Key Takeaways

- Bridging the Gap: Revolving credit solves the Net 30, 60, or 90 delay by providing immediate cash to cover upfront costs while you wait for customer payments.

- Operational Continuity: These funds ensure critical expenses, like weekly payroll and 941 taxes, are met, preventing project delays or labor issues.

- Revenue-Based Funding: Approval is tied to your business cash flow rather than just a credit score, allowing for funding in as little as 24 to 48 hours.

- Scaling Potential: Access to ready capital allows you to bid on larger projects or manage multiple jobs simultaneously without draining your personal bank account.

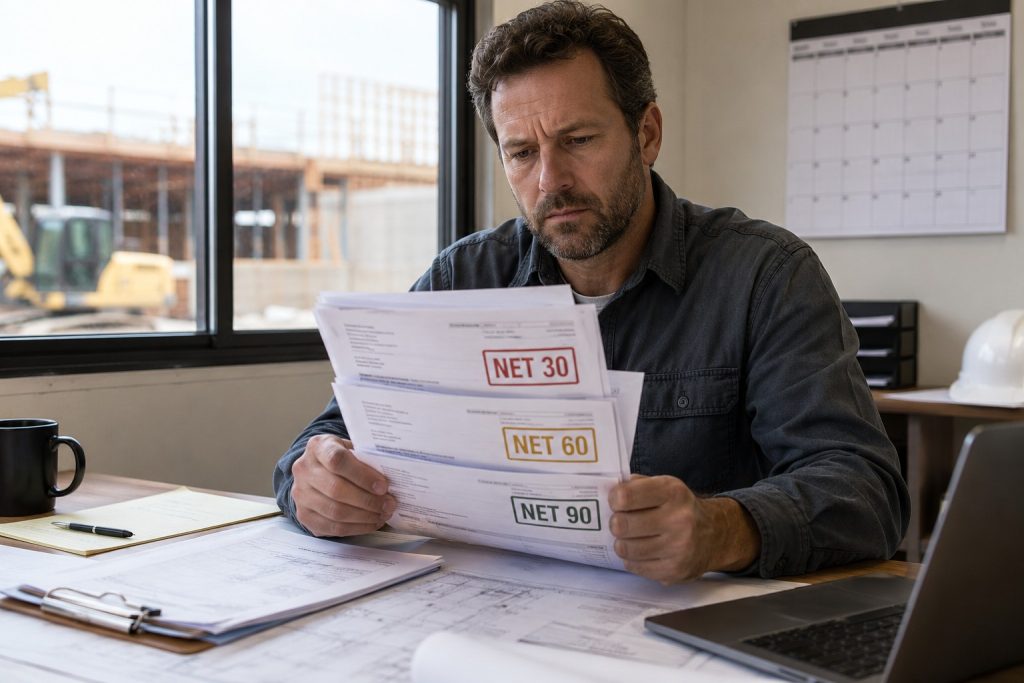

Cash Flow Gaps From Net 30, 60, and 90 Day Payment Terms

A construction working capital credit line for contractors can provide the liquidty you need to fund your latest project or bridge the gap between customer payments and expenses. Contractors are often required to work with Net 30, 60, or 90 day terms. Other projects might pay with progress or milestone payments. As a contractor, you must pay expenses upfront prior to getting paid, which can create gaps in your cash flow that can become difficult to manage.

How a Revolving Line of Credit Provides Liquidity

A revolving line of credit can help provide your business with liquidity when customer receivables exceed the cash in your bank account. You can access these funds to pay everything from payroll and 941 payroll taxes to materials, workers’ compensation insurance, equipment rental, or just about any business-related expense. You can use your funds to keep your crews working and materials delivered to the job site on time, preventing delays that could affect your payment. This will ensure your business maintains steady cash flow and meets critical obligations on time.

