and Home Builders

Contractors and home builders regularly apply for a $50,000 no-doc construction company loan to manage multiple facets of the business. Funding is used to pay for permits, hire crews, and purchase kitchen cabinets, concrete, and other business-related expenses. This capital keeps projects moving forward and on time while avoiding costly delays due to a lack of materials or manpower.

Roofing Companies

Roofing contractors commonly apply to cover purchases such as shingles or underlayment. They also use these funds to rent equipment for multiple job sites, pay workers’ compensation insurance, and make sure crews have all the proper safety gear. A $50,000 no-doc short-term loan keeps operations running smoothly and contractors sleeping soundly.

HVAC Contractors

HVAC contractors need financing for inventory and other expenses such as hiring crews. It is essential to keep spare parts in inventory—such as thermostats, R32 refrigerants, capacitors, and other important items that need to be kept on hand. This keeps customers happy and contractors paid. A $50K no-doc working capital loan can provide the cash needed to make these purchases in anticipation of peak demand.

Plumbing and Electrical Contractors

Plumbing and electrical contractors can also benefit from fast unsecured capital. A $50K loan can cover the payroll needed to complete commercial projects while waiting for payment from general contractors and other commercial accounts. Quick access to capital ensures technicians stay dispatched and service calls continue without interruption.

Landscaping and Site Work Companies

Landscaping companies and site work contractors can use these loans to rent equipment like excavators or bulldozers. They can also make purchases like materials and fuel for vehicles. Unsecured loans for landscaping contractors are becoming the lifeline of the construction industry.

Concrete, Framing, and Specialty Trade Contractors

Concrete and framing contractors rely on these loans to keep up with business expenses while waiting on Net 30, 60, or 90-day payment cycles. A $50,000 loan can help bridge the gap between your expenses and payments from customers. This can help provide your business a cash cushion when the ride gets bumpy.

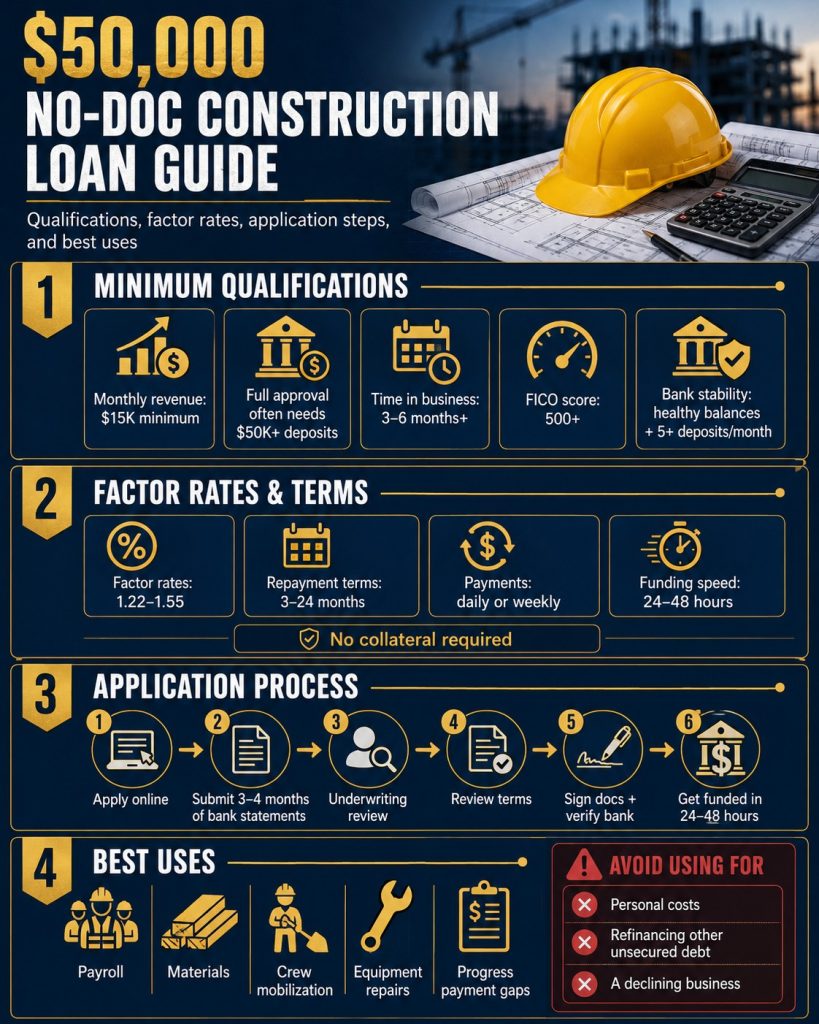

Minimum Qualifications for a $50,000 Trade Contractor Loan

Overview

- Monthly Revenue Requirement: Monthly revenue of at least $15K is required, with $50K+ often needed for full approval, based on the most recent 3 to 4 months of deposits.

