Key Takeaways

- Beat Seasonality: Use a revolving line to stock up before summer heatwaves or winter storms hit, so you aren’t caught off guard.

- Bridge Invoice Gaps: Cover payroll and high inventory costs while waiting 30 to 90 days for commercial clients to pay.

- Scale with Revenue: Your credit limit grows as your deposits grow, providing a funding solution that scales with your business.

- Fast Mobilization: Access funds in 24 to 48 hours to hire extra techs or repair your fleet during peak demand.

HVAC Contractor Cash Flow Challenges and Seasonality

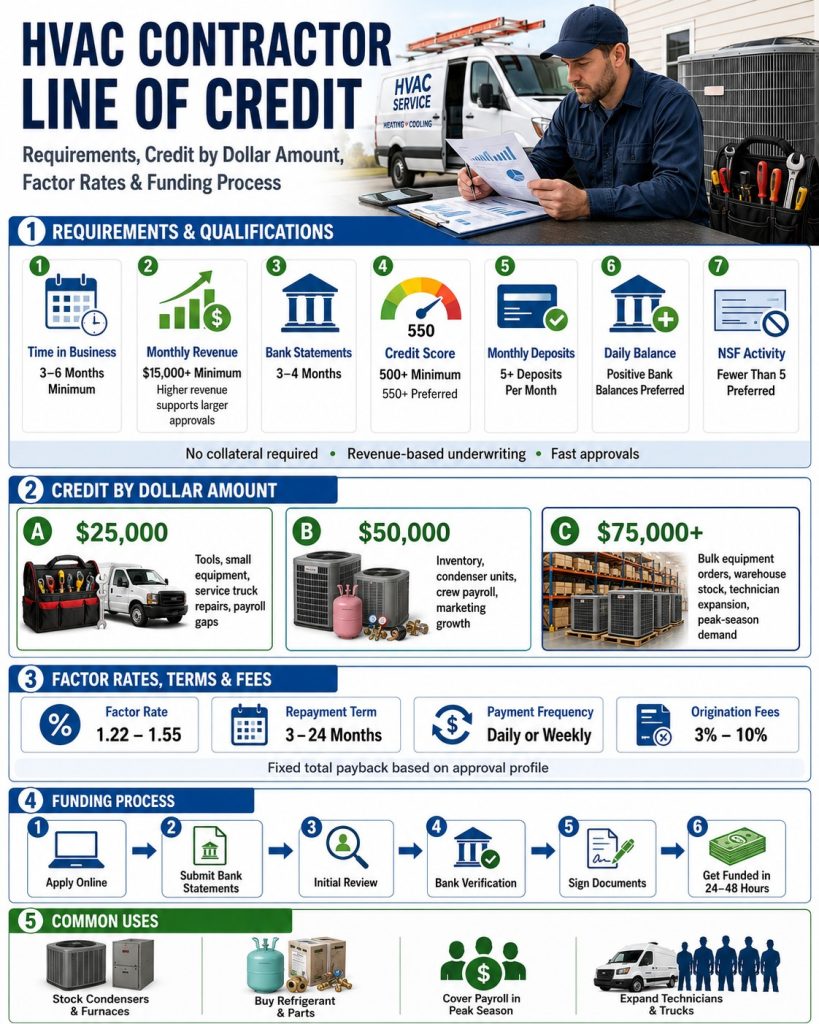

A construction business line of credit for HVAC contractors provides the fast working capital needed to cover critical expenses like payroll, 941 taxes, and inventory. As an HVAC specialist, you deal with extreme seasonality that other trades don’t face. A sudden winter storm or a record-breaking summer heatwave can keep your phones ringing off the hook, but the “shoulder seasons” can be dangerously unpredictable. Commercial HVAC contractors, in particular, often have to float massive upfront costs for units and labor while customers wait 30, 60, or even 90 days to settle their invoices.

Using a Construction Line of Credit to Cover HVAC Expenses

An HVAC working capital credit line helps your business cover these spikes in expenses without draining your cash reserves. Having a revolving line of credit ensures your crews stay on the clock and your projects aren’t stalled by cash flow gaps. We use your actual revenue to unlock approvals ranging from $25,000 to $250,000. Because this is a scalable solution, your access to capital is primarily limited by your monthly deposits—meaning as you take on more service calls and installations, your borrowing power increases.