Real-World Perspective From a Business Owner

As a business owner, I understand the importance of having cash flow. Running a construction business is not without its challenges. There are lots of problems to deal with; working capital should not be one of them. In this guide, I will show you how you can apply for a construction business line of credit and get funded in as little as 24 to 48 hours. In it, you will learn how revenue-based underwriting works, qualification requirements, factor rates, payment terms and frequency, and how you can use your revolving credit line to scale your business.

Revenue-Based Construction Working Capital Credit Line

Key Takeaways

- Cash Flow Focus: Underwriters prioritize your actual bank deposits from the last 90–120 days over historical tax returns, allowing them to fund your current growth rather than your past performance.

- Approval Math: Your average monthly deposits serve as the primary benchmark for your credit limit. Generally, the more you deposit, the higher the limit you can unlock.

- Banking Hygiene: To secure the best terms, maintain positive daily balances and keep NSF activity to a minimum, as these are the top indicators of cash flow health.

- Speed of Execution: By removing the requirement for audited financials and collateral, the process is streamlined for approval and funding in as little as 24 to 48 hours.

How Revenue Determines Approval

Revenue-based underwriting for a construction line of credit is focused on your gross deposits over the last 3 to 4 months, rather than your tax returns and personal credit. Your bank deposits give underwriting a clear picture of how you manage your cash flow. Lenders look for stable and consistent deposits, positive daily balances, and limited NSF activity to determine your eligibility. In addition, your average monthly deposits will determine how much your business will qualify for. The greater your deposits, the higher your credit limit will be.

Why Deposits Matter More Than Tax Returns

Traditional bank and SBA loans require extensive documentation, such as the last 3 years of tax returns, personal and business bank statements, profit and loss statements, balance sheets, and your credit score. Alternative lenders do not have to abide by the same underwriting guidelines and therefore focus more on your gross deposits and your cash flow to determine if your business will be able to make the loan payment.

This approach reduces the amount of documentation as well as the time needed to get funded. This allows you to focus on your business and not bank stipulations. The elimination of excessive documentation and the need for collateral allows for approval and funding in 24 to 48 hours, and sometimes less.

Secured vs Unsecured Construction Working Capital Credit Line

Key Takeaways

- Asset Requirement: Secured lines require pledging high-value collateral like real estate or heavy equipment, while unsecured lines are based entirely on your 90-day revenue performance.

- Funding Velocity: Unsecured lines bypass the lengthy appraisal process, offering access to capital in 24 to 48 hours compared to the weeks or months required for secured bank products.

- Payment Structure: Secured lines often allow for interest-only payments, whereas unsecured lines typically require a combined principal and interest payment for every draw.

- Risk and Cost Trade-off: Secured options provide the lowest rates but put your physical assets at risk. Unsecured options carry higher costs but protect your property from seizure in the event of a default.

Secured Line of Credit for Contractors

A secured construction business line of credit requires that you pledge some form of collateral in the event of a default with your loan. This means that you need to commit something such as real estate or heavy equipment that can be sold to cover your loan if you fail to pay. Banks usually take 80% loan-to-value (LTV) on real estate and much less on equipment. This means that your credit line is based on how much collateral you are able to pledge. For example, $500,000 of property equity may unlock a $400,000 credit line. This type of arrangement gives you the best rates and allows for much longer repayment terms. This option is best for those with sufficient collateral to unlock the capital needed.

This process is much slower based on the extensive documentation required as well as appraisals. Underwriters require items such as tax returns, bank statements, and property valuations. Appraisals can take weeks or sometimes months to complete. These delays can prevent you from accessing capital when you need it most.

Unsecured Line of Credit for Contractors

An unsecured construction business line of credit for contractors does not require that you pledge any type of collateral such as real estate. Unsecured lenders are not regulated by the same underwriting restrictions as traditional loans. Underwriters focus more on your revenue and your last 3 to 4 months of gross deposits to your business bank account. These types of loans offer the fastest time to funding as compared to a secured credit line.