- Time in Business: A minimum of 3 to 6 months in business is required, while 2+ years in business typically helps qualify for better rates and longer terms.

- Credit Score Requirement: A credit score of 500 or higher is required, with stronger credit often leading to lower factor rates and better funding offers.

- Bank Statement Performance: Solid bank statement performance, including healthy average daily balances and limited NSF charges, can improve approval strength.

- Consistent Deposit Activity: Consistent deposit activity, ideally 5+ deposits per month, helps show diversified and stable cash flow.

Monthly Revenue Expectations by Trade

To qualify for a $50,000 unsecured no-doc loan, you generally need $50,000 or more per month in gross revenue or deposits. Your approval is primarily based on the average of your last 3 to 4 months of deposits, minus any existing unsecured loan payments. While $50,000 is the target for this specific loan amount, you will need a minimum of $15,000 per month to be considered for funding at all. You can also qualify for multiple loans (or “positions”) if your income supports the additional payment. Trades such as HVAC, roofing, plumbing, and landscaping often meet or exceed these revenue requirements.

Time in Business Across Construction Trades

You will need at least 3 to 6 months in business for consideration. Those with 2 years or more in operation will typically qualify for better rates and terms. Newer businesses will more than likely qualify for shorter terms and higher factor rates. Keep in mind that your business must be in full operation with consistent cash flow moving through your business bank account. A business that was registered 3 years ago but has had no active revenue or cash flow will not qualify.

Credit Score Flexibility for Skilled Trades

You will need a minimum FICO score of 500 to apply for a $50,000 no-doc loan. Alternative lenders focus more on revenue than credit; however, lower credit scores will cause higher factor rates. Bad credit is not necessarily a problem if your business meets the other requirements. Those with excellent credit will be able to qualify for “A” paper rates and terms. I have seen factor rates as low as 1.22 for high-tiered credit contractors.

Bank Statement Strength and Cash Flow Stability

Banking activity, such as your average daily balance and NSF (Non-Sufficient Funds) history, plays a major factor in underwriting. You have a much greater chance of approval with minimal NSF charges and strong beginning and ending daily balances. Underwriters typically do not like to see more than 5 NSF charges in any 3 to 4 month period; excessive charges, such as 10 or more, may completely disqualify your business. You must also show at least 5 customer deposits per month. Having fewer than 5 deposits suggests your business is dependent on too few clients. The more diversified your customer base, the less risky your business profile becomes.

Step-by-Step Process to Get a $50,000 Unsecured Loan

Overview

- Required Documents: Gather the last 3 to 4 months of business bank statements, ID, and a voided check or bank form.

- Simple Online Application: Submit a simple online application with basic business and owner details such as EIN, SSN, and address.

- Revenue-Based Underwriting: Underwriting reviews deposits, revenue, and existing obligations to determine the approval amount.

- Final Review and Verification: Review and sign terms, then complete final underwriting including background check, DataMerch review, and bank verification.

- Funding Deposit Timeline: After a brief merchant interview, funds are typically deposited by ACH or wire within 24 to 48 hours.

Gather Basic Contractor Documentation

Applying for a $50,000 no-doc construction company loan is straightforward. The first thing you will need to gather is your last 3 to 4 months of business bank statements. Residents of New York and California must submit 4 months to follow state disclosure laws. You should also have your state-issued driver’s license or passport ready, along with a voided check. A direct deposit form from your bank can be submitted in lieu of a voided check if necessary.

Submit a Simple Funding Application

You will need to complete a basic credit application with information such as your name, business name, Social Security number, Federal Tax ID (EIN), and business address. This can all be done online via our application portal. Please note that you must submit your business bank statements; personal bank statements cannot be accepted for this program.