What You Will Learn About HVAC Lines of Credit

I’ve been on your side of the desk as a business owner, and I know that having cash on hand is the difference between winning a big contract and watching it go to a competitor. In this guide, I’ll show you exactly how to apply for an HVAC contractor’s line of credit to bridge the gap between your daily expenses and customer payments. We will dive into how revenue-based underwriting works, what lenders look for in your bank deposits, and how to get this capital working for you in 24 to 48 hours.

How HVAC Contractors Use a Line of Credit to Grow Revenue

Key Takeaways

- Inventory Readiness: Use smaller lines to stock up on R-32 refrigerant and units before the summer rush or winter freezes.

- Large Project Capacity: Mid-sized lines allow you to float labor and material costs for multi-unit housing or commercial installs.

- Commercial Power: High-limit lines provide the mobilization capital needed for government and municipal contracts.

- Equipment & Fleet: Access fast cash to rent specialized equipment like sky lifts or to repair your fleet during peak service months.

$25,000–$50,000 HVAC Line of Credit for Small Jobs

A $25,000 to $50,000 HVAC credit line is ideal for small to medium-sized contractors generating up to $50,000 in monthly revenue. This level of working capital is perfect for stocking up on R-32 refrigerant, condensers, and fan blowers, or securing units from major brands like Trane and Carrier. Having this cash on hand gives you the flexibility to respond to emergency service calls immediately without draining your operating account.

$50,000–$100,000 HVAC Line of Credit for Mid-Size Projects

A $50,000 to $100,000 line of credit allows HVAC contractors to scale up for larger projects, such as multi-unit housing developments or retail build-outs. Projects like these often require you to cover significant labor and material costs weeks before the first draw is released. This level of funding lets you manage multiple jobsites simultaneously without hitting a cash flow wall. To qualify, you’ll typically need consistent monthly deposits between $50,000 and $100,000.

$100,000–$200,000 HVAC Line of Credit for Commercial Contracts

Large-scale commercial and municipal contracts demand serious liquidity. A $100,000 to $200,000 credit line provides the cushion needed to support massive purchase orders and navigate the “wait time” associated with milestone progress payments. If your business is generating $100,000 to $200,000 in monthly revenue, unlocking this tier of credit allows you to bid on more lucrative contracts that your competitors might have to pass up.

$200,000–$250,000 HVAC Line of Credit for Seasonal and Emergency Demand

For high-volume HVAC firms, a $200,000 to $250,000 revolving line is a strategic tool for large government or institutional projects. This capital can be used to mobilize entire teams of technicians, buy materials in bulk to hedge against 2026 price spikes, and rent specialized gear like sky lifts or forklifts for multiple sites. If your business generates $200,000 to $250,000 in monthly revenue, this line ensures you never have to say “no” to a major opportunity due to a lack of cash.

Revenue-Based Underwriting for HVAC Business Line of Credit

Key Takeaways

- Skip the History Lesson: We look at your last 90 days of deposits, not tax returns from two years ago.

- Bank Activity is King: Your credit limit is based on your real-time revenue. If you’re billing more, you’re getting more.

- Clean Statements Matter: Avoid NSF fees and keep your daily balances positive to snag the best rates.

- Fast Cash, No Red Tape: Since we aren’t auditing your entire life story, you can have a wire transfer in 24 to 48 hours.

Revenue-Based Underwriting vs. Traditional Bank and SBA Loans

Let’s be honest: traditional banks live in the past. They’ll ask for three years of tax returns and personal financial statements just to tell you “no” three weeks later. SBA loans are even slower. Revenue-based underwriting is different because it’s focused on the now. We look at your last 3 to 4 months of business bank statements to see how you’re performing today. It’s a real-time snapshot. If your business is moving and the cash is hitting the account, that’s all we need to see.

How HVAC Credit Line Approval Amounts Are Calculated

Underwriters do some quick math by averaging your last 3 to 4 months of gross deposits. If you’re in New York or California, have 4 months ready—it’s a state regulation thing. We take that average, subtract any other unsecured loans you’re already paying on, and that’s your baseline. Lenders want to see stability. They like consistent deposits and high daily balances. If you’ve got a bunch of NSF (overdraft) fees, it’s going to be a tougher sell. But if your banking is clean, your credit limit will scale right along with your revenue.