Key Differences

The most significant difference is that a secured line of credit will allow you to make interest-only payments until you pay down the line either partially or 100%. An unsecured line of credit requires that you make a principal and interest payment for each draw that you make. Secured lines are tied to asset value and offer lower costs, while unsecured lines are based on cash flow and provide faster access to capital at a higher cost.

Construction Working Capital Credit LineRequirements and Qualifications

Key Takeaways

- Revenue Floor: A minimum of $15,000 in monthly gross deposits over the last 90–120 days is required to establish your borrowing base.

- Deposit Diversity: You must show at least five deposits per month to prove your revenue comes from multiple customers, reducing “single-source” risk.

- Banking Hygiene: Maintaining a positive daily balance and keeping NSF activity under five incidents per month is critical for securing the lowest factor rates.

- Credit Accessibility: You can qualify with a FICO score as low as 550, though scores above 600 unlock significantly better terms and higher limits.

Revenue Requirements and Approval Amount

A contractor’s payroll line of credit requires underwriters to look at the revenue of each applicant. In order to qualify, an applicant would have to have at least $15,000 a month in gross deposits within the last three to four months. Applicants within the states of New York and California should have the past four months of deposits prepared for underwriters to review.

Unless an applicant has other outstanding loans, an underwriter can determine the credit line based on these deposits. The example below shows how this process would work:

- Month 1: $95,000

- Month 2: $82,000

- Month 3: $91,000

- Average: $89,000

Although the final approval does depend on any existing liabilities as well as the applicant’s banking habits, this would normally result in a credit line of $89,000 or less. In order to get the highest approval amounts, applicants must have high average balances, consistent deposits, and minimal NSF activity. Existing loans or positions will be subtracted from the average, but it is okay for an applicant to have other loans as long as the company’s revenue can handle it.

Deposit Frequency

Underwriters also observe deposit frequency, which refers to how many customer payments a business receives per month. To be eligible, a business must have at least five deposits per month. It looks better for a business to have more deposits because it shows a diversified client base. This shows underwriters that the business doesn’t just rely on a few big payments a month. Without the minimum of five deposits a month, an applicant is at risk of denial.

Banking Activity Requirements

Underwriters also view a business’s average banking activity as a metric for approval. Consistently having high daily balances displays to underwriters that the business owner can oversee the company’s cash flow. It is important to have minimal non-sufficient funds incidents and retain high beginning and ending balances. For the best rates, a business should have no more than five NSF incidents. Excessive activity usually leads to application denial or significantly higher financing costs. Ultimately, the cleaner a business’s banking activity appears to be, the more likely it is to get approved with the lowest finance charges.

Time in Business

The amount of time a company has been in operation is another aspect underwriters look at for eligibility. A minimum of six months is necessary for approval. However, businesses that have been operational for two years or more usually qualify for more exclusive programs with greater limits and better terms. A longer history reduces the business’s risk profile and demonstrates to lenders that the contractor in charge can successfully complete projects despite market fluctuations or delays.

Credit Requirements

While revenue is the main focus of underwriters, a credit score of at least 550 is necessary to apply. Additionally, a score of 600 or higher allows access to better programs. While a lower score won’t automatically disqualify an applicant, it will result in higher rates. A strong credit score leads to lower costs, larger approval amounts, and extended terms.

Existing Loans or Positions

Existing loans or positions do not prevent a contractor from applying for this type of loan. However, the total amount of funding is limited by the revenue the business generates. Some specific programs restrict the borrower to a maximum of two active positions, but there are others that do not. Borrowers should always be aware that taking on multiple positions increases their financial risk and will lead to greater overall borrowing costs.

How to Apply for Construction Working Capital Credit Line

Key Takeaways

- Application Readiness: Having your last 4 months of business bank statements and a voided check prepared can reduce approval time to under two hours.

- Verification Standards: Lenders utilize DecisionLogic for real-time bank verification and DataMerch to check for prior payment history or defaults.

- Funding Deadlines: To receive a same-day wire transfer, the merchant interview and final paperwork must be completed before the 4:00 PM ET banking cutoff.