Revenue-Based Underwriting Review

The pre-approval process begins once you have submitted all your documents. At this point, underwriting will review your bank statements and gross revenue. The amount financed is based on the average of your last 3 to 4 months of deposits, minus any other existing unsecured loan payments. To qualify for a $50,000 no-doc working capital loan, you will typically need $50,000 or more in monthly revenue—a benchmark easily achievable by many general and trade contractors.

Review Terms and Payment Structure

The next step is to review your specific terms and payment structure. At this stage, you will know exactly how much you are approved to borrow and for how long. You will also see if you are approved for a daily or weekly payment plan. Once you review and approve the terms, you will be sent a contract via DocuSign. This must be returned along with a clear copy of your driver’s license and voided check.

Final Underwriting

Final underwriting is a more thorough process that involves a background check and a review through DataMerch—an industry database that tracks unsecured loan history. Any past defaults linked to your Social Security number will cause a non-approval. You will also be required to connect your bank account via DecisionLogic for real-time verification. Underwriting will review your current activity to ensure it aligns with previous months. Note that any undisclosed loans taken recently can cause a denial if your revenue cannot support the additional payment.

Final Funding

The final step is the Merchant Interview. An underwriter will ask a few brief questions about your business and how you plan to use the funds. It is important to remember that unsecured business loans cannot be used for personal expenses; stating otherwise will cause non-funding. Once you successfully complete the interview, your working capital will be sent via same-day wire or ACH transfer. Depending on the complexity of your file, this entire process can be completed in just 24 to 48 hours.

Can You Get a $50,000 Unsecured Construction Loan With Bad Credit?

Overview

- Revenue-Based Review: Alternative lenders prioritize revenue and bank activity over credit score, with minimum FICO requirements typically starting around 500.

- Cash-Flow Strength: Strong cash flow can help offset bad credit, though higher factor rates are common for higher-risk files.

- Disqualification Factors: Open defaults or active bankruptcies usually disqualify applicants from approval.

Why Alternative Lenders Are More Flexible Than Banks

Bad things do happen to good people from time to time. Issues like divorces, injuries, or even unpaid invoices can cause credit challenges that do not reflect the true strength of a construction business. Fortunately, alternative lenders are typically much more flexible with bad credit than traditional banks. Underwriters tend to value your income and banking performance more than just your FICO score, which makes the process of applying for a no-doc $50,000 unsecured loan far more realistic for active contractors with steady revenue.

Minimum Credit Score and Revenue Focus

In most cases, you will need a minimum credit score around 500 to qualify. Applicants below a 500 FICO score are generally rejected. Even so, lenders place heavy emphasis on revenue and banking activity, including average daily balances, starting and ending balances, the number of NSF charges, and the consistency of deposits. Contractors with strong cash-flow history who meet these requirements are often approved, though they should expect higher factor rates than borrowers with stronger credit. Rates for bad credit, short-term no-doc loans commonly start near 1.40 and can climb to 1.55 or higher depending on the overall risk profile.

Defaults, Bankruptcies, and Starter Loan Options

Borrowers with open defaults or active bankruptcies are usually not eligible for approval. Lenders perform detailed background reviews, often including DataMerch checks, to evaluate past repayment behavior. If prior defaults have been resolved, some lenders may offer a small “starter loan” to rebuild payment history, but these options typically carry very high costs and short repayment terms, sometimes as brief as 30 days.

Best Uses of a $50,000 Loan Across Construction Trades

Overview

- Payroll Support: Cover payroll for crews while waiting on customer invoices or slow-paying commercial accounts.

- Bulk Material Purchases: Purchase bulk materials and maintain inventory to keep active jobs on schedule.

- Cash-Flow Gap Coverage: Close cash-flow gaps between ongoing expenses and incoming customer payments.

- Emergency Repair Funding: Handle emergency equipment or vehicle repairs without delaying active construction projects.

Payroll for Skilled Labor Crews

Contractors and subcontractors use a no-doc $50K unsecured loan for a variety of purposes, most importantly for payroll. Crews have families to feed and expect timely payments; however, customers do not always pay on time, which can interrupt your payment schedules. A no-doc unsecured loan helps cover your payroll obligations while you wait on outstanding invoices to be settled.