Fast Approvals with Streamlined Documentation and Funding

The whole point here is speed. Because we’ve cut out the “paperwork tag” you play with big banks, we can move fast. Usually, it’s 24 to 48 hours from the time you apply to the time the money hits your account. Sometimes even faster. Less red tape means you can actually jump on a big multi-unit install or fix a fleet of broken trucks without waiting for a committee to approve it. It’s fast, it’s clean, and it keeps your crew on the job.

HVAC Contractor Line of Credit Requirements and Qualifications

Key Takeaways

- Revenue is King: You need at least $15,000 in monthly deposits to get through the door, and your average revenue sets your credit limit.

- Banking Hygiene Matters: Keeping your NSFs, or overdrafts, under five and maintaining five or more monthly deposits is the secret to lower rates.

- Fast Path to Elite Terms: Once you hit two years in business or a 600+ credit score, you unlock much higher limits and better repayment options.

- Low Credit is OK: You can still qualify with a 550 score as long as your cash flow is strong and consistent.

Monthly Revenue Requirements and Credit Line Approval Amounts

Underwriters are going to look closely at your bank deposits to see if you can actually handle a credit line. To even get a look, you need to show at least $15,000 hitting your business account every month for the last three or four months. If you’re based in California or New York, have four months of statements ready—it’s just the way the laws are written there.

We calculate your limit based on those deposits. For example, if your last three months looked like this:

- Month 1: $76,000

- Month 2: $83,000

- Month 3: $81,000

- Your Average: $80,000

In this scenario, you’d likely get a credit limit of around $80,000. Now, if you have other loans out, we have to subtract those payments from the total. But as long as your cash flow is strong and you aren’t bouncing checks, you’re in a good spot to get the max amount.

Deposit Frequency and Customer Payment Activity

Lenders don’t just look at the total dollar amount; they look at how many times a month you’re actually making deposits. You need at least five deposits a month to qualify. Why? Because if you only have one or two big deposits, it looks like you’re relying on a single customer. If that one guy pays late, your whole business stops. Having five or more deposits shows the lender that your HVAC business has a solid, diverse customer base.

Bank Account Health and Cash Flow Stability Requirements

The “health” of your bank account is basically a scoreboard for how you manage your money. Keeping a high daily balance tells the credit team that you aren’t living hand-to-mouth. You really want to avoid “Non-Sufficient Funds” (NSF) events. If you have more than five of those in a four-month period, you’re either going to get denied or hit with really high rates. A clean bank record is the fastest way to lower your borrowing costs.

Time in Business and Contractor Experience Requirements

You need to be in business for at least six months to get approved. If you’ve been at it for two years or more, you start unlocking the “elite” programs that have much higher limits and better terms. It just proves to the lender that you’ve survived a few seasons and know how to manage a crew.

Credit Score Requirements for HVAC Contractors

Revenue is the big driver here, but you still need a credit score of at least 550 to get through the door. If you’re over 600, your options get a lot better. A low score won’t always kill the deal, but it will make the money more expensive. The higher the score, the cheaper the capital.

Existing Loans, Debt Positions, and Stacking Guidelines

If you already have a loan or a “position” open, you can still apply. We just have to make sure your monthly revenue can support another payment. Some lenders won’t let you have more than two active loans at once, while others are a bit more flexible. Just remember: the more loans you “stack,” the higher your risk and your total costs will be.

Secured vs Unsecured HVAC Business Line of Credit

Key Takeaways

- Speed vs. Cost: Secured lines take weeks to fund but offer the lowest rates. Unsecured lines fund in 24–48 hours but carry higher costs.

- Collateral Requirements: Secured lines put your trucks or real estate at risk. Unsecured lines are based strictly on your bank deposits.

- Payment Structure: Secured loans often allow for interest-only payments. Unsecured loans typically require you to pay back principal and interest with every draw.

- Ease of Entry: Skip the appraisals and deep audits with an unsecured line—all you need are your recent bank statements.

Secured HVAC Credit Line

A secured credit line for HVAC contractors requires that you pledge collateral, such as equity in heavy equipment or real estate, to cover your loan in case of a default. Banks will usually lend a percentage of the value of the assets that you are pledging. Loans against real estate are typically taken at 80% of the value; this means the bank will loan you up to 80% of the property equity. This is also known as the LTV, or loan-to-value. Heavy equipment is valued at a much lower rate. Secured credit lines offer the best interest rates, which usually start at the prime rate plus a percentage. However, the approval process may be slower due to appraisals, financial reviews, and other issues that can cause delays. This process can sometimes take several weeks or months to complete.