- Business Purpose Compliance: The merchant interview is a mandatory step where you must confirm that the capital is for business use only to avoid an immediate denial.

Submit Credit Application

To start the process for a construction line of credit, contractors must fill out an online application. This first step gathers all the necessary details including the contractor’s full name, the official name of the business, and a contact phone number. The contractor will also be required to provide specific information regarding the contractor’s business story, including how long the business has been operational, and other essential personal and professional data.

Submit Business Bank Statements

As a part of the online application, contractors are required to upload business bank statements covering the last three to four months. For contractors operating in New York or California, state laws require the submission of the last four months of records. It is important to note that statements from platforms like Stripe or PayPal are not allowed for this step. A verified business bank account is a prerequisite for moving forward in the approval process.

Receive Pre-Approval Offer

Typically, contractors can expect to receive a pre-approval notification within a few hours, though the time varies based on the intricacy of the financial records. This offer will provide a breakdown of the potential loan amount, the associated factor rate, and how often payments will be required. With this information, the contractor can evaluate the total costs and expected return on investment. If the business does not meet the necessary qualifications, the contractor will be informed and may submit a new application after a three-month period.

Sign Documents

Once the contractor has officially accepted the terms, they will be sent the formal loan documents. The signing process can be completed through any online electronic signature platform like DocuSign. With the signed documents, the contractor must also provide a valid state-issued ID and a voided check for the business account. Depending on the specific application, contractors might also be asked to submit further paperwork like the business’s articles of incorporation or the contractor’s personal IRS Form 1040.

Final Underwriting Review

After all the required documents have been submitted, the application will go into a final underwriting stage. This involves an extensive examination of the business’s professional operation and banking history. Underwriters use the program DataMerch as a standard industry tool to verify payments to previous unsecured lenders.

Additionally, the contractor will be required to connect the business account to DecisionLogic, which allows underwriters to view a real-time assessment of the current month’s banking activity. This simply confirms that the business’s revenue is stable and can also view any previous loans that were not disclosed. If previous debt is discovered at this time, it can increase the total price or lead to denial. Additionally, the account must have a positive balance and show sufficient funds to cover at least three of the scheduled payments.

Merchant Interview

A mandatory merchant interview is required to take place before the loan is allowed to be released. During this short five- to ten-minute conversation, an underwriter will ask specific questions as to how the contractor intends to use the funds. This is to confirm that the credit line will be used only for business purposes and not for any personal expenses. It is important for the contractor to be transparent because any indication that the funds will be used for personal reasons will result in denial.

Final Funding

After a successful merchant interview, the funding will be sent that same day. They are delivered via a same-day wire transfer, which usually arrives on the day it is sent as long as the transfer occurs before the 4:00 PM ET cutoff. Transfers sent after this time will usually be available the next business day. If the contractor chooses an ACH transfer, it is important to keep in mind that they typically take twenty-four to forty-eight hours to appear in the business account.

Factor Rates, Payment Terms, and Repayment Frequency

Key Takeaways

- Fixed Cost Capital: Factor rates provide an upfront cost calculation, allowing you to build the exact expense of the capital into your project bids.

- Pricing Drivers: Your rate is driven by banking stability, with high daily balances and clean NSF history directly translating to lower multipliers.

- Duration Flexibility: Terms range from 3 to 24 months, giving you the ability to align your repayment schedule with the expected payout of your purchase order.

- Cash Flow Matching: Repayment frequency is tailored to your revenue cycle to ensure the debt service does not strain your operational liquidity.

Factor Rates

Alternative lenders calculate your overall finance charges based on a factor rate. Traditional lenders charge interest rates that accrue either daily or monthly. A factor rate is based on a fixed multiplier which is then multiplied by your loan amount in order to determine your finance charges. For example, a $100,000 loan with a 1.35 factor rate will have a total payback of $135,000. Your factor rate is determined by a variety of factors such as your revenue, cash flow, and your credit score. The stronger your business profile, the better your rates will be. Borrowers with low credit scores, NSF charges, and a lower overall business profile score will receive a higher rate. Rates can range anywhere from 1.20 to 1.45 or greater, depending on your qualifications.