Bulk Material Purchases for Active Jobs

Contractors must also purchase materials for active projects and general inventory. HVAC contractors, for example, must maintain specific parts at all times to keep customers happy and service calls moving. A quick, no-hassle $50,000 loan ensures that inventory is always replenished. Having these funds available helps you avoid costly delays and the loss of customers to competitors who can get the job done faster.

Covering Gaps Between Progress Payments

General contractors often work with milestone progress payments, especially on large commercial or government-related projects. A $50,000 no-doc working capital loan can cover your overhead between these milestones, keeping the job moving forward and ensuring the next phase of payments is released on time.

Emergency Repairs and Jobsite Expenses

Construction is never without surprises. Vehicles break down, leaving crews unable to make it to the jobsite. Heavy equipment also requires expensive, unexpected repairs that can stop work in its tracks. Quick access to capital, like a $50K no-doc loan, allows contractors to address these mechanical problems immediately and keep projects on schedule.

When to Use and Not Use a $50,000 Unsecured Construction Loan

Overview

- Cash-Flow Gap Support: Use funding to bridge cash-flow gaps for payroll, materials, and inventory tied to revenue-generating projects.

- Uses to Avoid: Avoid using funds to refinance other unsecured debt, pay credit cards, or cover ongoing losses in a struggling business.

- Income-Focused Borrowing: Only apply when the funds will produce income, support active work, or help complete existing jobs.

When to Apply

You should never apply for a $50K no-doc construction company loan for just any reason. These loans are best for covering cash-flow gaps between your business expenses and customer payments. This type of short-term working capital is ideal for covering payroll or purchasing materials and inventory. You should also consider this type of capital for business expansion purposes, such as bidding on government projects that are awarded on a purchase order basis. Ultimately, the loan needs to either generate new income or help you complete ongoing work that is already under contract.

When to Walk Away

You should never use this type of loan to pay off credit cards or other unsecured loans. I never advise merchants to take out one loan to cover another’s interest and principal; the math is simply not in your favor. Furthermore, never use a $50k no-doc construction company loan as a “Hail Mary” to keep a failing business from closing its doors. At that point, it is better to look for other means to stay afloat or simply step away. It is not worth the extra stress or a default that would prevent you from securing future loans when you’re ready for a fresh start.

Frequently Asked Questions (FAQ)

Can I get a $50,000 construction loan with no tax returns?

Yes. These are revenue-based loans. Lenders qualify you based on your last 3–4 months of business bank statements rather than tax returns or profit-and-loss statements.

What is the minimum credit score required?

You typically need a 500 FICO score or higher. While bad credit isn’t a dealbreaker, a higher score (650+) will get you lower factor rates and longer repayment terms.

How fast can I get the $50,000?

The process is built for speed. Most contractors receive an approval within hours and have the funds deposited in 24 to 48 hours after the final merchant interview.

Is collateral like trucks or equipment required?

No. These loans are unsecured, meaning you don’t pledge equipment or real estate. However, a standard personal guarantee is required, similar to a business credit card.

How much revenue does my trade business need?

To secure a full $50,000, lenders usually look for $50,000+ in average monthly deposits. The minimum revenue to be considered for any amount is typically $15,000 per month.

What are common uses of these funds?

Most contractors use the $50k to bridge 30- to 90-day payment gaps, cover weekly payroll, buy bulk materials upfront, or mobilize crews for new commercial projects.

Author Bio:

Robert “Todd” Holliday is a construction financing specialist with over two decades of combined experience in the construction and alternative lending sectors. Since 2020, he has facilitated millions of dollars in capital for contractors across the U.S., helping them navigate the complex cash flow cycles of the modern industry. As the former founder of ShadeIt, LLC (2004–2005), a commercial and residential tension shade fabricator, Todd possesses the unique “boots-on-the-ground” perspective required to understand the real-world financial pressures of materials, payroll, and project delays. He now leverages that expertise to bridge the gap between construction firms and the best available 2026 funding options.

Financial Disclaimer

The information provided in this guide is for educational and informational purposes only and does not constitute professional financial, legal, or tax advice. Loan rates, terms, and SBA program guidelines mentioned are based on early 2026 market projections and are subject to change without notice based on lender criteria and Federal Reserve policy. Qualification for any construction loan product depends on individual business factors, including credit score, annual revenue, and time in business. We recommend consulting with a certified financial advisor or a qualified tax professional before entering into any credit agreement.