Unsecured HVAC Credit Line

An unsecured credit line from an alternative lending source does not require collateral, appraisals, or any extensive documentation. Simply fill out a credit application and submit your last 3 to 4 months of bank statements (NY and CA must submit 4 months). Funding is available in 24 to 48 hours. Unsecured credit lines are perfect for covering expenses when receivables exceed your cash on hand. Use these funds for expenses such as materials, payroll, or any other short-term costs that you may have. Secured options offer better pricing; however, unsecured loans offer speed and convenience that are worth the extra costs.

Key Differences

The biggest difference between the two is that a secured HVAC contractor credit line will allow you to make interest-only payments. You can make interest-only payments until the credit line is completely paid. In contrast, an unsecured line of credit requires that you make both principal and interest payments for each draw that you take. Secured credit lines are more flexible with your payment frequency and the amount of time they give you to pay the balance off. Unsecured loans sometimes have weekly or daily payments and higher borrowing costs, but they are available in 24 to 48 hours, or less.

Secured HVAC Credit Line

A secured credit line for HVAC contractors requires that you pledge collateral, such as equity in heavy equipment or real estate, to cover your loan in case of a default. Banks will usually lend a percentage of the value of the assets that you are pledging. Loans against real estate are typically taken at 80% of the value; this means the bank will loan you up to 80% of the property equity. This is also known as the LTV, or loan-to-value. Heavy equipment is valued at a much lower rate. Secured credit lines offer the best interest rates, which usually start at the prime rate plus a percentage. However, the approval process may be slower due to appraisals, financial reviews, and other issues that can cause delays. This process can sometimes take several weeks or months to complete.

Unsecured HVAC Credit Line

An unsecured credit line from an alternative lending source does not require collateral, appraisals, or any extensive documentation. Simply fill out a credit application and submit your last 3 to 4 months of bank statements (NY and CA must submit 4 months). Funding is available in 24 to 48 hours. Unsecured credit lines are perfect for covering expenses when receivables exceed your cash on hand. Use these funds for expenses such as materials, payroll, or any other short-term costs that you may have. Secured options offer better pricing; however, unsecured loans offer speed and convenience that are worth the extra costs.

Key Differences

The biggest difference between the two is that a secured HVAC contractor credit line will allow you to make interest-only payments. You can make interest-only payments until the credit line is completely paid. In contrast, an unsecured line of credit requires that you make both principal and interest payments for each draw that you take. Secured credit lines are more flexible with your payment frequency and the amount of time they give you to pay the balance off. Unsecured loans sometimes have weekly or daily payments and higher borrowing costs, but they are available in 24 to 48 hours, or less.