Payment Terms

Your payment terms are also approved on a case-by-case basis. Terms usually range from 3 to 24 months depending on your qualifications. The longer your term, the lower your payment; however, overall finance charges will be greater. A shorter term will have a higher payment with the least amount of finance charges. The longer you hold on to the funds, the more expensive it becomes; the shorter the duration, the less expensive your overall finance costs will be. Be sure to align your payment cycles with customer repayment schedules in order to properly service your debt.

Repayment Frequency

How often you will pay is referred to as your repayment frequency. An unsecured working capital line of credit for contractors is either paid daily, weekly, or monthly, depending on approval. Borrowers with good credit, high revenue, and strong cash flow will more than likely be approved for a weekly or even a monthly payment. Borrowers with less than desirable credit and qualifications will more than likely have a daily payment. In addition, those with more than one position or loan will also more than likely have to make a daily payment.

Reasons Construction Working Capital Credit Line Applications Are Denied

Key Takeaways

- DataMerch Tracking: Alternative lenders use a centralized database called DataMerch to track defaults; these records are tied to both your personal Social Security number and your Federal EIN.

- Modification Red Flags: Any deviation from an original repayment plan, even a negotiated “payment arrangement”, is flagged as a modification, signaling cash flow instability to underwriters.

- Entity-Wide Accountability: Defaults or modifications associated with a partner or a previous business you owned can still result in a denial for your current company.

- Banking Activity: Excessive NSF activity, negative daily balances, and low ending balances are primary indicators of a weak risk profile and often lead to rejection.

Defaults (DataMerch)

Past defaults with other lenders is the most common reason for denials that we see with many borrowers. Underwriters use DataMerch, an online resource that tracks your payment history with any other unsecured lenders. Your history is tied to both your Social Security Number and your Federal EIN. This means that you will still be denied funding if you have had any defaults with your current or any other business that you may have owned. This also includes any business owned with any other partners as well. Unfortunately, a past default results in an automatic denial and you are placed on a “blackball” list of borrowers no longer eligible.

Payment Modifications

Payment modifications are another reason we see borrowers being denied funding. A payment modification is any type of payment arrangement that you make with another lender. Any adjustment to your original contract is an indicator that your business has had past problems with cash flow. Underwriters view this as a red flag and it indicates that your business may struggle to meet future obligations. Even if the modification helped you stay current, it still raises concerns about stability.

Weak Bank Activity

Other reasons borrowers are denied are low revenue, excessive NSF charges, as well as inconsistent deposits over the last 3 to 4 months. Lenders look for a minimum revenue amount each month. You will be denied if you do not meet the minimum threshold. Underwriters also look at the overall health of your cash flow. You will also be denied if your business has too many negative days and weak ending balances each month. You will also not be eligible using personal bank statements or processing statements such as Stripe or PayPal. You need to have a proper business bank account and you should transfer your funds into your business account if you are taking payments with a processor such as Stripe or PayPal.

Construction Working Capital Credit Line by Dollar Amount

Key Takeaways

- Revenue Matching: Approval limits typically mirror your monthly gross deposits. If you average $50,000 in monthly revenue, you can generally qualify for a $50,000 line.

- Tiered Eligibility: Your borrowing base scales with your deposits; as your monthly average increases, so does your ability to unlock higher credit limits.

- Commercial Capacity: Lines between $150k and $250k are specifically designed to help subcontractors bridge the gap on large commercial and municipal projects.

- Scalability: High-limit lines allow for the management of multiple simultaneous crews and the procurement of bulk materials without hitting personal credit limits.

$25,000 Construction Working Capital Credit Line

To qualify for a $25,000 construction credit line for contractors, your business needs to generate at least $25,000 per month in gross revenue. This credit line works for contractors and subcontractors who need funds to cover expenses such as materials, payroll, workers’ compensation, or other business-related expenses. Average revenue that ranges between $25,000 and $49,999 will be eligible to apply for a contractors’ line of credit between $25,000 and $49,999.

$50,000 Construction Working Capital Credit Line

To qualify for a $50,000 contractors line of credit, you will need to have at least $50,000 per month in average deposits over the last 3 to 4 months. A $50,000 construction company credit line can be used to cover a wide range of business expenses as well. Average revenue that ranges between $50,000 and $99,999 is eligible to apply for a contractors’ line of credit for up to $99,999.

$100,000 Construction Working Capital Credit Line

In order to apply for a $100,000 construction company line of credit, you will need to have at least $100,000 or more in average gross revenue over the last 3 to 4 months as well. Many small to medium-sized contractors meet or exceed this threshold. You will be eligible to qualify for up to $199,999 should your gross average revenue fall between $100,000 and $199,999 over the last 3 to 4-month period.

$150,000–$250,000 Construction Working Capital Credit Line

To apply for a $150,000 line of credit for contractors, you will need at least $150,000 or more in monthly revenue over the last 3 to 4 months as well. A credit line of $200,000 can be used to work on larger commercial and municipal-type projects. These types of projects often require you to incur upfront expenses such as labor and materials before receiving payment. Your business can qualify for a $250,000 construction company credit line with average gross revenue of $250,000 or more.

$250,000+ Construction Working Capital Credit Line

Contractors with more than $250,000 in gross monthly revenue can apply for a credit line of $250,000 or greater. Unlocking this amount of capital can be used for large-scale commercial or government projects. This level of funding allows you to manage multiple crews and keep your projects on schedule. Your business can also qualify for a $500,000 contractor working capital credit line should your average gross revenue exceed $500,000 or more.

Trades That Use a Construction Working Capital Credit Line

Key Takeaways

- Project Mobilization: A working capital line allows trades to “float” the significant upfront costs of labor and materials before the first draw or milestone payment is released.

- Managing Retainage: These funds unlock the 5% to 10% in retainage fees typically held back by GCs, allowing you to pay your crews while waiting for the final project closeout.

- Supply Chain Agility: In 2026, specialized contractors use revolving credit to bulk-purchase materials like R-32 refrigerant or copper wiring to hedge against price fluctuations and seasonal demand.

- Continuity During Delays: Whether it’s waiting for a Certificate of Occupancy or navigating a two-stage insurance payout, a credit line ensures that 941 taxes and payroll never stop.

General Contractors

General contractors use a Construction Working Capital Credit Line to cover payroll, insurance, and workers’ compensation, or even to pay subcontractors when waiting for payments from customers. A construction revolving line of credit can be used over and over to cover these types of expenses. Large commercial and government projects require access to liquidity in order to accept purchase orders and begin mobilization. A revolving line of credit for contractors gives you the capital you need to keep projects moving forward and take on new business without straining your cash flow.

HVAC Contractors

HVAC contractors can use an HVAC revolving line of credit to cover expenses such as condensers, thermostats, or enough R-32 refrigerant for the entire summer. With 2026 marking a major transition in low-GWP refrigerant standards, being ready for peak seasons is more expensive than ever. A revolving line of credit for use during peak seasons allows you to hire more technicians as well. Pay down your credit line and continue to use it over and over as opportunities arise to take on more service calls or large-scale installations.

Roofing Contractors

Roofing contractors can use their roofing credit line to purchase materials in bulk and be prepared for insurance claims during storm season. Insurance companies typically pay these claims in a two-stage process: the first payment is based on the Actual Cash Value (ACV), while the second payment is based on the Replacement Cost Value (RCV). You can use a Construction Working Capital Credit Line to cover your business expenses while waiting on the second payment (recoverable depreciation), which can sometimes take weeks or months.