Factor Rates, Terms, and Repayment for HVAC Credit Lines

Key Takeaways

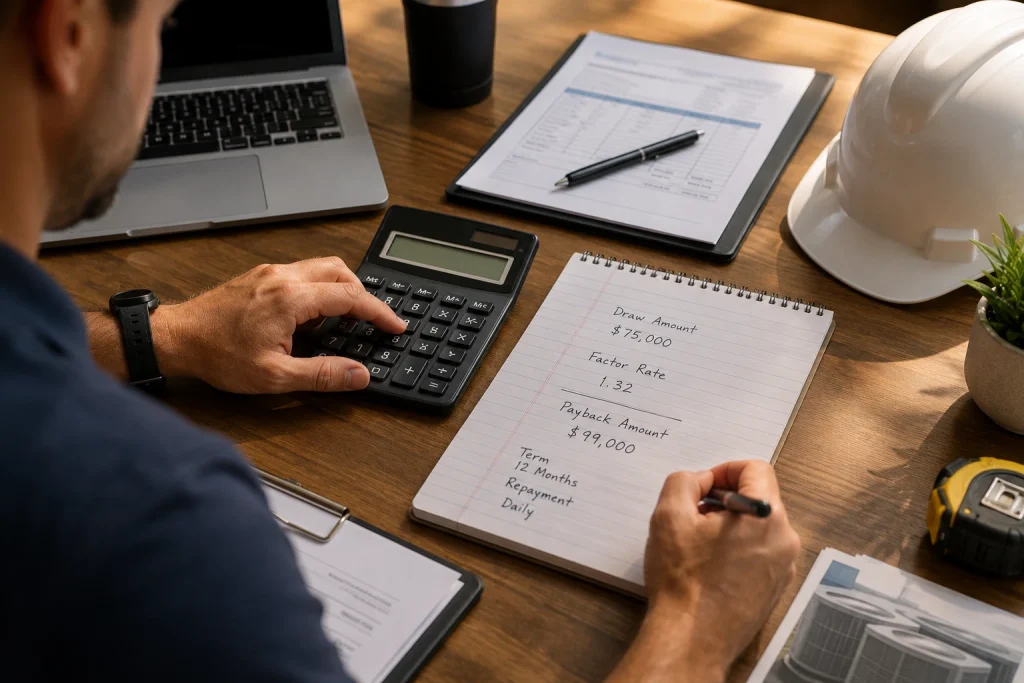

- Factor Rates: Costs are calculated using a fixed multiplier, such as 1.20, not a traditional accruing interest rate.

- Cost Example: A $50,000 draw with a 1.32 factor rate means a total payback of $66,000.

- Repayment Terms: Terms range from 3 to 24 months depending on your business strength and cash flow.

- Payment Frequency: Payments are made daily, weekly, or monthly, with the best options reserved for strong credit profiles.

- Risk vs. Rate: Lower credit scores and inconsistent deposits will result in higher factor rates and more frequent payments.

How Factor Rates Work for HVAC Credit Lines

Alternative lenders calculate finance charges differently from traditional lenders, such as banks or SBA-type loans. Conventional-type loans calculate finance charges using interest rates that accrue either daily or monthly. In contrast, alternative lenders calculate your finance charges using a factor rate. A factor rate is based on a fixed multiplier, which is then multiplied by your loan amount to determine your finance charges. For example, a $50,000 loan with a 1.32 factor rate will have a total payback of $66,000. Your factor rate is determined based on your qualifications. The stronger your profile, the better your rates will be. Borrowers with low credit scores who meet minimum qualifications will pay higher rates. Rates can range anywhere from 1.20 to 1.45 or greater, depending on how your business scores.

HVAC Credit Line Payment Terms Explained

Your payment terms refer to how long or how many payments you need to make to pay off the loan. Terms are approved on a case-by-case basis. Shorter terms have higher payments; however, you will pay less in overall finance charges. Longer terms have lower payments but higher overall finance costs. Terms will usually range from 3 to 24 months. It is important to align your repayment term with your expected cash flow and project timelines to ensure the payments remain manageable.

HVAC Credit Line Payment Frequency Options

Your payment frequency refers to how often you will make a payment. Unsecured credit lines for HVAC contractors are paid either daily, weekly, or monthly. This is determined on a case-by-case basis. Borrowers with strong credit, consistent revenue, and properly managed cash flow will qualify for better options. Those with less-than-desirable credit and poor cash flow will more than likely have a daily payment.

Bad Credit HVAC Business Line of Credit (Fast Approval Options)

Key Takeaways

- Credit Isn’t Everything: You can qualify with a 550 FICO because lenders care more about your bank deposits than your score.

- Cash Flow is King: Strong, steady deposits over the last 3 to 4 months are the best way to offset a low credit score.

- Higher Costs for Risk: Expect a factor rate of 1.40 or higher and daily payments if your credit is less than perfect.

- Build for the Future: Once you show a solid payment history, you can move into better rates and longer terms.

Can You Qualify with Bad Credit

Bad things happen to good people. Life events such as divorce or accidents can leave borrowers with bad credit. HVAC contractors with a FICO score as low as 550 can still apply for an unsecured line of credit. Lenders focus more on your overall deposits and cash flow vs. your credit score.

How Revenue Offsets Credit Risk

Underwriters focus on your last 3 to 4 months of business bank statements. Consistent and strong monthly deposits can significantly increase your chances of getting approved, despite your less-than-perfect credit history. You can still be approved and funded so long as you meet minimum requirements and demonstrate your ability to repay the loan.