Electrical Contractors

Large commercial or municipal projects often require that electrical contractors work with purchase orders that do not pay until the project receives its Certificate of Occupancy. This can take weeks or months before the final payment is received. Use an electrical contractor’s revolving line of credit to purchase inventory for these projects, such as copper wiring, electrical panels, and transformers. Access to revolving working capital allows electrical contractors to take on more projects and keep bills paid while receivables exceed cash on hand.

Plumbing Contractors

Use a credit line for plumbing contractors to bridge gaps between customer payments and business expenses. Use your funds for anything from a digital marketing campaign to covering retainage fees held back on large projects. In 2026, while many private projects now cap retainage at 5%, that capital is still locked until the project is completed in full. This requires dealing with other contractors who need to finish their jobs, as well as material or weather delays common to the construction industry. A working capital line of credit allows you to unlock the value of those fees and use that capital toward growing your business.

Landscaping Contractors

Use your landscaping contractor’s revolving credit line to purchase equipment such as mowers, blowers, edgers, or any gear you need to keep your crews working efficiently. Commercial and municipal contracts also require that landscapers float project expenses upfront for months at a time. These costs can add up, especially when working multiple job sites. You can also use your landscaper’s line of credit to cover payment gaps when customers pay on Net 30, 60, or even 90-day cycles, ensuring that your payroll and taxes are always covered.

Frequently Asked Questions (FAQ)

What is a Construction Working Capital Credit Line

A construction business line of credit for contractors is a revolving financing solution that provides access to working capital for materials, payroll, and job-related expenses. Contractors can draw funds, repay them, and reuse the credit as needed to manage cash flow gaps caused by Net 30, 60, or 90 payment terms.

How do I qualify for a construction business line of credit?

To qualify for a construction business line of credit, lenders typically require at least $15,000 in monthly gross deposits over the last 3 to 4 months. Underwriters focus on consistent revenue, deposit frequency, and banking activity rather than just your credit score.

How much can I get approved for with a contractor line of credit?

Approval amounts are usually based on your average monthly revenue. Most contractors can qualify for a credit line equal to their monthly deposits, adjusted for any existing loan obligations or active positions.

Can I get a construction line of credit with bad credit?

Yes, you can get a construction business line of credit with bad credit. Many lenders accept FICO scores as low as 550, especially if your business shows strong and consistent cash flow.

How fast can I get funding for a construction line of credit?

Most construction lines of credit approvals are issued the same day, with funding available in 24 to 48 hours. Same-day wire funding may be available if all underwriting steps are completed early.

What can I use a construction business line of credit for?

You can use a construction line of credit for materials, payroll, equipment rentals, insurance, and other project-related expenses. This flexibility helps contractors maintain operations and avoid project delays.

What are the repayment terms for a construction line of credit?

Repayment terms typically range from 3 to 24 months. Payments are usually made daily or weekly, although stronger applicants may qualify for weekly or monthly payment schedules.

Why would a construction line of credit application be denied?

Common reasons for denial include prior defaults, payment modifications, low monthly revenue, excessive NSF charges, and inconsistent deposit activity. Maintaining strong cash flow and clean banking history improves approval chances.

About the Author

Robert “Todd” Holliday is a construction financing specialist with over two decades of combined experience in the construction and alternative lending sectors. Since 2020, he has facilitated millions of dollars in capital for contractors across the U.S., helping them navigate the complex cash flow cycles of the modern industry. As the former founder of ShadeIt, LLC (2004–2005), a commercial and residential tension shade fabricator, Todd possesses the unique “boots-on-the-ground” perspective required to understand the real-world financial pressures of materials, payroll, and project delays. He now leverages that expertise to bridge the gap between construction firms and the best available 2026 funding options.

Financial Disclaimer The information provided in this guide is for educational and informational purposes only and does not constitute professional financial, legal, or tax advice. Loan rates, terms, and SBA program guidelines mentioned are based on early 2026 market projections and are subject to change without notice based on lender criteria and Federal Reserve policy. Qualification for any construction loan product depends on individual business factors, including credit score, annual revenue, and time in business. We recommend consulting with a certified financial advisor or a qualified tax professional before entering into any credit agreement.