What to Expect with Terms

It is still possible to be approved with bad credit; however, your terms and factor rate will usually reflect the extra risk. Expect to pay a factor of 1.40 or higher, depending on the complexity of your file. Borrowers with less-than-perfect credit will usually qualify for a shorter term and a daily payment. You can receive better rates and terms in the future once you have established some payment history.

Submit Credit Application

To start the request for a construction credit line, the owner must fill out the online application form. This initial step captures fundamental data such as your name, the legal name of the business, and a contact phone number. You will also be required to provide information regarding the company’s background, tenure, and other significant professional details.

Submit Business Bank Statements

As part of the digital application process, contractors must provide their bank statements from the previous three to four months. State laws require businesses in New York or California to submit four months of these records. Please note that records from third-party processors like PayPal or Stripe are not acceptable for this requirement. Possessing a verified, business-specific bank account is a fundamental requirement for approval.

Receive Pre-Approval Offer

Preliminary offers are typically sent within a few hours, though complex financial files may require more time for a complete review. This notice will specify the proposed credit limit, the factor rate, and the schedule for repayments. These details allow the contractor to analyze the total cost and the predicted profit margins for their project. If the company does not meet the necessary criteria, the applicant will be notified and can re-apply after 90 days.

Sign Documents

Once you agree to the terms, the formal loan contract will be prepared for your signature. You can sign these papers electronically through platforms like DocuSign for a faster process. In addition to the signatures, you must upload a copy of your state-issued ID and a voided check for the business. Depending on the specific file, you might also be asked for 1040 tax returns or incorporation documents.

Final Underwriting Review

The application enters the final underwriting stage once all the required paperwork has been submitted. Lenders check DataMerch to ensure there are no outstanding defaults or unpaid balances with other creditors.

Additionally, you must link your bank account via DecisionLogic to give underwriters a live look at your current month’s transactions. This step confirms that revenue is steady and identifies any existing debts that were not previously disclosed. Finding unlisted liabilities during this phase can result in an increased interest rate or an outright denial. The account must also maintain a positive balance and have enough cash to cover the first three scheduled installments.

Merchant Interview

A mandatory, brief phone conversation with the business owner is required before any capital is disbursed. During this five-to-ten-minute call, the analyst will inquire about how the credit line will be used. This is done to confirm that the funds are intended for business operations and not for personal needs. Complete transparency is essential, as any indication of personal use will lead to the application being rejected.

Final Funding

Once the interview is successfully concluded, the money is cleared for immediate release. Funds sent by wire transfer typically arrive the same day if the process is finished before 4:00 PM ET. Wire transfers initiated after the afternoon cutoff are generally available on the next business day. If you choose an ACH transfer, it usually takes one to two days for the funds to fully clear in your account.

How to Apply for HVAC Line of Credit (24–48 Hour Funding)

Submit Credit Application

To start the request for a construction credit line, the owner must fill out the online application form. This initial step captures fundamental data such as your name, the legal name of the business, and a contact phone number. You will also be required to provide information regarding the company’s background, tenure, and other significant professional details.

Submit Business Bank Statements

As part of the digital application process, contractors must provide their bank statements from the previous three to four months. State laws require businesses in New York or California to submit four months of these records. Please note that records from third-party processors like PayPal or Stripe are not acceptable for this requirement. Possessing a verified, business-specific bank account is a fundamental requirement for approval.

Receive Pre-Approval Offer

Preliminary offers are typically sent within a few hours, though complex financial files may require more time for a complete review. This notice will specify the proposed credit limit, the factor rate, and the schedule for repayments. These details allow the contractor to analyze the total cost and the predicted profit margins for their project. If the company does not meet the necessary criteria, the applicant will be notified and can re-apply after 90 days.

Sign Documents

Once you agree to the terms, the formal loan contract will be prepared for your signature. You can sign these papers electronically through platforms like DocuSign for a faster process. In addition to the signatures, you must upload a copy of your state-issued ID and a voided check for the business. Depending on the specific file, you might also be asked for 1040 tax returns or incorporation documents.

Final Underwriting Review

The application enters the final underwriting stage once all the required paperwork has been submitted. Lenders check DataMerch to ensure there are no outstanding defaults or unpaid balances with other creditors.

Additionally, you must link your bank account via DecisionLogic to give underwriters a live look at your current month’s transactions. This step confirms that revenue is steady and identifies any existing debts that were not previously disclosed. Finding unlisted liabilities during this phase can result in an increased interest rate or an outright denial. The account must also maintain a positive balance and have enough cash to cover the first three scheduled installments.

Merchant Interview

A mandatory, brief phone conversation with the business owner is required before any capital is disbursed. During this five-to-ten-minute call, the analyst will inquire about how the credit line will be used. This is done to confirm that the funds are intended for business operations and not for personal needs. Complete transparency is essential, as any indication of personal use will lead to the application being rejected.

Final Funding

Once the interview is successfully concluded, the money is cleared for immediate release. Funds sent by wire transfer typically arrive the same day if the process is finished before 4:00 PM ET. Wire transfers initiated after the afternoon cutoff are generally available on the next business day. If you choose an ACH transfer, it usually takes one to two days for the funds to fully clear in your account.

Construction Business Lines of Credit for Other Trade Contractors

Key Takeaways

- Bridge the Insurance Gap: Roofers can float material and labor costs while waiting for the final insurance checks to clear.

- Survive Commercial Delays: Electricians can cover high-cost items like copper and panels until the building gets its certificate of occupancy.

- Fund Marketing & Growth: Plumbers can use the line for daily expenses or to run Google and Facebook ads to get more trucks on the road.

- Beat Seasonal Slumps: Landscapers can manage cash flow spikes during peak seasons to fuel crews, buy bulk mulch, and rent gear.

Line of Credit for Roofing Contractors

Roofing contractors who work with insurance companies often need to purchase materials and pay for labor before getting paid. A roofing contractor can use a revolving credit line to cover expenses such as shingles, underlayment, labor, and equipment. The initial actual cash value check does not always cover your total expenses 100% upfront while you wait for the final replacement cost value check to be released. A roofing company’s revolving line of credit bridges that gap.

Line of Credit for Electrical Contractors

Electrical contractors can use a revolving line of credit to cover expenses such as copper wiring, breaker panels, and conduit. Some commercial projects require electrical contractors to wait until the project is completed and has received its certificate of occupancy before final payments are made. Having an open line of credit keeps your cash flow moving smoothly during these long commercial wait times.

Line of Credit for Plumbing Contractors

A plumbing contractor can use a revolving credit line for a lot of different reasons. Use your line of credit for anything from payroll to expenses such as pipe, fittings, water heaters, insurance, or just about any cost you can imagine. You can also use your plumbing contractor’s line of credit for marketing expenses like Google or Facebook ads to actively acquire new customers and keep your trucks busy.

Line of Credit for Landscaping Contractors

Landscaping contractors often experience seasonal cash flow fluctuations that make access to working capital essential. Expenses such as mulch, stone, irrigation systems, fuel, payroll, and equipment rentals can add up quickly during peak seasons. A landscaping contractor line of credit helps businesses manage multiple crews and take on larger commercial or municipal projects with confidence.

Can I qualify for an HVAC contractor line of credit with bad credit?

Yes, you can still qualify with a credit score as low as 550 so long as your business has $15,000 per month in gross revenue and you are able to meet minimum requirements. Underwriting focuses on your revenue and the overall health of your cash flow vs. your credit.

How much can I qualify for with an HVAC business line of credit?

Your credit limit is typically based around the average of your last 3 to 4 months of gross monthly deposits (NY and CA residents must submit 4 months) less any existing loan/positions that you may already have.

What can I use an HVAC contractor line of credit for?

You can use your line of credit to purchase HVAC equipment, R-32 refrigerant, condensers, furnaces, inventory, cover payroll, repair service vehicles, or finance any other business-related expense.

How quickly can I receive funding?

Once you complete the credit application and submit business bank statements, you can receive funding within 24 to 48 hours. Some applications may even qualify for same-day funding.

What documents do I need to apply?

You need to complete a short online application and submit the last three or four months of business bank statements. Borrowers in New York or California will usually need four months of statements.

Do I need collateral to qualify?

No, you do not need any collateral to be approved and funded.

Can I qualify if I already have another business loan?

Yes, you may still qualify if your monthly revenue is strong enough to support another payment. Underwriters will review existing debt before determining available credit limits.

How often do I need to pay my HVAC credit line?

Your payment frequency is determined by your overall qualifications. Depending on how you qualify, payment frequency is going to be either daily, weekly or monthly. Borrowers with stronger credit profiles will qualify for either weekly or monthly.